Diversifying infrastructure options and enhancing capacity are key for maintaining sector attractiveness

Few sectors are as fundamental to supporting long-term economic development as transport. As Ghana’s growth has accelerated in recent years, the government has sought to boost investment in all modes of transport through public and private resources.

Unlike many emerging markets, Ghana’s transport backbone covers every region of the country, with heavy concentration in the most economically developed areas, such as around the capital, Accra.

Credentials

The country’s transport network is relatively well developed by African standards. Nonetheless, as the country moves into the middle-income bracket, limitations in infrastructure are becoming increasingly apparent, and in some cases are impeding growth in select sectors.

Fortunately, the flow of oil earnings that have stimulated Ghana’s growth also provide the resources to address bottlenecks and build infrastructure to support long-term economic and social development. As such, the government is keen to attract more participation from private and foreign partners.

The benefits from transportation infrastructure development are clear. According to World Bank estimates, raising the country’s infrastructure spending level to that of upper-middle-income countries could boost Ghana’s annual growth by as much as 2.7%.

In its 2013 report on transport in Africa, “Africa Gearing Up”, PwC included Ghana as one of 10 African case studies of important markets. The group identified key competitive advantages such as the strong growth rate, high foreign direct investment inflows and the diversified economy. However, “critical limiting factors” were also noted, including a growing tax burden, weak rule of law and a widening fiscal deficit. Overall, the report asserted that, “Ghana will continue to foster its reputation and position to be known as a safe gateway to West Africa and an ideal point of arrival for newcomers to Africa.”

Growth Drivers

PwC identifies consumer goods as a major driver of logistics and transport demand in Africa, highlighting that 70% of the world’s biggest consumer goods companies are already active on the continent, a sign that they are making “big bets” on growth. Demographics and a growing middle class are also recognised as trends likely to support market growth both in terms of “formal” modern retail and traditional retail, with international firms increasingly tapping into the latter as well as the former. These trends apply to Ghana, with its population growth rate now topping 2.2% and increasing affluence – factors which prompted the World Bank to reclassify it as a low-middle-income country in 2011.

One area showcased by PwC is micro-distribution. The report affirmed that this occurrence tends to affect consumers in areas with less-developed supply chains. Micro-distribution was pioneered in Africa by Coca-Cola, whose micro-distribution centres (MDCs) are small-scale depots owned by local entrepreneurs who act as middlemen between bottlers and small retailers, particularly in hard to reach areas. The US drinks company has 3000 MDCs in East Africa, employing around 13,500 people, with each MDC generating as much as $30,000 in monthly revenue.

Supporting Sectors

PwC suggests that countries that are dependent on minerals and fossil fuels for export earnings will look to boost agriculture to diversify their economies. This will lead to increased demand for the transport business. Ghana’s economy is already somewhat diversified, but efforts to boost agriculture – which already employs the majority of the workforce – could still have an impact on the transport sector. To this end, with large swathes of fertile land and the strength of existing agricultural commodities, including cocoa, Ghana becomes one of the most promising countries in sub-Saharan Africa for agricultural development.

Manufacturing development will be another source of demand. While industry’s share of the country’s GDP actually declined over the past decade, this can be attributed to the rapid rise of the oil sector. In fact, there are several positive signs, including the announcement in September 2013 by Indian automotive manufacturer Mahindra to build an auto assembly plant in Ghana with a local partner. At the time of writing, there were no developments as to when this initiative would be launched.

Downsides

Drags on regional supply chain, logistics and transportation growth come from a range of factors. One of the most serious is a lack of intraregional trade; only 11% of African countries’ trade is with other African partners, according to PwC.

