Oman prepares for a sustained period of lower oil revenues

Having endured low oil prices for the entire year, countries across the resource-rich GCC saw their balance sheets constrained in 2015. In Oman’s case, lower revenues from the petroleum sector led to a nominal GDP contraction of 13.8% and the country’s largest deficit in more than a decade. Closing the fiscal gap is a top priority for the government, whose ambition extends beyond the short-term issue of funding to restructuring the entire economic base. Spending cuts, taxation reform and boosting private sector activity will all play a part in this process, which is likely to preoccupy authorities for years to come.

Because the influence of crude oil prices on nominal GDP figures is greatest in countries with the largest hydrocarbons sectors, balance sheets in these economies are often examined in current-price terms – hence Oman’s National Centre for Statistics and Information (NCSI) does not regularly release inflation-adjusted GDP figures. According to the IMF, however, the real GDP growth rate in the sultanate was 3.3% in 2015, an improvement on the 2.9% recorded a year earlier. The IMF projection for 2016 was 1.8% in its most recent “World Economic Outlook” report, published in October 2016.

Oil Conundrum

Oman is not alone in facing the challenges brought on by a new economic reality. Budget shortfalls recorded in 2015 and 2016 have compelled governments across the GCC to revise their economic strategies, reining in spending where possible and seeking new sources of revenue in an effort to balance the books.

Oman’s net oil revenues in 2015 contracted to OR5.66bn ($14.7bn), despite a 5.4% increase in export volumes to 308m barrels. Revenue losses were commensurate, with a decline of 45.3% in the average price realisation for Omani crude, which stood at $56.50 per barrel in 2015, down from $103.20 the previous year. This suffering was felt across the GCC and oil-exporting countries of MENA, which the IMF reported lost more than $340bn in oil revenue, or around 20% of their combined GDP.

Diversification of economic activity away from oil and gas has been a key ambition of every GCC country for decades, though some have moved further towards that goal than others. The possibility of an era of low oil prices has brought greater urgency to the undertaking. Some countries, such as Saudi Arabia, have initiated reform processes which, if successfully implemented, are far-reaching enough to be of historical significance.

Five-Year Plan

In Oman, which since the 1970s has seen a less-volatile growth trajectory than some of its neighbours, the response has been moderate. The country is in the early stages of deploying its ninth five-year plan (FYP) covering 2016-20 – the final component of Vision 2020, a blueprint for social and economic development launched in 1995. The FYP was devised with an eye to the new economic reality, and its principal hallmarks – as is the case with strategies across the region – are modest assumptions regarding medium-term growth and a greater emphasis on private sector participation.

The plan is based on an average oil price of $55 per barrel, compared to an actual average of $95.60 between 2011 and 2015. This projection accounts for what the government anticipates will be 2.8% average annual GDP growth rate in constant prices over the five-year period, compared to 3.3% over the previous five years. In past years, oil and gas revenues in Oman have usually accounted for around 90% of state revenues, so the low-price scenario the government has planned for will place considerable constraints on its capacity to spend.

More than half of the OR41bn ($106.5bn) in targeted investment, therefore, is to be derived from the private sector, to be deployed in projects such as the South Batinah Logistics Area, the Oman National Railway, tourism facilities within Port Sultan Qaboos, a number of fishery projects, Al Dhahirah Special Economic Zone (SEZ) and Port of Shinas. “Given the current oil price, the Omani government should press forward with the public-private partnership financing model for many of the large-scale infrastructure projects,” Ernst Grissemann, managing director of Bauer Nimr, told OBG. “Not only does this provide for the participation of the private sector, but it takes the financing onus off the government.”

To mitigate future economic shocks from oil price volatility, the FYP sets an ambitious target of reducing oil’s contribution to GDP from an average of 44% seen in the 2011-15 period to 26% by 2020. To this end, institutional changes are afoot – notably the establishment of a general department within the Supreme Council for Planning (SCP) tasked with coordinating with ministries and specialised institutions. The FYP also outlines several medium-term objectives, such as maintaining the inflation rate at an average of 2.9%, and developing the contribution of small and medium-sized enterprises (SMEs). Inflationary pressures in 2015 calmed considerably, with the consumer price index at 0.1% for the year and an average of 2.5% recorded in the 2010-14 period.

