Economic slowdown in Morocco pushes banks to diversify their offerings

The banks of Morocco rank among the largest on the continent, with a regional footprint matched only by South Africa’s biggest lenders. Recent years have seen these institutions deepen programmes for small and medium-sized enterprises (SMEs) and expand cashless transactions. However, that is not to say that the industry is not facing some significant challenges. Having dealt with the issue of depressed liquidity levels a number of years ago, the banking sector is now faced with low lending growth and rising levels of non-performing loans (NPLs).

This said, the country’s banks are both well provisioned and well capitalised, and the regulatory authorities continue to take measures to boost stability, including the ongoing implementation of a new banking law passed in 2014. Early 2017 will also see the opening of the kingdom’s first Islamic banks, a prospect that is bringing new foreign investment into the sector and should help to boost already high levels of financial inclusion by regional standards.

Major Players

According to the latest figures from the central bank, Bank Al Maghrib (BAM), as of June 2015 there were 19 onshore banks and six offshore banks operating in Morocco. The three largest banks – Attijariwafa Bank, the Banque Centrale Populaire (BCP) Group and Banque Marocaine du Commerce Extérieure (BMCE) – accounted for nearly two-thirds of industry assets (65.6% of the total).

Attijariwafa Bank is the largest of the three main players, with assets of Dh411.1bn (€37.7bn) in 2015, up 2.3% on 2014. The main shareholder in the institution, which was created in 2004 through a merger of Banque Commerciale du Maroc and Wafa Bank, is the royally controlled holding group Société Nationale d’Investissement (SNI), with an ownership stake of 47.9%. In 2010 SNI said that it was planing to reduce its stake in the bank, and in 2014 it was reported to have engaged advisers for the sale of a 19% ownership share. However, in March 2016 the group said that it had dropped its plans and that it intended to maintain its current shareholding.

The BCP Group consists of the Banque Centrale Populaire itself and 10 regionally-based cooperative banks, in each of which BCP possesses a 52% equity stake, as well as various foreign and non-banking units. The group’s total assets stood at Dh280bn (€25.7bn) in 2015, up 5.2% year-on-year (y-o-y). BMCE’s largest shareholder is the domestic firm FinanceCom, which holds a 36.41% share in the bank (29.93% via fellow group member the RMA Watanya insurance company). French retail bank Banque Fédérative du Crédit Mutuel Groupe and Moroccan state-backed investment fund the Deposit and Management Fund (Caisse de Dépôt et de Gestion, CDG) also hold sizeable stakes, at 26.21% and 8.46%, respectively. In 2015 the bank had total consolidated assets of around Dh279bn (€25.6bn), up 13% y-o-y.

New Entrants

In spite of the large number of lenders already operating in the sector, several new entrants are expected, in part as a result of the passage of a new banking law in 2014 that provides a regulatory framework for Islamic banking – known locally as participative banking. A sharia financial board has been established to ensure compliance, and BAM is currently reviewing seven applications for new lenders, including subsidiaries from Emirates National Bank of Dubai and Masraf Al Rayan of Qatar, along with joint ventures from Qatar International Islamic Bank and Morocco’s Crédit Immobilier et Hotelier Bank; Bahrain’s Al Baraka and BMCE; and US-based Guidance Financial Group and BCP. The first of these should be up and running by early 2017 (see analysis).

The sector has also seen a number of new arrivals to the conventional market. In 2010 the country’s post office launched Al Barid Bank, offering one of the largest branch networks, while more recently the sector saw the entry of CFG Bank, which was created through the transformation of local investment bank CFG Group into a universal bank that opened its first retail branch in March 2016. As of the end of May 2016, the bank had a total of six branches, three of which were located in Casablanca, two in Rabat and one in Fez. At the end of the first half of 2016 CFG had built up a loan book that was worth a total of Dh795m (€72.9m) as well as customer deposits of Dh2.19bn (€200.8m). A bank representative told local media in June of that year that the institution intends to extend its branch network to eight branches by the end of 2016 and to around 20 by 2020.

