Dubai taking innovative steps to become a major maritime centre

With a strategic position near the Strait of Hormuz, Dubai has always been a natural location for a port serving its hinterland, and the emirate has a longstanding maritime tradition. Furthermore, following the development of Jebel Ali Port, which now has the largest man-made harbour in the world, Dubai has emerged as a serious player in the global maritime industry. However, the emirate has ambitions that go well beyond its famous port. The authorities want to build a maritime cluster that can rival Singapore and Hong Kong in terms of breadth and depth.

Indeed, with the aspiration of attracting the leading international companies across the whole spectrum of maritime business – from shipbuilding and repairs, to brokerage, insurance and ship ownership – the government has introduced a series of initiatives and strategies to position the emirate at the forefront of the global industry.

Government Strategy

The government of Dubai has placed a greater emphasis on the maritime sector in the last decade and has been keen to point out its substantial contribution to economic growth and development in the emirate.

The sector currently is an important employment generator within the emirate’s economy and creates more than 75,000 jobs, with operations, engineering, and ports and shipping accounting for more than three quarters of all jobs in the sector.

Consequently, the emirate is emerging as a highly competitive global cluster. However, it has some way to go to match the world’s leading maritime centres. While Dubai’s maritime industry adds Dh14.4bn ($3.92bn) in economic value, Hong Kong’s contributes Dh41.1bn ($11.2bn), Singapore’s Dh67.8bn ($18.5bn) and Norway’s Dh95.1bn ($25.9bn). Similarly the industry in these centres has a greater impact in terms of employment generation, creating some 222,000 jobs in Hong Kong, 167,000 in Singapore and 101,000 in Norway. Nonetheless, the emirate has grand ambitions to join the ranks of these leading players. “We have done benchmarking with the world’s top maritime clusters and centres. Singapore is a great model to learn from; we work together with Singapore on many fronts and we see where we stand in terms of weaknesses and strengths,” Nawfal Al Jourani, director of communications at the Dubai Maritime City Authority (DMCA), told OBG.

Driving Growth

Under the stewardship of the DMCA, the regulatory body for the sector founded in 2007, the emirate is highlighting the maritime industry as a leading engine of economic growth and promoting the city as an ideal location for maritime companies to establish operations.

The framework for this is laid out under the Dubai Maritime Sector Strategy, a white paper that outlines the goals of the authority in broad terms. These include creating a more robust regulatory regime, introducing a thorough licensing system, promoting the emirate to the global industry, pushing smart technology in the sector, maintaining high-quality infrastructure and developing local human capital.

These long-term goals are now pursued in conjunction with other plans including Dubai Maritime Vision 2030 and Dubai Strategic Plan, and the DMCA has begun to make inroads on the first two goals, namely regulation and licensing.

For example, the agency has introduced a number of regulations and initiatives in the field of environment and safety, including the designation of the international company Monjasa as the official oil spill responder for the emirate; a safety campaign aimed at ship operators; a sustainability programme with an emphasis on the reduction in harmful emissions; concerted efforts to improve feeder traffic flows at Dubai ports; and new speed limits for marine crafts in the emirate’s waters.

Legal Developments

One of the most important recent initiatives by the DMCA is the introduction of a new arbitration centre for the maritime industry in Dubai. The announcement of the Emirates Maritime Arbitration Centre (EMAC) in September 2014 is a welcome step forward in introducing a legal framework for the regional industry.

Indeed, the arbitration centre is the first initiative of its kind in the Middle East.

“Generally, arbitration is not something that is used very much in the region, but it is something that the UAE, as a growing maritime cluster, could benefit from,” Lars Seistrup, managing director of Damen Shipyards Sharjah, told OBG. The DMCA is confident that the new centre will meet a growing demand in the region. “As a result of the volume of sea trade here, we know for sure that there’s a great need for arbitration,” Jourani told OBG.

The timeline for the EMAC to become operational is yet to be announced; however, the role the body will play has been laid out. Dispute resolution and deliberation will be based on a legal regime drawing from best practices around the globe and is designed to give parties access to a range of maritime regulatory guidelines and standards. The centre will be equipped to hear cases across a range of industry segments, including cargo shipping, shipbuilding and repairs, assurance and reinsurance, loss adjustment, marine collisions and affreightment.