The company places some hopes in the tradeboosting efforts of regional trade organisations such as ECOWAS, of which Ghana is a member, along with 14 of its neighbours. Potentially even more promising in the longer term is a mooted free trade zone that would encompass a large number of countries on the continent. There is some scepticism about the project meeting its timeline, however, with multilateral cooperation moving rather slowly, in part hampered by the multiple jurisdictions, domestic political considerations and disagreements between individual countries. Yet, should further cooperation be achieved, it would represent a key step forward for African trade, which could ultimately create major opportunities for transport and logistics service providers on the continent.

Enter The Dragon

While Ghana has better roads and ports than many African countries, it still faces major challenges. Among them are delays at ports, deteriorating road quality and a decline of rail networks. To this end, China’s lack of natural resources, but experience in developing its own infrastructure presents a strategic fit with Africa’s abundant resources and underdeveloped infrastructure. Across the continent, the Asian dragon is investing heavily in the development of rail networks, roads and utilities, among other things, as it increases commodity exports from resource-rich African countries.

Road Network

Roads are overwhelmingly the most important means of domestic transport in Ghana, accounting for 98% of freight and 95% of passenger traffic. Some 7% of the 1.47m vehicles on the road are heavy trucks, which cause significant wear-and-tear on road surfaces. This could be somewhat alleviated by rehabilitating the country’s rail network to shift heavy goods (such as bulk commodities) onto the tracks. This should lead to considerable cost and potentially time savings for companies shipping heavy loads, and their customers.

The local road network covered 68,124 km at the end of 2013, according to projections by the Ministry of Roads and Highways (MRH), which breaks the system down into three broad categories: trunk roads, feeder roads and urban roads.

Trunk roads are major arterial routes providing regional, inter-regional and international links, and are major conduits for trade. Including ferry routes on inland water bodies – in particular Lake Volta – the trunk road network in the country extends to 13,344 km. Feeder roads are the smaller routes that connect major routes to the settlements beyond, and, with a total length of 42,210 km, these make up the bulk of the broader road network. Feeder roads are designed to provide safe, all-weather access at optimal cost, and aid the flow of goods and people. These roads play an essential role in socio-economic development, particularly in rural areas, supporting the growing agriculture sector and, according to the MRH, boosting employment opportunities for women and the poor. At the urban level, meanwhile, there are approximately 12,400 km of roads in metropolitan areas and municipalities.

Each part of the system is administered by a different body under the MRH: the Ghana Highway Authority for trunk roads, the Department of Feeder Roads and the Department of Urban Roads. Also under the Ministry’s aegis is the Koforidua Training Centre, which provides skills training for transport sector professionals, including engineers, consultants and administrative staff, and the Road Fund Secretariat, which finances the maintenance, upgrade and rehabilitation of roads, as well as road safety activities.

One of the major focuses of Ghana’s road building programme is linking resource-rich areas in the more remote parts of the east and west of the country with the major urban centres and ports of the south, such as Accra, Tema, Takoradi and Kumasi. International connectivity is a priority: PwC highlights the Lagos-Abidjan highway, which passes along Ghana’s south coast, as one of the more promising trunk road developments in Africa.

Road Budget

The pilot programme budget for 2013-15, published by the MRH, plans expenditures of GHS363.96m ($138.74m) in 2014 and GHS366.97m ($139.9m) in 2015. Spending is split into four separate budget programmes: BP1, management and administration; BP2, road construction; BP3, road rehabilitation and maintenance; and BP4, road safety and environment.

In 2014 BP1 will receive GHS41.49m ($15.82m); BP2, GHS233.57m ($89.04m); BP3, GHS88.27m ($33.65m); and BP4, GHS10.62m ($4.05m). In 2015 BP1 is set to receive GHS41.58m ($15.85m); BP2, GHS225.8m ($86.07m); BP3, GHS88.85m ($33.87m); and BP4, GHS10.73m ($4.09m).