CFG Bank is also building a network of standalone automatic teller machines outside of bank branches that in addition to cash withdrawals will provide services such as cash and cheque deposits. The bank plans to have ten such facilities in place by the end of 2016. In addition, the institution aims to recruit around 40,000 clients over the course of the next four years, via both an internet banking platform and a branch network of around 20 outlets.

Indicators

The IMF describes the financial sector in its 2015 Article IV Consultation with Morocco as “well capitalised and profitable”, noting that the overall banking capital adequacy ratio was 13.8% as of June 2015, well above Basel III minimum requirements. The body also highlighted that banks have access to stable sources of funding. Furthermore, the fund’s financial sector assessment programme found that “aggregate capitalisation levels would remain adequate under adverse scenarios”, and that threats to financial sector stability were limited as a result.

Overall net banking income stood at Dh10bn (€916.9m) for 2014 as a whole and Dh5.5bn (€504.3m) for the first half of 2015, down 8.7% y-o-y, amid a fall in equity return from 12% in mid-2014 to 10.5% a year later. Lending rates in the sector were falling more slowly than BAM’s benchmark rate, however, leading to a rise in net margins that should boost sector profitability in 2016. Most mortgages in the country are also long-term, fixed-rate products, further boosting profitability at a time of falling interest rates – though high levels of sector liquidity as a result of strong deposit growth and weaker credit growth in recent years have simultaneously led to heavy competition on rates, putting downward pressure on margins.

The Moroccan banking sector suffered from tight liquidity in the early years of this decade due to factors such as rising national current account and fiscal deficits. However, the situation has improved over the last two years as both deficits have fallen. In consequence, the sector’s liquidity needs fell from Dh68.4bn (€6.3bn) in December 2013 to Dh40.6bn (€3.7bn) a year later, and again to Dh16.5bn (€1.5bn) by the end of 2015. By April 2016 banks were seeking a weekly average of around Dh6bn (€550.1m) of liquidity from BAM, and the IMF in its February 2015 Article IV Consultation report suggested that liquidity pressures might disappear entirely in 2016.

Indeed, the challenge for some banks is to now deal with excess liquidity as a result of rising deposits and low loan growth. Total outstanding bank lending stood at Dh768.5bn (€70.5bn) as of March 2016, up 1.3% on the same month a year prior, and the value of outstanding loans grew by 2.8% over the course of 2015, compared to growth of over 10% in 2011. Credit to households has been driving loan growth, having expanded at 3.4% over the 12 months to March 2016, compared to 0.5% for lending to companies. Consumer credit in turn is driving household borrowing; consumer loans were up 5.6% y-o-y in March by outstanding value, well ahead of mortgages on 1.9%. The total value of outstanding household credit stood at Dh286.4bn (€26.3bn) in March, while loans to businesses were worth Dh375bn (€34.4bn).

Lending

Mehdi Chakir, financial analyst at CFG Bank’s investment arm, cited two main factors for the corporate sector’s lending slowdown. “At the end of 2014, major real estate developers had a large stock of unsold units, so they stopped production and moved towards a strategy of generating cash, which led to a fall in loans to developers. Furthermore, the majority of short-term operating loans made by banks were to cover delays in the payment of fuel subsidy refunds to fuel providers. However, since petrol subsidies ended and a reduced budget deficit allowed the state to make payments more easily, these too have fallen off,” Chakir told OBG. Meanwhile, Mamoun Tahri-Joutei, director of economic intelligence at BMCE, said that lending to parastatal firms had declined in 2015 due to less dynamic public investment.

Rising NPL rates have also caused banks to reduce lending. “Available data show that the slowdown in lending is mainly explained by a drop in demand coming from companies in a context of low non-agricultural activities, in particular since 2013, and the strong uncertainties that surround the economic recovery of our main trade partners,” Hiba Zahoui, deputy director of the Banking Supervision Directorate at BAM, told OBG. “Credit supply by the banking sector has also lowered as credit risks have risen,” Zahoui said, adding that the general economic slowdown being faced by the country was also putting downward pressure on credit provision.