While the EMAC will meet an existing need, it is hoped that the development of a well-defined legal environment will also draw more business to the emirate. Amer Ali, executive-director at the DMCA, told the local press upon the launch of the EMAC that, “Dubai’s maritime community has long expressed a growing need to attract and recruit more ship owners into the emirate, since they will represent the basic foundation of a successful maritime industry.” According to Ali, the EMAC is one step that will help achieve this goal.

Strength In Depth

Such initiatives are one of the primary reasons that Dubai and the UAE remain dominant players in the regional maritime industry. In the next three years, the UAE’s maritime sector is expected to be worth $66bn and contribute as much as 35% to Middle Eastern investment in the sector.

As well as a strong regulatory environment, the UAE’s – and Dubai’s – success has been built on a foundation of substantial infrastructure capacity. Sultan Ahmed bin Sulayem, chairman of the DMCA, told the local press, “The maritime industry has been developed through increased investment towards building the capacity of seaports, airports, free zones, logistics and Customs administrations to cope with a remarkable rise in Dubai’s foreign trade, which soared to [a] record high of $361bn in 2013. This is nine times higher than its value in 2000. Such growth is being upheld through continual expansion of ports, particularly the Jebel Ali Port, which will take its total handling capacity to 19m twenty-foot equivalent units (TEUs) early in 2015.”

Another component of Dubai’s infrastructure that continues to expand is the development of Dubai Maritime City (DMC). The project, a 2.27m-sq-metre district, has space allotted for mixed-use real estate development, yacht marinas, and an industrial precinct for shipbuilding and repairs.

Gulf Craft, a yacht manufacturer, announced in October 2014 that it would invest $100m to develop an approximately 900,000-sq-ft shipyard facility. In addition, DMC also experienced an uptick in the number of real estate development announcements on site in 2014. This includes office space that will be leased to ship owners, ship management companies, and marine protection and insurance companies at preferential rates.

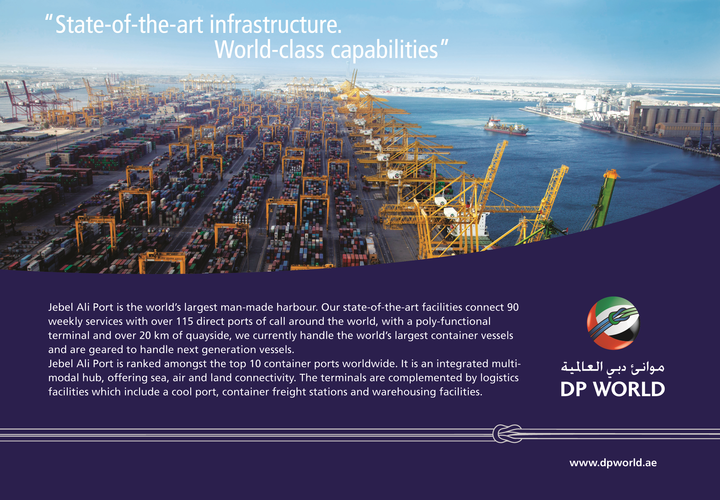

Ports

First conceived by Sheikh Rashid bin Saeed Al Maktoum in 1976, Jebel Ali has become one of the leading sources of growth for the emirate. The container port currently has 23 berths and 78 quay cranes, with the $850m Terminal 3 adding six more berths to bring the total capacity to 19m TEUs by 2015. The general cargo terminal has 26 berths and a total storage area of 1.4m sq metres.

The port continues to go from strength to strength. The expansion of Jebel Ali’s Terminal 2 by 1m TEUs helped Dubai’s ports, which include Mina Rashid and Mina Al Hamriya, to achieve a record year in 2013, handling 13.6m TEUs, a 2.7% increase on 2012.

Moreover, Jebel Ali took the title of world’s most productive port, according to the US-based Journal of Commerce. The port achieved 138 moves per vessel per hour (MPH), beating 438 other ports included in the worldwide study. Jebel Ali was also found to be the most efficient port in terms of handling large ships, achieving 163 MPH for container vessels of 8000 TEUs or more.

