Two Takeaways from Our Survey of CEOs in the UAE

23 Jul 2017

View the OBG Business Barometer: UAE CEO survey infographic

World-class infrastructure and tourism offerings, significant financial reserves and a reputation as a safe haven have all contributed to a feeling that despite the various headwinds buffeting the UAE, it is well placed to drive on with reforms intended to ensure long-term, sustainable prosperity.

There are seven constituent emirates that make up the UAE, and while the federal government makes decisions on specific areas – security and foreign policy, immigration and education standards, to name a few – the individual emirates have considerable autonomy over their own affairs.

Each emirate has therefore been able to take its own path. From the industrial base of Sharjah, the hydrocarbons and heavy industry sectors of Abu Dhabi and the services megalopolis of Dubai, the UAE as a whole is one of the most diversified in the region.

However, as with all economies, and in particular those that make up the GCC, sentiment is everything. All of the economic diversification strategies in the region have at their core a dramatically increased role for the private sector, and the UAE is no exception.

In a perfect world, the transition would be a gradual reduction of state-led growth immediately and seamlessly – and replaced by a corresponding expansion of private sector. At this point you’d be forgiven for asking which planet I’m on ….

The point is, rejigging an entire, large and complex economy is not something that sticks to a rigid plan.

What is perhaps the new normal for the price of oil, which has led to an economic slowdown in the region, means that the major reforms to the UAE’s subsidy system and the imminent introduction of a GCC-wide value-added tax (VAT) come at a time when businesses are already feeling the pinch.

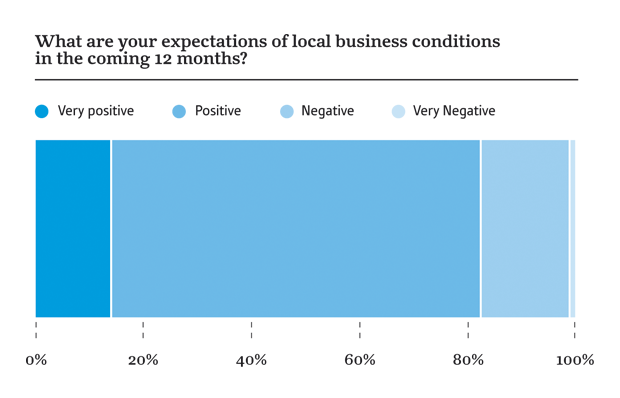

So it is interesting that of the CEOs whom OBG surveyed, 85% of respondents indicated that they were positive or very positive about local business conditions.

Dubai-based companies were slightly more positive in their outlook than those based in Abu Dhabi or Sharjah. This could be the result of a number of factors, not least of which is that these business are more remote from the impact of hydrocarbons prices.

Of the sectors where CEOs had a positive outlook, banking and capital markets, construction and real estate, health, education and ICT were particularly well represented. None of these should perhaps be surprising.

Financial services businesses see opportunity in both bullish and bearish markets: the construction and real estate sectors are continuing to benefit from the government-led infrastructure drive, albeit reprioritised, and health and education are areas where budgets have remained relatively large and demand strong, falling into the all-important social infrastructure bracket.

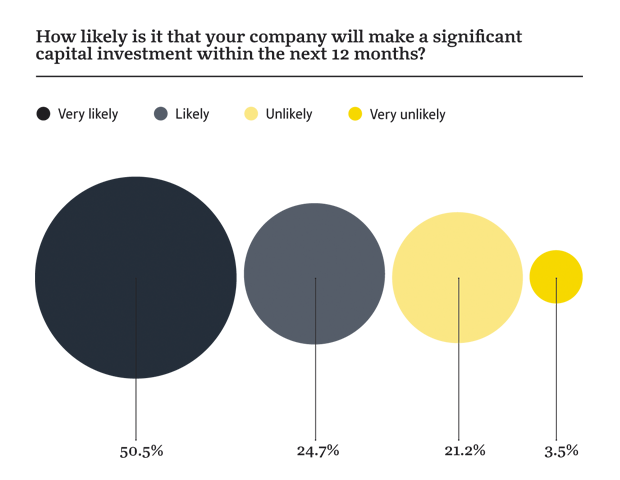

Even among those who expressed a negative outlook, 64% indicated that their companies were likely or very likely to make a significant capital investment in the coming year.

On the face of it this goes against the perceived wisdom. If, as a CEO, you are not confident in the economic outlook, why would you dig deep into your pockets and invest? Perhaps even tap markets?

I think we can draw two important conclusions from this.

First, it speaks to the underlying long-term confidence CEOs have in the UAE. Second, and perhaps more importantly, it underlines identified but as-yet-unrealised potential.

One interesting caveat of our findings is that international-domiciled companies are moderately more positive than locally based ones. Again, there are many possibilities as to why this is the case. However, my conclusion would be that foreign businesses are less invested in the local discussion – the domestic narrative – and look purely at the possibility for return on investment. It therefore again underscores the UAE’s appeal.

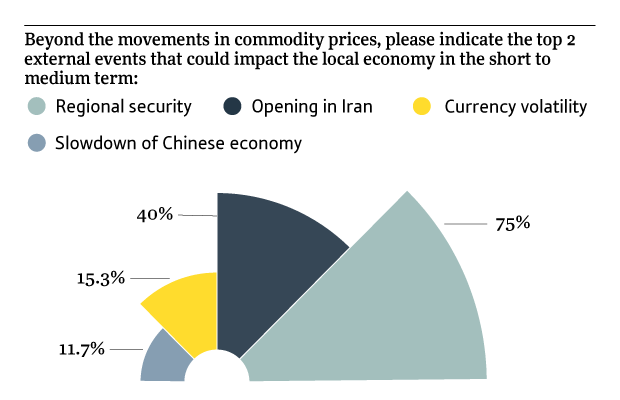

Interestingly of those surveyed, 10% identified slower growth in China and US interest rate changes as top external factors that could impact growth. Topping their concerns, and no surprise here, the CEOs identified regional security as a top worry.

One of these is access to credit, and just over half of respondents – 54% – found this aspect of doing business easy or very easy, whilst 46% said it was difficult or very difficult. The reason that such a relatively high proportion are finding it difficult may well be a reflection of tightened liquidity within the banking sector, as well as a reluctance to lend to small and medium-sized enterprises – important elements of the Vision 2030 goals. That said, it was interesting to note that there was no particular difference in whether a company was large or small as to how they responded.

While the fragile peace that was brokered at the G20 by Russia and the US in southern Syria offers the tiniest spark of hope for a broader resolution, this conflict has enormous regional implications, not least in terms of the continuing stand-off with Iran and the worrying isolation of Qatar.

Amid all this though, I end where I began. The UAE is meeting the challenges to its economic health head on, from a position of strength across the emirates.

Covid-19 Economic Impact Assessments

Stay updated on how some of the world’s most promising markets are being affected by the Covid-19 pandemic, and what actions governments and private businesses are taking to mitigate challenges and ensure their long-term growth story continues.

Register now and also receive a complimentary 2-month licence to the OBG Research Terminal.

Register Here×