BAM has worked to facilitate talks between the banking sector and the General Confederation of Moroccan Companies to help resolve the issue. Among measures the bank has suggested are efforts to reduce the widespread problem of payment delays by companies to their suppliers (see Economy chapter). Mohamed Tahri, deputy director-general at Société Générale Maroc, said banks were also seeking a number of regulatory changes to help boost lending growth, notably including reforms that would allow banks to finance both value-added tax arrears and regional investment in a more secure fashion.

The outlook for 2016 is mixed. Chakir told OBG that he expected household credit to continue to grow faster than corporate lending in 2016. Tahri echoed this sentiment saying, “more and more banks are orienting themselves towards the retail segment, which will continue to see growth in the coming years”, citing the development of the kingdom’s middle class and professional segment, which have been less affected by the country’s economic slowdown than the corporate sector. However, he also pointed out that the banks’ growing interest in financing the economy and the needs of the industrial and real estate sectors in particular was giving rise to heavy competition, which is putting pressure on margins. “Margins have become very small, against a backdrop of a rise in the cost of the risk,” Tahri told OBG.

Rising NPLs

Since 2010 NPLs have been rising and were equivalent to 7.7% of outstanding bank loans in March 2016, up from 6.9% a year earlier and 7.3% at the end of 2015. The financial difficulties at Moroccan oil refiner Samir have contributed to this increase, as the assets of the company were seized by the tax authorities in August 2015, ahead of the firm’s liquidation the following June. Problems in the steel industry resulting from overcapacity from exporters to Morocco have also caused banks to reclassify loans to domestic steel companies, though none have had to default yet. In addition, NPLs are particularly high in the hotel and restaurant sector (around 21%). However, while NPLs continued to grow in 2015, the rate of expansion tapered, due in part to the slowdown in lending. Provisioning levels are also relatively high, at 66% as of June 2015. “Banks are very prudent regarding provisioning for NPLs,” Chakir told OBG; a phenomenon due in part to close regulatory scrutiny.

“As a regulator we are making sure NPLs are covered by the necessary provisions, levels of which we review regularly, and we are also encouraging banks to proactively identify portfolios at risk before they become distressed in order to both monitor and provision for them,” Zahoui told OBG, arguing that the recent rise was a normal part of the regular economic cycle and that BAM was keeping an eye on the issue.

Regulatory Reform

In 2014 Parliament approved a new banking law, which has brought a range of changes to the sector since being promulgated in 2015, most notably the establishment of an Islamic banking segment. The reform also created a new category of payment institutions, obliging banks to appoint independent administrators to their boards, while expanding the powers of BAM’s System Risk Surveillance Committee. Zahoui, speaking in April 2016, told OBG that BAM was continuing to work on a range of circulars implementing the law, the last of which will be finalised in 2017. Also in April BAM introduced new rules requiring banks to provide some banking services for free and to reduce commissions on lending. Furthermore, the authorities are working on gradually imposing Basel III standards on the sector, although most lenders already exceed the key requirements mandated by the Basel standards.

Zahoui told OBG that BAM was also working on new regulations on how banks classify restructured loans, after several major loans made by the sector had to be restructured, as well as drafting a new rule that will define loan defaults more closely in line with international standards, which she said the bank expects to be ready by the end of 2016. In order to reduce risks associated with concentrated lending, the bank is also introducing new information requirements for banks lending to business groups under which banks will need to collect consolidated information on the entire group’s finances as well as those of the individual company being lent to. Lastly, the government is working on a draft central bank law, which would bolster BAM’s supervisory powers and resources, in line with IMF recommendations.

SME Financing

Credit can be problematic for local companies, with respondents to the World Economic Forum’s “Global Competitiveness Report 2015-16” rating access to finance as the largest obstacle to doing business in the country. This is the case for SMEs in particular, with difficulties in recouping debt from SMEs leading banks to demand collateral from them that they often do not possess. “Banks that are competing heavily to find and finance value-creating projects nonetheless seek guarantees in light of the difficulties involved in recovering debts,” said Tahri.