Remaining Competitive

As the largest container terminal between Rotterdam and Singapore, and one of the 10 largest in the world, Jebel Ali has become a model for development for several countries in the GCC region.

Saudi Arabia and Oman, in particular, have moved ahead with plans to build port capacity that could offer an alternative to Dubai and position these countries as logistics centres for the region.

According to the consulting group AT Kearney, GCC port capacity will increase by more than 200%, or 70m TEUs, in the next two decades.

As such, there is likely to be overcapacity in the region. Jebel Ali, however, has a pedigree that will make it difficult to challenge. Jorn Hinge, president and CEO of United Arab Shipping Company, told OBG, “Despite substantial investment in new ports and related infrastructure expected to come on-line in the next few years throughout the GCC, the maturity, volume and sophistication of Jebel Ali Port combined with the neighbouring free zone will make it difficult for other ports in the Gulf to persuade shipping lines to shift business.”

Others in the sector agree: “With Jebel Ali, they are significantly ahead of the demand at any point in time,” Kapil Mehta, head of trade and marketing for the UAE, Oman, Qatar and Iran at Maersk, told OBG. “We might see some deterioration of throughput through Jebel Ali because infrastructure around the region will grow, but at this time it is difficult to see any other countries being able to take an entire network of ships at their port.”

Consolidation

While regional ports could offer a cost discount on Jebel Ali, the port is price competitive on a global scale, according to Mehta. As such, there seem to be few threats to its regional dominance in the medium term.

Yet the port is unlikely to recreate the stellar rise that it experienced in the last decade. Between 2003 and 2012, Dubai ports, led by Jebel Ali, recorded a 150% growth in volumes, increasing from 5m TEUs to 13.3m TEUs in 2012.

With the port firmly established on the world stage, such rapid growth is unlikely to be repeated in the next decade. “For now, we are looking at the cluster as a fairly mature market. GDP growth will determine containerised growth and we expect it to be in the single digits,” Mehta told OBG.

Indeed, while the port has built strong capacity in terms of draft and berths, an excess is likely to remain for some time. Mehta says, for example, that there are no immediate plans for the Triple-E, Maersk’s 18,000-TEU capacity line of ships, to call at Jebel Ali, though the shipper may revise this based on how things develop in the future.

DP World Investments

Nonetheless, the port remains crucial to the Dubai-based port operator, DP World. In 2013 the performance of its Dubai operations outperformed its global network. The company is now the third-largest ports operator in the world. It has 65 marine terminals around the world and handled 55m TEUs in 2013. In the first quarter of 2014, volumes across its container-handling network increased by 10.5%.

However, DP World is not resting on its laurels. Its core business, container handling, which accounts for more than 75% of company revenues, is expected to grow substantially over the next decade.

Capacity across the company’s container portfolio is forecast to reach more than 100m TEUs by 2020. In June 2014 the operator raised $1bn through a convertible bonds sale, issuing a statement that the funds would be used “to take advantage of organic and inorganic growth opportunities, diversify funding sources and general corporate purposes”.

Joining Forces

Its intention to expand through acquisitions became abundantly clear in September 2014 when P&O Maritime, which is a wholly owned subsidiary of DP World, announced the purchase of a majority stake in a Spanish operator of offshore support vessels for the energy industry, Remolcadores de Puerto y Altura SA (Repasa). The new joint venture under the P&O Maritime brand will give DP World greater penetration in offshore operations of liquefied natural gas, as well as greater access to the markets of the Mediterranean and West Africa. In the same month, it was announced that DP World had expressed interest in investing in the Albanian ports of Durres, the biggest port in the country, and Shengjin, when the chairman of the company, Sultan Ahmed bin Sulayem, accompanied a Dubai delegation visiting the Balkan country.

One month later, the company announced the $25.5m acquisition of World Security FZE, a company that provides security services and solutions to ports and free zones in Dubai.

Shpping Industry

This acquisition spree comes at a time when the global shipping industry is experiencing a sluggish performance. As a result, rates across all segments of the market have been depressed as the number of new-build ships continues to outpace demand.