The programme looks to construct 313 km of roads in 2013, 189 km in 2014 and 220 km in 2015, including 93 bridges and interchanges, which require more complex engineering and specialist contractors, Funding presents the greatest challenge to road maintenance and upgrades in Ghana. The 2013 national budget saw a decrease of nearly 30% on transport expenditure. The government allocated $459.5m to the MRH and the Ministry of Transport (MoT) in 2013, compared to $647.8m in 2012. Public-private partnerships (PPPs) are seen as crucial for further developments. There is also pressure on the government to increase its fuel levy, a major funding source for road building and maintenance.

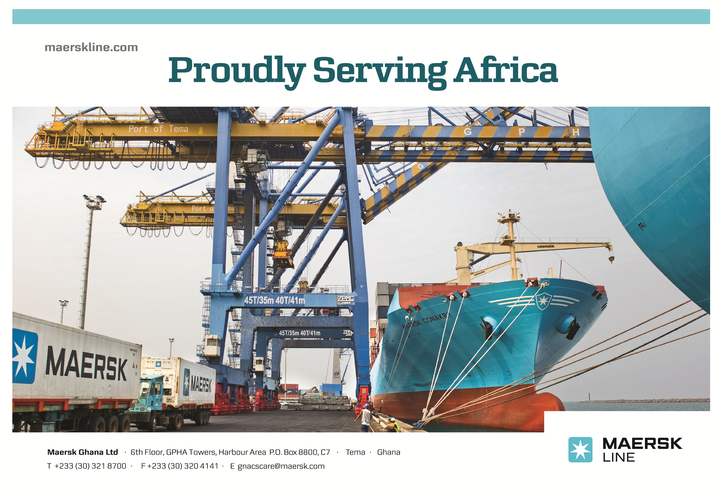

Tema

Ghana’s biggest, busiest port is Tema, 30 km east of Accra. Tema is home to a number of industries that have developed around its 3.9m-sq-metre port, through which 70% of the country’s trade flows, according to the Ghana Ports and Harbours Authority (GPHA). Traffic at the port facility has grown rapidly over the past decade, particularly since 2010 when Ghana’s oil production started and began to accelerate economic growth.

In 2013 the port registered 1553 vessel calls, up from 1521 in 2012, while total traffic reached 12.18m tonnes, up 6.2% from 11.47m tonnes. Of this total, the vast majority were imports, at 10.01m tonnes, up 6.7% from 9.38m in 2012. Exports through Tema grew 1.2% from 1.48m tonnes to 1.49m tonnes.

Total container traffic was 841,989 twenty-foot equivalent units (TEUs), rising 2.2% from 824,238 TEUs the previous year. Transit tonnage rose 17% from 530,457 to 620,668 tonnes, while trans-shipment grew from 50,403 to 51,748 tonnes.

To give an idea of the growth of volumes, in 2008 the port handled 8.73m tonnes of cargo and 555.01 TEUs of containerised freight. The key factor contributing to volume growth has been exports, which totalled just 6.12m tonnes in 2008. On the other hand, trans-shipments have plunged from a peak of 339,841 TEUs in 2006; the decline in entrepôt traffic is attributable to factors including regional competition, the trans-shipment operators being crowded out by Ghana-bound cargo and increasing congestion at the port driving customers elsewhere.

The steadiest growth over the past decade has come from container traffic, which fell only one year – 2009, at the peak of the global economic crisis – reflecting the international trend to greater containerisation, and Ghana’s domestic growth story.

Improvements Needed

While Tema benefits from Ghana’s political stability, it currently faces significant capacity challenges, PwC noted in its African logistics report. “Long waiting times pose security risks for ships,” the professional services group highlighted. Although local shippers do not see security as a primary risk, they acknowledge that the issue exists, according to the report. The bureaucratic process of moving freight through Tema often includes the need to visit several different, remote offices of various agencies at the port, exacerbating capacity bottlenecks. Currently, imports require permission from eight separate agencies, with six different forms to be completed, while exports require authorisation from six agencies and four forms, according to the World Bank’s 2013 Logistics Performance Index (LPI).