In spite of this, the situation is good by Middle Eastern and African standards, with SMEs accounting for 38% of lending. “SMEs’ access to credit has long been less of a problem in Morocco than in other countries, and has improved a great deal in recent years,” said Tahri-Joutei. “The issue is not really about the availability of financing, but rather about banks being able to find good projects to back, and SMEs becoming more transparent and efficient in some areas.”

The industry is working to further improve such access, with some banks increasingly focusing on the very small enterprise (VSE) segment as part of wider efforts to carve individual business niches for themselves. Attijariwafa Bank, for example, has started to develop a rating system for firms that could help with the development of the segment.

Loan Guarantees

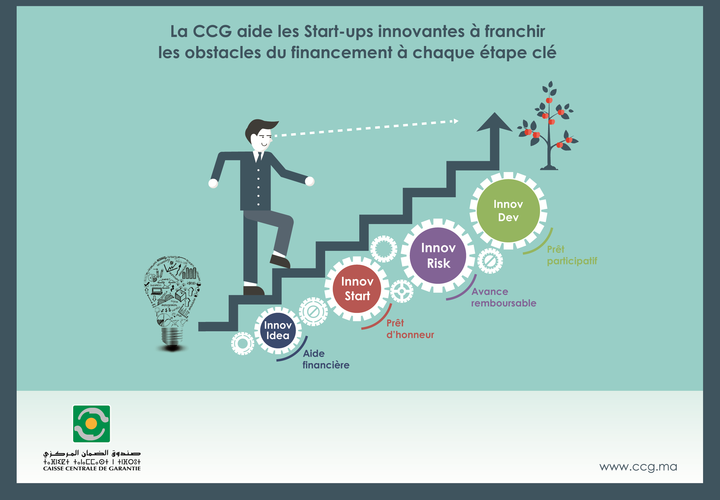

The Central Guarantee Fund (Caisse Centrale de Garantie, CCG), created in 1949, was designed as an incentive instrument for investment in the economy, and aims to contribute to economic and social development. In addition to guaranteeing and co-financing companies, since 2003 the CCG has guaranteed mortgages, assisting with the purchase of approximately 250,000 residences to date. In 2009 it set up a new strategic development plan as part of the recast of the national system of guarantees for SMEs, in which the state plays a central role by relying on the CCG.

The institution offers a range of products that meet the needs of SMEs throughout their life-cycle, including guarantees for up to 70% of the value of commercial bank loans to newly established firms, and up to 60% for established companies. These guarantees now account for approximately 80% of the CCG’s activities. To improve the efficiency of the disbursement process, the body leaves the decision-making for guaranteed loan issuances worth less than Dh1m (€91,700) to the bank in question. The CCG also participates in co-financing activities – that is, direct lending to firms in cooperation with banks – amounting to around Dh1.4bn (€128.4m) in loans in 2015. Most of this co-financing is aimed at companies suffering from the widespread problem of delayed payments from clients (see Economy chapter).

Additionally, an SME support fund to help companies facing financial difficulties was launched in June 2014 by BAM, the Moroccan Banking Association and the CCG, and works to encourage investment in SMEs by providing funding alongside them, while allowing the capital in question to take the entirety of investment returns below a certain threshold. The CCG made total commitments of Dh6.8bn (€623.5m) across 5240 transactions in 2015, up from Dh1.99bn (€182.5m) in 2010. The institution appears to have had a major impact on the availability of credit for SMEs, and according to a study carried out by professional services company Deloitte, 81% of firms benefitting from its support would not have been able to raise adequate financing otherwise. The study also found that for every Dh1 (€0.09) invested in the fund by the government, the authorities received a return of Dh2.8 (€0.26) from direct and indirect tax receipts. “VSEs nowadays offer the best incremental growth opportunities for the banking system, which has adapted to better meet the needs of these customers,” Hicham Zanati Serghini, director-general of CCG, told OBG. “Thanks to the CCG’s guarantee, we observe a bank’s downscaling strategy in terms of loans granted to this category of enterprises.”