Fiscal Matters

While Oman’s hydrocarbons resources are expensive and technically difficult to extract, the revenues it brought allowed the government to run near-balanced budgets from 2010 to 2013. In 2014, however, the effects of sinking oil prices began to become apparent in the national accounts, and the government ran a fiscal deficit of OR1.06bn ($2.8bn), equal to 3.4% of GDP. In 2015, as oil prices hit a new low, the deficit reached OR4.63bn ($12bn), or some 17.2% of nominal GDP, according to the Central Bank of Oman (CBO). IMF projections predict the same shortfall for 2016.

Oman’s current account swung from a surplus of OR1.6bn ($4.2bn) in 2014, representing 5.2% of GDP, to a deficit of OR4.2bn ($10.9bn), the equivalent of 15.4% of nominal GDP, a year later. In its “Financial Stability 2016” report, the CBO described expectations of further deficits in both the country’s budget and current account. These twin deficits carry profound implications for the economic stability of the sultanate. A prolonged current account deficit could force Oman to dip into its foreign reserves if it is to retain the dollar currency peg that has served it well for decades – as the CBO has indicated it intends to do. How long the nation’s external buffer – which stood at some $16.7bn in January 2016 – will allow the CBO to keep this commitment depends on the price of oil and the government’s ability to mitigate its fiscal situation through reform.

Cutting Costs

The obvious starting point in tackling a structural fiscal deficit is trimming government spending, and in this regard Oman has already made substantial progress. While Vision 2020 and the FYP represent the state’s medium-term response to the nation’s deteriorating external position and growing budget deficit, Oman began to cut some of its costs early in 2016, starting with fuel subsidies.

In January 2016 the government revised its price mechanism for petroleum products to reflect global oil prices, thereby reducing a subsidy burden that cost it nearly OR1bn ($2.6bn) in 2015. As a result, prices for regular-grade fuel rose from 114 baisa ($0.30) per litre to 140 baisa ($0.36), while super grade fuel went from 120 baisa ($0.31) per litre to 160 ($0.42). Diesel also rose from 146 baisa ($0.38) per litre to 160 baisa ($0.42).

Over the course of 2016, Oman has approached the difficult topic of public sector salaries by focusing on reducing benefits attached to government jobs. Over a dozen agencies – including the Public Authorities for Electricity and Water, Telecommunications, and Civil Aviation, and the Capital Market Authority – have cut bonuses and other perks, such as life, health, travel and car insurance, and loans and allowances for housing, school fees and mobile phones. Other areas where the government has successfully implemented spending cuts include defence and capital investment by civil ministries. Taken together, this broad cost-cutting exercise is expected to reduce state spending in 2015 by $3.8bn, or 5.5% of GDP. More such measures are expected in 2017.

Regarding utilities, the Authority for Electricity Regulation intends to raise electricity prices for large government, industrial and commercial users from the start of 2017, introducing a higher tariff for customers who consume more than 150 MW annually. According to the government body, this consumer segment accounts for around 20% of power subsidies each year, meaning that the increased tariff could save the state some OR100m ($259.7m) on its yearly bill. Residential consumers are not expected to face any tariff changes in the short term.

Boosting Revenue

As well as cutting costs, Oman is seeking ways to boost revenue as a means of reducing its fiscal deficit. As in the wider GCC, the sultanate is renowned for its low tax burden; there is no personal income tax for residents or foreign nationals, and until 2016, companies outside the hydrocarbons sector paid a modest 12% on income over OR30,000 ($77,900). The corporate tax rate for companies operating in oil and gas exploration is 55% on any income derived from petroleum product sales. Capital gains are taxed as ordinary income, and profits from the sale of listed shares are exempt from taxation. There is no payroll tax, and stamp duty only applies to the purchase of real estate at 3% of the sale value. In terms of social security, employers must contribute an amount equal to 10.5% of their Omani employees’ monthly salary to cover pension, disability and death benefits, as well as 1% of employees’ monthly salary for industrial illnesses and injuries. The sultanate’s unobtrusive tax framework has helped underpin the growth of companies operating there. The possibility of a prolonged period of low oil prices, however, has thrown the sustainability of this approach into doubt. As a result, the coming years are likely to see some significant changes to Oman’s taxation framework.