“New tonnage is expected in the second half of 2015 but an overtonnage situation already exists in the dry bulk sector. The situation has deteriorated due to the slow-down in the Chinese economy in 2014,” Capt. Farhad P Patel, director at Sharaf Shipping, told OBG. Given that there is a time lag between order and delivery, and the strong order book following an initial recovery from the global financial crisis, new inventory is likely to hit the market for some time to come.

Nevertheless, the sector seems to have seen out the bottom of the market. In April 2014, for example, investment group Moody’s revised its outlook for the global shipping industry from negative to stable for the first time since June 2011.

In a statement that accompanied the announcement, Mariko Semetko, Moody’s assistant vice-president and analyst said, “The revision reflects our expectation that the global industry’s aggregate EBITDA [earnings before interest, taxes, depreciation and amortisation] will rise by mid-single digits in percentage terms year-over-year in 2014, in line with our -5% to 10% growth range for a stable outlook.” Although Semetko acknowledged that overcapacity remains a challenge, the agency also said, “Industry conditions are at a trough and the supply-demand gap will not worsen materially. In this environment, we expect the supply of vessels will exceed demand by no more than 2%, or that demand will exceed supply by up to 2%.”

This is good news for a local maritime industry that is reliant on global shipping to stimulate other sectors of the cluster.

In addition to the potential for a global recovery, the local market looks conducive to sector expansion over the next decade. In the medium term, strong economic and demographic growth in the emirate, the federation and the region, in addition to growth in emerging markets serviced by Dubai, should support the whole gamut of maritime businesses from shipping lines and shipbuilding to freight forwarders and shipping brokers.

Financing

In the short term, however, confidence remains fragile. It is hardly surprising, therefore, that in terms of financing, the market has been cautious in the last two years. The liquidity in the bank market and appetite for asset finance returned during 2014, according to Knut Mathiassen, regional head of shipping finance for the Middle East and Africa at Standard Chartered. The bank itself has a significant shipping finance loan book in the Middle East. However, for those that can access loans, the cost of financing has been improving, with the rates on shipping loans falling by as much as 100 basis points since 2010. For a number of companies in need of capital, financing has come in the form of equity. For instance, in November 2010 the US-based private equity firm, Oaktree, acquired a controlling stake in the Emirati company Gulmar Offshore Middle East, which has now been revived as Harkand.

Another success story is Stanford Marine, a Dubai-based operator, acquired by Abraaj Capital in 2007, which prospered during the downturn. The company reported revenue of $237m and an EBITDA of $60.2m in 2013. Abraaj, which bought a 51% stake in the company in 2007, is currently looking to sell its share for a market value of $300m.

Other maritime companies have gone down the route of publicly listing, with Abu Dhabi’s Gulf Marine Services listing on the London Stock Exchange in February 2014. However, Gulf Navigation Holding is at present the only locally listed shipping company. “It has not been easy to raise money for shipping here after the financial crisis in 2009, as it’s been mainly centred on Singapore, New York and Oslo,” Mathiassen told OBG. However, GCC banks are now back in the market giving international banks increased competition, especially Islamic banking institutions.

Outlook

Despite difficult global conditions, Dubai’s maritime industry is growing into a leading economic engine. The emirate’s flagship companies in the maritime sector, DP World and Drydocks World, continue to adapt and thrive despite a depressed shipping market. With the government introducing new regulation and improving the legal environment for maritime operators in the emirate through the DMCA, the prospects of an increase in the footprint of a whole range of sector industries looks strong.

Although ship ownership – as well as maritime financial services from insurance to brokerage – is currently under-represented, this is likely to change in the future as the wider maritime industry in the emirate gains weight and credibility. As such, therefore, indicators for the local maritime sector could start to look a lot more like the leading global maritime clusters of Singapore, Hong Kong and Norway against which the emirate has benchmarked itself.

You have reached the limit of premium articles you can view for free.

Choose from the options below to purchase print or digital editions of our Reports. You can also purchase a website subscription giving you unlimited access to all of our Reports online for 12 months.

If you have already purchased this Report or have a website subscription, please login to continue.