The state has continued to work on a range of initiatives to improve SMEs’ access to credit along with the wider business environment in which they operate. These include a mechanism put in place by BAM in 2013 under which it agreed to provide banks with additional liquidity – which was in high demand at the time – if they lent to SMEs, while penalising institutions that did not. To date around Dh15bn (€1.4bn) has been lent under the strategy. Between 2007 and 2014 BAM also conducted three separate awareness campaigns on financial issues encountered by VSEs.

The administrative council of the newly created Moroccan Observatory for Very Small, Small and Medium-Sized Enterprises also held its first meeting in June 2016. The body, which is presided over by the governor of BAM, will collect data on SMEs and VSEs, including information on the business environments they function in and their access to financing.

Non-Bank Lending

There were 34 non-bank financial institutions operating in Morocco as of mid-2015, including 16 consumer credit firms, six leasing firms and two real estate lenders. Kamal Benkiran, director of studies at the Professional Association of Finance Companies (Association Professionelle des Sociétés de Finances, APSF), said that non-bank lenders – many of which are subsidiaries of banks – have been facing rising competition from banks over the past decade. “Competition from banks will become increasingly intense in the coming years,” he told OBG.

The value of total outstanding consumer credit country-wide stood at Dh42.7bn (€3.9bn) in 2015, up 0.4% on the previous year, according to figures from the APSF. The total included Dh23.1bn (€2.1bn) of personal loans and Dh19bn (€1.7bn) of car loans. Consumer credit NPL levels stood at 12.6% in 2015, down from 13.2% a year earlier. New consumer protection rules affecting the segment came into force in April 2016. Among the changes, lenders now have to make loan offers to customers in writing and allow them up to a week to respond, which according to Benkiran will slow down the lending process.

Outstanding leasing credit was Dh42.6bn (€3.9bn) in June 2016, up 1.7% y-o-y, of which real estate leasing contributed a total of Dh15.95bn (€1.5bn). Chakir told OBG that the sector was experiencing a slowdown due to decreasing levels of investment by firms and a simultaneous decline in the retail market, though the car-leasing segment had picked up in 2015.

Mohcine Boucetta, deputy director general of Morocco-based Sogelease, expects the domestic leasing market to change and become more sophisticated. “The market could use specialised players that provide leasing services aimed at specific segments,” he told OBG. “There is likely to be demand for such specialist firms, which represents a future business opportunity for the industry.”

Distribution Numbers

There were 11.8m bank cards issued in the kingdom across 2015, up 8.1% on 2014 figures, with 6529 ATMs in existence countrywide, up 4.6%. Card payments are continuing to grow quickly, and the total value of these transactions stood at Dh22.9bn (€2.1bn) in 2015, up 9.6% y-o-y. Internet banking is also well developed in the kingdom and continues to expand.

Payment Systems

Payment activity is set for further development in the wake of the 2014 banking law, which created a new category of deposit-only payment institutions. These will be permitted to take customer deposits and offer a range of payment solutions, such as pre-paid cards, mobile payments and electronic transfers, while being forbidden from offering credit. These institutions will be allowed to establish branches of their own, and use networks of both their own dedicated agents and independent agents, which will allow customers to make deposits and withdrawals. Speaking in April 2016, Asmaa Bennani, director of payment systems and financial inclusion at BAM, told OBG that the bank had received a number of applications for licences and that the first institutions were expected to be up and running by the end of 2016. “The establishment of the new institutions will help with the development of payments in Morocco and with our strategy to reduce the amount of cash in circulation. It will also help to boost financial inclusion for people who do not want to use a bank,” she said, citing BAM research highlighting that some potential customers found banks intimidating. BAM’s Committee of Credit Establishments approved two circulars about the creation of the aforementioned institutions in June 2016. Recent regulatory changes will also allow for mobile-to-mobile payments in 2017.