In 2016 the upper chamber of the consultative council, known as the Majlis Al Dawla, and the lower chamber – the Majlis Al Shura – agreed to remove the OR30,000 ($77,900) tax-free ceiling for businesses operating in Oman and increase the corporate rate from 12% to 15%. The move is expected to net the government an additional OR125m-250m ($324.6m-649.3m) per year, though the authorities have said SMEs will be protected from the rise.

While the sensitive issue of personal taxation has not yet been addressed, Oman’s residents and businesses will soon feel the effects of another major tax initiative. In February 2016 GCC ministers finally signed off on the long-anticipated framework for a value-added tax (VAT), which will be implemented across the region from January 1, 2018. Though each member state is free to establish its own exemptions from the tax, global accounting firm EY estimates that the 5% level recently agreed upon could bring Oman OR250m ($649.3m) in extra revenue, or 1.4% of GDP (see analysis). A mooted 2% levy on remittances made by expatriates, meanwhile, is not expected to be introduced in the short term. The World Bank’s “Doing Business 2017” report found that taxation of all kinds in Oman represented 23.9% of state profits, significantly higher than in Bahrain (13.5%), Saudi Arabia (15.7%) and the UAE (15.9%).

Bridging The Gap

Oman has taken concrete steps to address its fiscal deficit, but its cost-cutting and revenue-raising efforts to date are not sufficient to close the fiscal gap in an era of low oil prices. The sultanate has therefore had to consider other funding options in a bid to meet its financial obligations. In October 2015 Oman issued its first sovereign sukuk (Islamic bond), which, with a minimum subscription of OR500,000 ($1.3m), was aimed at domestic fund managers, banks and other sophisticated investors. The OR200m ($519.4m) five-year offering was based on the popular ijara sukuk format – whereby the instrument effectively functions as a leasing arrangement – and drew 22 orders over the subscription period. As well as raising crucial funds for the government, the sale was widely welcomed in the market as a much-needed instrument for Islamic banks, takaful (Islamic insurance) operators and sharia-compliant funds to manage their liquidity more effectively. The sovereign sukuk has also been listed on the Muscat Securities Market, where it will provide a benchmark for any Omani institutions that wish to issue Islamic bonds.

As well as issuing domestic debt, in the summer of 2016 Oman went to the international bond market for the first time since 1997. The sultanate offered $1bn in five-year notes at a yield of 245 basis points over the benchmark mid-swap rate, as well as $1.5bn in 10-year bonds at a spread of 320 basis points. The return to the markets came despite an ambivalent assessment of the economy by the major credit rating agencies in the months leading up to it: Standard & Poor’s gave Oman a “BBB-/A-3” rating in May 2016, and in the same month Moody’s downgraded the country’s rating to “Baa1”, placing it at the lower-medium grade in investment terms.

Nonetheless, according to the CBO, Oman’s net public debt position is lower than in other GCC countries, and the international markets remain open to it. However, the IMF estimated in 2015 that without further fiscal adjustment or a significant recovery in oil prices, the task of financing the projected cumulative fiscal deficit to 2020 would “exhaust fiscal buffers and raise debt to about 25% of GDP, or increase government debt to over 70% of GDP by 2020 if buffers were to be preserved”. The fiscal reforms of 2016, therefore, are likely to be just the beginning of a longer-term restructuring of the economy.

Inflation & Monetary Policy

While the removal of subsidies is often associated with inflation spikes, which carry both political and economic risk, the effects of Oman’s process of subsidy reform are mitigated by a benign global inflationary environment and a relatively elastic supply of foreign labour. With inflation (based on the average annual consumer price index) rising by almost 0.75% during the first half of 2016, the CBO has been able to maintain an accommodative monetary policy stance, even making revisions to the reserve requirement for the sultanate’s banks to facilitate larger lending volumes (see Banking chapter).