“In the 1980s the clearing process took one or two days, but in 2014, even with technological advancements, the dwell time is much, much longer,” MC Vasnani, managing director of Consolidated Shipping Agencies (Conship), told OBG. “At some point, people began to view the ports as goldmines. Now there are multiple active agencies, and there is significant overlap in authority among the Ports Authority, the Ghana Revenue Authority and other port agencies.”

Takoradi

Ghana’s second port is Takoradi, 225 km west of Accra and 300 km east of Abidjan. The facility is used primarily for exporting bulk commodities, and is starting to benefit from its proximity to Ghana’s newly operating oil fields.

In 2013, Takoradi saw ship calls drop to 1364 from 1664 in 2012 and 1798 in 2011, according to GPHA, though total port traffic in tonne terms still grew, reaching 5.45m, up 2.6% from 5.31m and 4.94m in 2012 and 2011, respectively. Exports accounted for 3.45m tonnes of this figure, and imports 1.99m tonnes, compared to 2.96m and 2.35m, respectively, in 2012.

Total container traffic, meanwhile, dropped 16% to 52,373 TEUs from 60,746 TEUs, falling to the lowest level since 2009. Container exports in 2013 totalled 27,513 TEUs and imports 24,860, down from 31,684 and 29,371 TEUs the previous year.

Expansion Project

In November 2013 the GPHA announced that it would seek investments worth $2.5bn to develop Tema and Takoradi, with the goal of increasing capacity, allowing the ports to handle larger ships and cutting vessel waiting times.

A key objective of the plan is to double Tema’s container capacity to 2m TEUs by 2018 to support its development as a regional hub. The first phase, to be completed by 2017, focuses on developing basic port infrastructure. This includes a breakwater, as well as dredging to increase the draught to 16m from the current 11.5m, which would allow access to ships with a capacity of 10,000 TEUs. The focus of this upgrade is to support five new berths, two for containers, two for multi-purpose and roll on-roll off vessels, and one for passenger and cruise ships. The next phases will add further container terminals and units for handling fruit and other perishables.

The first phase of the Takoradi expansion also includes extensive dredging to a 16-metre draught and the extension of the port’s breakwater. According to the GPHA, the expected outcomes include improving access, lowering turnaround times and developing a “service and logistic base” for the oil industry. The first-phase contract was awarded to Belgian contractor Jan De Nul and financed by a loan from KBC Bank, which is based in Belgium. These different phases will add facilities to support the West African oil rig sector, with the aim of establishing Takoradi as a centre for the regional hydrocarbons industry (see Energy chapter).

In August 2014 GPHA director-general Richard Anamoo announced plans to develop a third port in the country due to space limitations at Tema and Takoradi. At the time of publication, there were few details available – even the location is as yet unspecified – and this is likely to be a project for the longer term. Nevertheless, Anamoo said that the new port would serve both the oil industry and strengthen Ghana’s position as a regional trade hub.

Down The Track

Ghana has a modest railway network, with parts of it falling into neglect and operations well below potential. Currently, it handles less than 2% of all passenger and freight traffic.

The mainline system forms a triangle between Accra, Kumasi and Takoradi, with the partly operational Kumasi-Takoradi Western Railway acting as a key natural resource route currently used for transporting bulk minerals, most notably bauxite and manganese. The condition of the track has deteriorated significantly however, such that the Ghana Bauxite Company has abandoned rail transport altogether, in spite of it being considerably less expensive than road haulage. Further, the Ghana Manganese Company has said that it may follow suit. The present condition of the railway network is thus hurting the mining industry and also putting greater pressure on the country’s already-clogged roads.

Making Promises Real

Redevelopment is long awaited, with consecutive governments promising to rehabilitate and extend the system, even committing to the goal of increasing the track from 947 km to 4000 km by 2047. A $10.4bn deal with the Export-Import Bank of China sealed in 2010 was intended to include cash to develop the Western Railway, but progress has stalled. Transport industry insiders told OBG that they have seen little movement on plans to develop an overarching railway master plan, including a proposal slated to begin in 2015 for the redevelopment of the Western and Eastern Railway lines (the latter running between Accra and Kumasi) to create a 668-km network of rehabilitated rails.

