Broadly positive outlook in Kuwait continues, but need for investment reform is clear

01 Oct 2017

View the OBG Business Barometer: Kuwait CEO survey infographic

Of all the comparatively wealthy countries in the region, on a per-capita basis, Kuwait is one of the richest. Its oil wealth per capita is much higher than Saudi Arabia’s, for example, and the government has been prudent in saving over the years, building up its sovereign wealth funds to ensure that future generations benefit from the oil bounty.

So when oil prices took their precipitous downward turn in 2014, Kuwait was particularly well placed to see things through with minimal pain.

Indeed, for a number of years, Kuwait’s annual budget was calculated on a price-per-barrel forecast far lower than any other country in the region. Furthermore, the government stipulates that each year a significant percentage of oil income is channelled directly into the sovereign wealth fund, the Future Generations Fund (FGF). This is typically 10% of net income each year, as well as 10% of government revenue.

A second fund, the General Reserve Fund, plays a day-to-day role in fiscal management, as opposed to the long-term portfolio investment of the FGF. Both of these funds are managed by the Kuwait Investment Authority (KIA).

These funds, and the generous welfare package and public sector employment opportunities Kuwaiti nationals enjoy, have traditionally redistributed the country’s oil wealth, and in many ways still do.

But even in the new era of lower oil prices, which has seen many neighbouring GCC economies tackle the burden of subsidies, it has proven difficult for the government to reduce them in Kuwait: parliament refused to pass a bill in 2016 that would have reduced electricity and water subsidies for nationals. It did, however, pass an amended bill that will see costs increase for expatriates and businesses owned by them.

Boosting government revenue

That said, change is definitely afoot even if slower than some would like: the proposed GCC-wide value- added tax, set to be introduced next year, marks a significant change in Kuwait’s social contract.

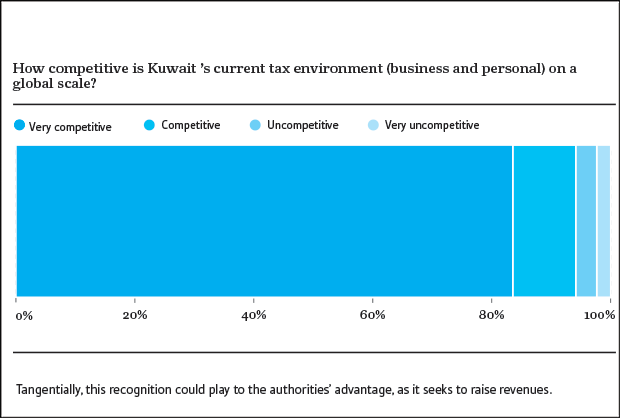

Add to this the introduction of a 10% corporate income tax to replace existing tariffs for foreign businesses and a number of smaller fees for locally domiciled firms, and it will be interesting to see if the current feeling amongst CEOs regarding the tax envronment changes. Oxford Business Group’s latest findings in its Business Barometer: CEO Survey found that 94% feel Kuwait’s tax environment is competitive or very competitive.

Tangentially, this recognition could play to the authorities’ advantage, as it seeks to raise revenues.

A very influential public sector

Perhaps unsurprisingly, the public sector is the employer of choice for nationals. According to the Public Authority for Civil Information, 343,340 Kuwaiti citizens work in the public sector – 80% of all working nationals. By contrast, less than 90,000 work in the private sector, which employs some 2.2m people.

Given the size of the state in terms of revenue generation and state-owned enterprises, our finding – that 45% of respondents said government spending accounted for 60% or more of their business – was striking, if not unexpected.

Developing the private sector into a more significant engine of growth is increasingly pressing, so organisations such as the National Fund for Small and Medium Enterprise Development have their work cut out for them.

It is fair to say that economic reform in Kuwait has not been as highly prioritised as it has been elsewhere in the region, or as urgently pursued until recently. However, huge levels of counter-cyclical infrastructure spending by the government – the $112bn five-year National Development Plan for 2015-20 and a re-energised reform programme, New Kuwait 2035 – are building business leaders’ confidence.