The Omani rial is pegged to the dollar at $1:OR0.3849, a rate that has remained unchanged since 1986. As with other GCC states, this arrangement has suited the sultanate well over recent decades. While a floating exchange rate might be beneficial in terms of producing more stable fiscal revenues in nominal rial terms, the dollar peg has been helpful in enabling Oman to build stable trade relations as an oil exporter. Moreover, the peg to the world’s reserve currency has removed the risk of speculative bubbles in domestic currency that small countries are generally exposed to.

The dollar peg strategy, however, comes at a price, by making foreign reserves necessary to maintain the exchange rate. This does not represent a significant challenge to commodity-based economies like Oman’s if revenues are strong, but the oil price decline means that rather than expanding, the nation’s external buffers are being eroded. Questions about the ability of GCC countries to maintain the dollar peg have led to an elevated degree of speculation on regional currencies over the past year. Oman’s rial, which is protected by one of the smaller foreign reserves in the Gulf, is no exception: in early 2016, one-year dollar/rial forwards – currency deals to be settled after 12 months – jumped to their highest levels since 2006. The CBO, however, was quick to respond, stating that its commitment to the dollar peg remained unchanged.

Oil & Gas Receipts

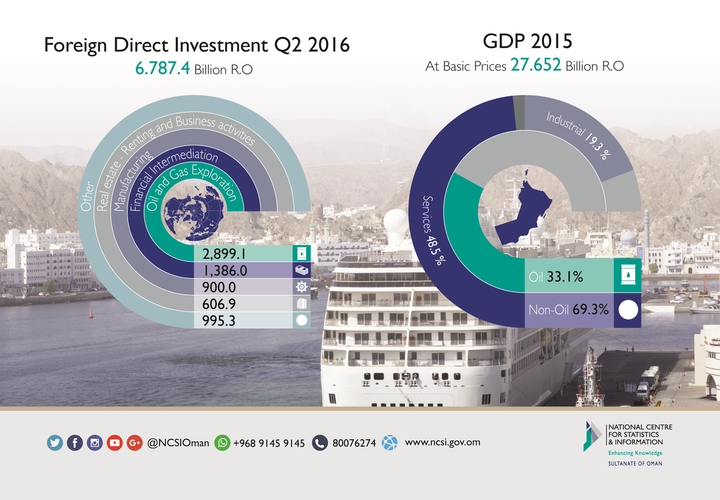

Although economic diversification is the state’s long-term ambition and oil prices continue to be relatively low, hydrocarbons revenues still play a central role in Oman’s economy. Between 2011 and 2014, oil and gas income accounted for 84% of annual government revenues on average, according to the CBO. The low oil price environment that has prevailed since mid-2014 has reduced the contribution of the hydrocarbons segment to total government revenues, but at 78.7% it was still the single biggest component in 2015. The sultanate has continued to expand crude oil production in recent years, and in 2015 it grew by 4% to reach some 358m barrels (see Energy chapter).

Maintaining and even increasing production is important not only in terms of revenue, but also because oil and gas extraction underpins many of the activities that Oman is keen on developing to diversify its economy, including the production of petrochemicals and aluminium, power generation, and water desalination. These segments form the core of the sultanate’s manufacturing base, which the government is committed to expanding. To this end, the Vision 2020 development strategy has set the target of boosting manufacturing’s economic contribution to 15% from the 4% recorded in 1996 when the plan was launched.

While there is some way to go before this target is attained – in the first half of 2015 manufacturing contributed 9.3% to GDP – the average annual growth rate of the segment throughout the lifetime of the eighth five-year plan was 18.4%. A large share of future manufacturing growth will be associated with the $6.4bn Liwa Plastic Industrial Complex, a project that has received the majority of its funding from international financial institutions. When it comes on-line in 2020, the facility will allow Oman to produce polyethylene for the first time, provide 13,000 jobs and support the development of a downstream plastics industry.

Transport and logistics is another sector earmarked for growth over the short term. The government intends to leverage the country’s geographic location and see it act as a redistribution hub for East and Central Africa, with the target of placing Oman in the top 30 of the World Bank Logistics Performance Index by 2020. In 2016 the sultanate ranked 48th out of 160 economies, behind the UAE (13th), Qatar (30th) and Bahrain (44th), but ahead of Saudi Arabia (52nd) and Kuwait (53rd). “Markets in East Africa present a great opportunity for Oman because of their rapid economic growth and geographical proximity,” Imaad Al Harthy, assistant general manager for insurance at the Export Credit Guarantee Agency (ECGA), told OBG. “Ethiopia in particular has serious growth ambitions and a large population, which may help Oman boost its non-oil exports.”