Local officials insist that they are committed to developing the rail network. In January 2014, President John Dramani Mahama pledged that work on the system would start by the end of the year.

Gathering Steam

There are promising signs of this, including the successful rehabilitation of the Accra-Tema line, a commuter railway that was overhauled and upgraded to standard gauge in the past decade, including improvements to local stations.

With Ghana’s budgetary constraints in mind, further developments are likely to include PPPs. Indeed, two of the transport projects that the MoT’s PPP unit is overseeing are the rehabilitation of the Eastern Railway and Boankra inland port – both seen as flagship transport projects that have been delayed for too long. In July 2014, the government announced it had selected PwC as the transaction advisor for both projects. The company will undertake initial feasibility studies, develop financial and economic models, and advise on and manage the procurement process.

The Boankra inland port is a 400-acre site near Kumasi that has been cleared for the construction of an intermodal dry port to take pressure off Tema and ease the transportation of goods to northern Ghana and the countries beyond. The concept behind the port is to allow goods meant for the hinterland to be transported directly to Boankra from the ports for Customs clearance and processing before being dispatched to other destinations. Work started in 1996, but the project has been stalled by land disputes and shortages of funds. Syed Naved Uz Zafar, managing director of Maersk, told OBG, “Given Ghana’s population, location and volume of goods transported, there is certainly scope for an inland dry port. Dry docks take less time to construct but will require complementary development of the railroads.”

Regional Advantages

Boankra’s development is often linked to Ghana’s overarching goal of strengthening its position as a regional trade centre, particularly for seaborne transport for the landlocked countries to the north, which include Burkina Faso, Mali and Niger. While it already serves as a major import and export centre for its northern neighbours, it is increasingly facing stiff competition.

Ghana has the natural advantage of its coastline as an access point for landlocked countries to the north. Nonetheless, it cannot capitalise on this alone, as several neighbouring coastal countries, including Côte d’Ivoire, Togo and further afield Nigeria and Senegal, also hold potential as key transit points.

To stay ahead of the pack, Ghana will need investment, political will and administrative capacity deployed in areas such as planning and high-level expertise. The country also requires collaboration between the public sector, responsible for much infrastructure and regulation, and the private sector players in the logistics sector.

“Ghana is making strides to establish itself as an important gateway to the West African market,” PwC said in its 2013 report “Africa Gearing Up”. The consultancy firm elaborated that “key supporting factors are its abundant natural resources, economic liberalism and track record of political stability.”

In 2013, Tema handled 620,668 tonnes of transit cargo, up from 530,457 tonnes in 2012, but below the 750,000-900,000 tonnes it was processing in the middle of the last decade. Of that volume, the lion’s share, 464,104 tonnes, went to Burkina Faso, which directly borders Ghana to the north, with 49,606 tonnes going to Mali and 47,974 tonnes to Niger. Another 58,984 tonnes went to other countries.

Traffic to Mali in particular has fallen considerably over the past 10 years, from 416,883 tonnes in 2003. Mali borders both Senegal and Côte d’Ivoire, both of which function as more natural seaborne trade outlets for the landlocked country than does Ghana.

For the time being, no port has yet established itself as a clear frontrunner for a maritime hub in West Africa. Abidjan was once seen as the regional powerhouse, but armed conflict in Côte d’Ivoire in 2011 undermined this potential; substantial amounts of traffic were subsequently re-routed through Ghana.