Financial Inclusion

The degree of involvement of citizens in the formal financial system has expanded rapidly in recent years. The banked population was 62% as of June 2014, according to data from BAM, up from 50% at the end of 2010. According to the World Bank’s Global Findex database, this is one of the highest levels in Africa. This swift improvement has stemmed in part from a strategy launched in the late 2000s by BAM that saw a wide range of changes aimed at boosting inclusion, including requirements for banks to provide around 20 basic banking services for free and to abolish minimum deposit requirements for customers opening new deposit accounts. The creation of Al Barid Bank, the kingdom’s postal bank, through the award of a banking licence to the Moroccan post office, has also helped expand the banking branch network into underserved rural areas. At the end of 2014 Al Barid Bank had 5.4m accounts, equivalent to around 16% of the total population.

Bennani told OBG that the central bank was also working with the Ministry of Economy and Finance on the creation of a new three-year comprehensive financial inclusion strategy, which she said should be ready by the end of 2016. The launch of Islamic banking is also set to at least slightly raise levels of financial inclusion by bringing in new customers unwilling to participate in the conventional banking system.

Microcredit

Morocco has one of the region’s best-developed microcredit industries, though the wider microfinance sector remains more of a work in progress, with micro-insurance still in the early stages of development and microcredit institutions forbidden from taking deposits, preventing the emergence of a micro-savings industry. The sector is tightly regulated, and all micro-loans, the maximum permitted size of which is currently Dh50,000 (€4580), must be used for productive purposes only, with consumer microcredit forbidden. Furthermore, only nonprofit institutions are allowed to issue micro-loans in Morocco. While there has been some discussion about allowing private companies into the segment, the future of such plans remains unclear.

There are 13 microcredit associations operating in Morocco, four of which – Al Amana, Fondation pour le Développement Local et le Partenariat, Fondation Attawfiq and Fondation ARDI – have a presence across the whole country, while another, Bab Rizq Jameel, has a presence limited largely to rural areas. The value of microcredit loans issued in 2015 stood at Dh6.37bn (€584m), spread across 911,000 active sector clients (around 55% of whom are women and 15% of which are youths), up 2.8% on the previous year. By sector of economic activity, 58% of such loans went to commerce, 21% to handicrafts, 15% to services and 6% to agriculture. Following rapid growth in the early 2000s, the industry faced financial difficulties around the time of the 2008-09 global financial crisis, which saw one institution collapse and the authorities step in to prevent wider contagion. The segment has recovered since then; its overall NPL ratio stood at 4.8% as of June 2015, down from 5.1% a year earlier, and well below peak levels of 9% reached in mid-2009.

The sector’s representative body is the National Federation of Microcredit Associations, which in 2012 put in place a strategy for the development of the sector, under which it is seeking to raise the amount of outstanding microcredit loans from Dh6.37bn (€584m) in 2015 to Dh25bn (€2.3bn) by 2020 and the number of active clients to 3.2m. The authorities have also taken various measures to support micro-lending, including the creation of a development fund called Jaïda, which is operated by state investment fund CDG and seeks to facilitate access to financing for microcredit associations, including by raising money of its own to lend directly to them. Total outstanding financing provided by the institution in 2015 was worth Dh824m (€75.6m), down 6% on the 2014 figure, as the fund seeks to encourage associations to diversify their sources of financing. Around 80% of financing for the segment already comes from commercial banks, in contrast to some other countries in the region where providers are reliant mainly on financing from donors and multilateral institutions.

Outlook

It remains to be seen when faster growth will return to bank lending in Morocco. However, continuing regulatory reform will help the stability of the system, and banks’ continuing expansion abroad, as well as the launch of Islamic banking and new payment institutions, will help to maintain profits, bring major new banking actors into the kingdom, diversify the sector’s product offering and help boost financial inclusion levels that are already high by regional standards. “Moving forward, digitisation and alternative credit, or Islamic financial services, represent new trends to which the sector must adapt,” Laila Mamou, CEO of Wafasalaf, a consumer credit firm, told OBG.

You have reached the limit of premium articles you can view for free.

Choose from the options below to purchase print or digital editions of our Reports. You can also purchase a website subscription giving you unlimited access to all of our Reports online for 12 months.

If you have already purchased this Report or have a website subscription, please login to continue.