Transport & Sezs

Key projects in transport and logistics include the development of the port town of Duqm in central-eastern Oman. Eight integrated components will eventually make up the SEZ at Duqm, including Oman’s newest port, an industrial area, a residential zone, a fishing harbour, a tourism centre, a logistics hub, a central business district, and an education and training area. The Special Economic Zone Authority Duqm (SEZAD) manages, regulates and develops all economic activities in Duqm. “SEZAD has the benefit of being essentially a one-stop shop for investors, and all of the approvals can be done internally without the need to consult other governmental entities,” Yahya bin Said Al Jabri, chairman of SEZAD, told OBG. “This has worked in SEZAD’s favour, and we have seen significant interest from many large-scale international investors, with numerous agreements already signed.”

The 95-sq-km Al Batinah South Logistics Area set for completion in 2030 will be another fillip to the industry, and has attracted significant interest since it was first unveiled in 2013 by the SCP. As a flagship logistics hub, the area will have zones dedicated to multimodal connectivity, light industries, commercial services, warehousing and logistics.

Tourism

The Ministry of Tourism (MoT), meanwhile, aims to expand the contribution of tourism to GDP to 5% in 2020 and anticipates the creation of 100,000 employment opportunities by 2024. Estimates from the “Economic Impact of Travel and Tourism 2016” published by the World Travel & Tourism Council (WTTC) differ somewhat from government forecasts, with direct tourism’s contribution expected to rise from OR696.9m ($1.8bn) and 2.5% of GDP in 2015 to OR1.34bn ($3.5bn) and 3.4% by 2026. In terms of total contribution, the WTTC sees the sector moving from OR1.59bn ($4.1bn) and 5.7% of GDP in 2015, to OR3.02bn ($7.9bn) and 7.7% in 2026. Regarding employment, the industry directly supports 53,000 jobs, as per the report, and accounts for 2.7% of total employment, with the WTTC predicting this will rise to 81,000 jobs and 3.9% of employment in 2026. Job creation is a key benefit of this labour-intensive sector, and with more than 39 tourism projects under way in 2015, foundations are being laid for significant employment growth in the sector.

Target Growth Sectors

Fishing has long been an economic staple in Oman, and the fisheries industry was earmarked as one of five key sectors with the potential to drive economic diversification in the FYP. Current plans envisage a production boost of 200,000 tonnes by 2020, which will bring total annual output to 480,000 tonnes and provide an additional 20,000 jobs. Major projects in the sector include a fishery harbour in Duqm and an adjoining industrial fisheries cluster (see Construction chapter).

Mining, which accounted for 0.4% of GDP in 2014, is also expected to see an increase in activity over the coming years. The sector showed 10.3% growth in 2015, boosting its GDP contribution to 0.5%, and a new mining law is expected to attract investment in segments such as gold, copper and rare earth. The sector will also stand to benefit from the mineral processing and refining facilities being developed in Port of Duqm’s industrial zone.

If the government’s ambitions are met, these key sectors will play a major role in the restructuring of the Omani economy – a development that will be welcomed by the business community. “Oman for many years was focused on using its oil revenues to invest in basic infrastructure. Now that these needs have been more or less met, it is time that we take steps to move towards a more mature and sustainable economy,” Fawzi Hamed Al Harrassy, executive director of local construction group Teejan, told OBG.

Trade

Expanding the manufacturing base, and thus the range of potential exports, is recognised as a crucial undertaking in this period of low oil prices. Export volumes fell by 33.4% in 2015, throwing the current account into deficit and challenging Oman’s ability to maintain its peg to the US dollar. Reducing the dominance of oil and gas exports, which make up 59.4% of exports, is therefore a priority, and one that Oman is relatively well positioned to meet thanks to its high degree of trade openness.