Positive investment outlooks despite transparency concerns

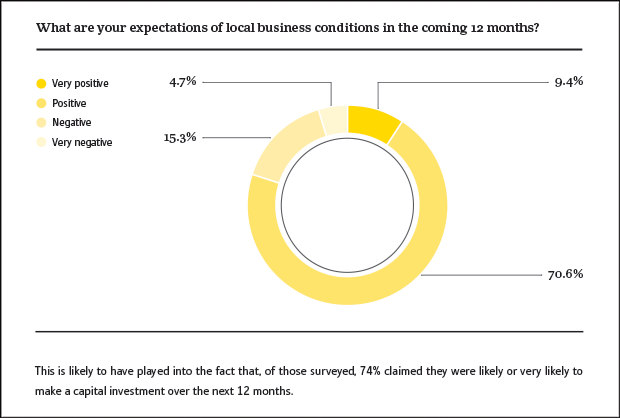

These actions have also pleased ratings agencies, which have given Kuwait an AA rating with a stable outlook. So, whilst the CEOs surveyed by OBG felt that the biggest cause for concern, apart from commodities’ pricefluctuations, was regional instability – something that hits a bit closer to home, given the ongoing dispute within the GCC itself – their outlooks for business conditions for the next year were overwhelmingly positive. Four out of every five respondents reported that their outlooks were either positive or very positive.

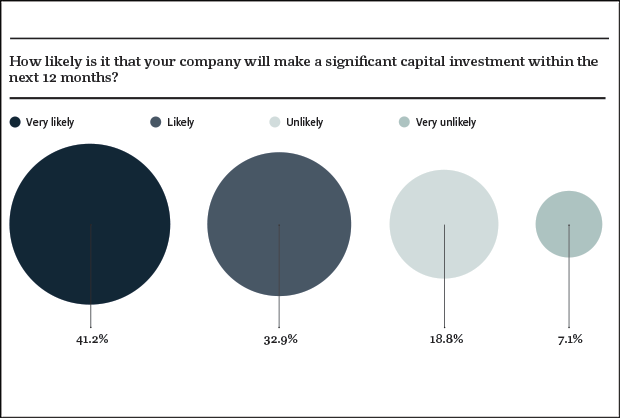

This is likely to have played into the fact that, of those surveyed, 74% claimed they were likely or very likely to make a capital investment over the next 12 months.

Given the level of wealth within Kuwait, it is no surprise that businesspeople may be looking to invest when prices in many quarters are lower: the country is a net exporter of wealth. Furthermore, individuals and corporations alike have long been investors, both regionally in cities such as Dubai, and further afield in London, where uncertainty over Brexit and the weaker sterling have made assets proportionally cheaper than they have been for some time.

CEOs were more circumspect about the level of business transparency in the country: with just over half – 55% – saying the level of transparency was high or very high, in comparison to other countries in the region. This has been noted in the various economic reform programmes the government has created, and further efforts, such as corporate governance, are never far off.

Interestingly, 66% of CEOs surveyed said getting access to credit was either easy or very easy, which bodes well for the private sector.

Increasing need for public support of private industry

Kuwait is relatively insulated from the impact of significantly lower oil receipts. However, whereas it may have been possible in previous downturns to suggest that the country could afford to, and in some respects did, sit on its petrodollar laurels, this is clearly not the current approach.

Businesspeople I spoke with, even relatively recently, frequently voiced frustration at the pace of change, the freeing up of government-owned land for development, and the machinations of parliament, often leaving me to conclude that they felt their successes were more often in spite of government help rather than aided by it.

Indeed, the conclusions of our Business Barometer show a broadly positive outlook from CEOs, but, given the role of the state in Kuwait, more than ever before, government impetus behind reforms and investments needs to be maintained.

Covid-19 Economic Impact Assessments

Stay updated on how some of the world’s most promising markets are being affected by the Covid-19 pandemic, and what actions governments and private businesses are taking to mitigate challenges and ensure their long-term growth story continues.

Register now and also receive a complimentary 2-month licence to the OBG Research Terminal.

Register Here×