Stiff Competition

Tema is a natural candidate for a regional hub, but long delays at the port and shaky inland infrastructure often deter shippers. As a result, transport sector players in Ghana have become concerned that the country will continue to lose its edge to rival ports. For example, although Ghana was able to attract significant business away from Côte d’Ivoire, many of these shippers returned to the latter country following the end of the crisis. Additionally, many neighbouring countries are upgrading facilities and have been conducting aggressive marketing campaigns that have lured potential customers away from Ghana’s ports.

Tolaram Port at Lekki is expected to open in 2015, and will be Nigeria’s deepest port, with a draught of up to 16.5 metres. The port has the potential of being scaled to an annual capacity of 2.5m TEUs and 2m tonnes of dry bulk, while servicing vessels with liquid cargos of up to 160,000 deadweight tonnes. The existing Lagos Port Complex is at present extremely congested, and Tolaram is expected to alleviate the pressure and potentially catalyse Nigeria’s development as the region’s shipping hub.

Meanwhile, Senegal has contracted the management of the Port of Dakar to Dubai Ports World (DPW), one of the world’s major port companies, including the responsibility of developing a new “Port of the Future” with 1.5m-TEU capacity. Some of Ghana’s neighbours also have competitive advantages in inland transportation, particularly railways, an area in which it will take significant time and investment for Ghana to catch up. Moreover, Ghana is one of the few countries in the region to rigorously enforce ECOWAS limits on road transport axle loads of 11.5 tonnes for single-load carrying axles.

“Ghana faces serious competition as a transit country,” Conship’s Vasnani told OBG. “Senegal has invited DPW to the country and also has the advantage of a functioning rail line all the way to Bamako, Mali. Côte d’Ivoire is a fierce competitor as well. This is because, like other francophone countries along the coast, they have a linguistic tie to the landlocked countries of Burkina Faso, Niger and Mali.”

Still Work To Do

According to the LPI, average lead times for the supply chain going from point-of-origin to port or airport for export is four days, and the cost for a 40-foot dry container averages $2259. Meanwhile, the equivalent figures for imports are five days and $1856. Additionally, according to PwC, the wait between unloading and exiting a port is usually two to three days at efficient ports, but the average in sub-Saharan Africa is 14 days.

Given that long wait times are a common feature of African ports, Tema could gain a tangible competitive edge by reducing the length of hold-ups. This would involve both increasing physical port capacity (potentially including substantial redevelopment or relocation), as well as directly reducing the length of Customs procedures.

Customs procedures are rather tedious, with 45% of import shipments physically inspected. While several countries have even higher percentages, others have significantly lower figures. For example, Togo and Senegal inspect 18% and 14%, respectively, of imports. In the US, the proportion is 4%.

Furthermore, while Customs and tax procedures for imports directly to Ghana are clearly defined, those for transit to third countries are a “grey area”, Mohamed Tabch, station manager for logistics company Aramex, told OBG. “This means that in-transit shipping can take three to four days in Ghana. In a region with few flight connections, three to four days is too long to wait. There are not enough available planes to wait around that long,” he said.

Outlook

As Ghana’s economic growth accelerated towards the end of the last decade, some aspects of transport infrastructure did not keep pace – an understandable lag, as GDP was expanding at some of the highest rates in the world. In response, the government has made improving transportation a priority, specifically to support domestic growth, increase the standard of living of Ghanaians and enhance the country’s position as a regional trade centre.

Over the coming years, a range of transportation projects will move forward, with PPPs likely to become increasingly important. The private sector is set to take a key stake in developments including rail, road, ports, the Boankra inland terminal and, potentially, a new national airline (see analysis). While public resources remain somewhat limited, private financing can play a growing role. As well as capacity increases and improvements to infrastructure, boosting inter-modality should be a priority. While it faces growing competition regionally, Ghana can continue to capitalise on its liberal economic approach.

You have reached the limit of premium articles you can view for free.

Choose from the options below to purchase print or digital editions of our Reports. You can also purchase a website subscription giving you unlimited access to all of our Reports online for 12 months.

If you have already purchased this Report or have a website subscription, please login to continue.