Chemicals and related products took the largest share of non-oil exports in 2015, followed by minerals and plastic rubber products. All these categories, however, showed declines in export volumes that year due to reduced demand from the GCC and China. Several smaller export segments bucked the trend with modest expansion over 2015, including foodstuffs, beverages, tobacco and related products (up 4.4%), and animal or vegetable fats and oil (up 1.2%).

Export Promotion

While external factors bear heavily on Oman’s ability to boost both its traditional and emerging export lines, further trade activity can be facilitated by the ECGA. An independent legal entity despite being fully funded by the state, the agency has promoted non-oil exports since its founding in 1991 through its credit insurance, guarantee and financing services. These services are available to Omani exporters of any size, operating in any industrial, commodity or services segment. The ECGA insures exports to 108 countries, though with nonoil exports Oman’s focus has historically been more narrow: the UAE, Saudi Arabia and India were the three top destinations for non-oil exports of Omani origin in 2015, making up a combined 42.4% of them. Diversifying the nature and destination of Oman’s exported goods is therefore central to addressing a trade balance that is currently particularly subject to the vicissitudes of the oil market.

Investment

As the FYP acknowledges, Oman’s ability to diversify its economy, boost exports and broaden its revenue base lies to large degree in its ability to spur private investment. In its most recent annual report, the CBO noted that such investment was held back in 2015 by a backdrop of economic uncertainty. Prior to the slowdown, however, Oman had taken useful steps to boost investment. Several free zones have been developed since 1999 – including the SEZ of Duqm, Sohar Port and Freezone, Salalah Free Zone and Al Mazunah Free Zone in Dhofar – offering benefits such as tax holidays, lower Omanisation requirements, up to 100% foreign ownership and waivers, and reduction of corporate tax and Customs duties. In addition, the Public Establishment for Industrial Estates has operated since 1993, and oversees eight sites that offer incentives such as exemptions from income tax and Customs duties, as well as state loans for fisheries, agriculture, health and traditional handicraft activities.

The government has also turned its attention to boosting investment in smaller businesses, which it hopes will provide much-needed jobs for Oman’s youth. In 2014 it invested some OR100m ($259.7m) in an SME development fund, known as Al Naama, that offers entrepreneurs debt financing of OR50, 000-300,000 ($129,000-779,000). Piloted at 10 colleges in its first year, the programme will be available at higher education institutions by 2017. As well as providing fiscal aid, it is equipping smaller firms with crucial business know-how – for example, addressing the problem of poor accounting skills by working with consultancy KPMG to produce tailor-made software for local SMEs. By 2016 the platform was being used by 68 companies with local support from KPMG staff. The fund aims to build on this initial success and involve other global accounting firms in the initiative.

Elsewhere, the CBO has advised Omani banks to formulate a liberal SME lending policy, urging them to extend credit to SMEs at low interest rates, reduce other costs as far as possible and allocate 5% of their total credit to the segment (see Banking chapter). In terms of investment sources, the SCP estimates that foreign direct investment will grow by an annual average of 11% between 2016 and 2020. To achieve this, the government is taking steps to improve the investment climate, such as by removing the minimal capital requirement for new businesses. With Oman having risen three positions to 66th of 189 economies for ease of doing business in the World Bank’s “Doing Business 2017” report (see analysis), it can be argued that these moves are having an effect.

Outlook

Oman’s economic performance remains vulnerable to the direction of oil prices over the medium term. Although Brent crude climbed above the $50 mark in the first half of 2016, the outlook from most observers is a cautious one; Saudi Arabian investment firm Jadwa foresees the possibility of oil prices edging higher, but with any increase being marked by volatility. Jadwa’s Brent forecasts for fiscal years 2016 and 2017 stand at $44 and $55 per barrel, respectively. Prices at this level would mean the continuation of Oman’s fiscal deficit, which it is expected to meet by dipping further into its reserves and issuing more sovereign debt. To bridge fiscal shortfalls in this manner over the medium term is the most critical challenge the government faces. Over the longer term, the sultanate’s ability to reform its economic base will be central to its future stability.

You have reached the limit of premium articles you can view for free.

Choose from the options below to purchase print or digital editions of our Reports. You can also purchase a website subscription giving you unlimited access to all of our Reports online for 12 months.

If you have already purchased this Report or have a website subscription, please login to continue.