Tunisian CEOs Optimistic amid a Slow Recovery

01 Feb 2018

Seven years after the revolution, Tunisia continues to work on consolidating economic growth, with recent activity in a variety of sectors suggesting the country is making good progress towards this goal.

After being heavily affected by a damaged image and the UK’s travel ban, which ended in mid-2017, tourism has grown by more than 20% in the last year. This is due to both the return of visitors from traditional source markets and a new wave of arrivals from China – whose citizens no longer require a visa – and Russia.

Within the agriculture sector, another key driver of the economy, the government aims to boost olive oil production, with the crop in the midst of a promising season and output expected to grow by 160%.

Furthermore, Tunisia is eager for its industrial sector to become a technological leader in the region. In November I had the opportunity to moderate a panel on Industry 4.0 at the Tunisia Investment Forum together with the Italian-Tunisian Chamber of Commerce, and I saw first-hand that from the automotive industry to mechatronics, agri-business and pharmaceuticals, progress has been made in implementing new technologies.

On the back of muted GDP growth of around 1% in the 2015-16 period and 2.3% in 2017, according to IMF estimates, the business society and public sector are reconsidering their economic objectives, and how they think local companies and ecosystems should develop.

To investigate further, Oxford Business Group has launched its first OBG Business Barometer: Tunisia CEO Survey, based on face-to-face conversations with over 100 CEOs. Having checked the results, I can say that business leaders in Tunisia know this is a decisive moment.

More than two-thirds of the executives we talked to said that increased instability in neighbouring countries would be most likely to impact the economy in the short to medium term. Libya to the east is at a critical juncture, and as one of Tunisia’s main trading partners, sustained stability there would ultimately translate into numerous economic benefits for Tunisia. Meanwhile, difficulties experienced in other countries in the wider region, such as Egypt and Turkey, could favour Tunisia, at least in terms of tourism.

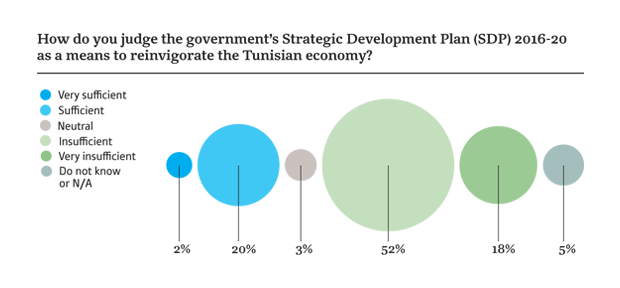

Our survey shows that the debate to define the economic identity of Tunisia is under way. As can be seen in the infographic below, more than half of respondents judged the Strategic Development Plan 2016-20 as insufficient to reinvigorate the economy, having yet to see the launch of any projects from the plan, while 18% said it was very insufficient and only 20% considered it sufficient.

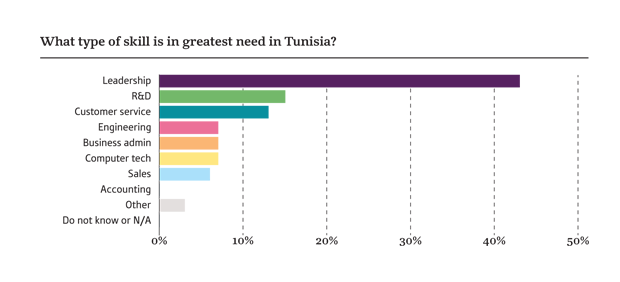

However, C-suite executives seemed willing to invest in the future: 81% reported they were either likely or very likely to make a significant capital investment in the next year. This finding is somewhat paradoxical in a country that claims a lack of leadership: around half of CEOs named leadership as the skill in greatest need, followed by research and development (15%), and customer service (13%). Leadership was also the most in-demand skill among businesspeople in Algeria, for which OBG published its first CEO Survey in November 2017.

In the face of a reportedly insufficient development plan and rising public debt, those surveyed were more upbeat about business transparency, with 72% rating it either as high or very high relative to the region.

![]()

However, there are calls for urgent tax reform, which will undoubtedly continue to be an area for improvement. Almost two-thirds of respondents said the tax environment is either uncompetitive or very uncompetitive on a global scale. Indeed, corporate tax was raised recently, and the informal economy remains strong. In line with this, 60% said access to credit is either difficult or very difficult.

The survey shows that there are a number of national-level needs, including the revision of industrial policies. Meanwhile, the local governments that emerge from the May elections will play an important role in the development and formalisation of both local ecosystems and small and medium-sized enterprises.

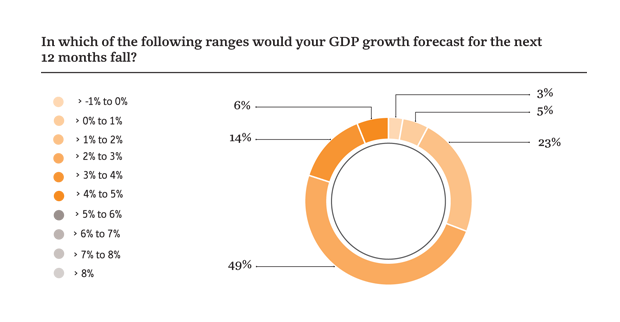

In the near term, CEOs are relatively optimistic: 77% have either positive or very positive expectations of local business conditions in the next 12 months, and approximately half forecast GDP growth of between 2% and 3% over the same period, with the IMF predicting the latter figure will hit 3.03% this year.

Covid-19 Economic Impact Assessments

Stay updated on how some of the world’s most promising markets are being affected by the Covid-19 pandemic, and what actions governments and private businesses are taking to mitigate challenges and ensure their long-term growth story continues.

Register now and also receive a complimentary 2-month licence to the OBG Research Terminal.

Register Here×