Talking to Saudi Arabia’s CEOs: 3 Key Takeaways

07 Jun 2017

It’s not difficult to conclude that for the Gulf region’s largest economy the past two years have been far from easy. What many analysts are now terming the new normal for oil prices – somewhere between $50-60 per barrel – has had a dramatic impact on Saudi Arabia’s fiscal position. But what impact is this having on business sentiment in the Kingdom?

Read The Report: Saudi Arabia 2016 (2017 Report coming soon)

The budget surpluses of the boom years are but a fleeting memory, and seemingly endless government spending has given way to austerity measures. But as OBG’s Business Barometer: Saudi Arabia shows, it’s far from all doom and gloom, not least because as we have seen across the GCC states, the private sector is far less reliant on government spending than is commonly thought.

Furthermore, there’s a policy silver lining to the reduction in government revenues, specifically the reinvigoration of efforts to diversify and reform the Kingdom’s economy.

In 2016 the government announced its National Transformation Programme (NTP) and the Vision 2030 initiative, as well as a flurry of reforms – from subsidy reduction, the implementation of VAT and the one that grabbed perhaps the most headlines, the IPO of a stake in Saudi Aramco. Any of these individually was significant, but together they signify major shifts in the way the Saudi economy and indeed the state operate.

So after a year of such big-ticket announcements, 2017 was always going to be a difficult year. As a number of businesspeople I spoke to on my last trip to the Kingdom said, now comes the tricky part for the policymakers: implementation, or the fleshing out of concepts so that they deliver substantive results.

Positive sentiment

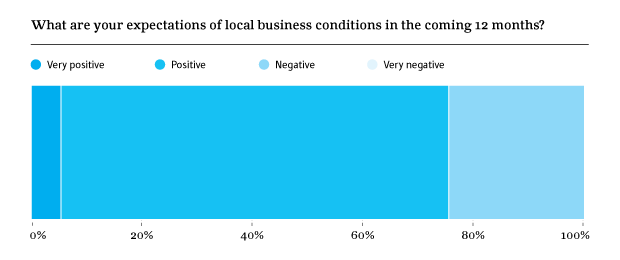

Of the CEOs who OBG surveyed, 70% said that they expected business conditions to be positive over the next 12 months, whilst 24% felt the outlook was negative. In many senses it’s this aspect of sentiment that matters most – the overarching feeling people have toward the environment. This will no doubt have been helped by higher than budgeted oil prices and therefore a better fiscal outlook, the government settling delayed payments to contractors and the positive feeling the NTP and Vision 2030 have instilled.

Areas of concern for those we spoke with include the impact of new utilities tariffs, the rise in expatriate labour fees and the uncertainty over infrastructure projects. The latter point was underlined by the fact that over 70% of construction company CEOs interviewed were in the negative camp. Similarly, smaller companies tended to be less positive in their outlook than their larger counterparts.

And, if we look at the sentiment of foreign versus local companies, overseas-headquartered businesses had a more negative perception of the business outlook. That said, in both categories well over half of respondents saw the future as favourable – 62% versus 74%.

Prospects for capital investment

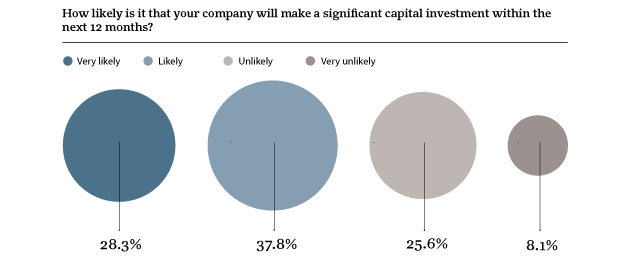

So what impact is this having on businessmen’s plans to make capital investments? Some 66% of respondents said they were likely or very likely to invest. What was particularly interesting was that of these ICT and real estate businesses were the most bullish. The least likely sector to make capital investments were companies in the industrial sector.

Perhaps given the role that ICT is slated to play in the development of the NTP and Vision 2030 it’s not such a surprise that this sector is so buoyant. Similarly, with white land tax’s introduction last year, and the hope that there will be an uptick in mortgage issuance, the real estate sector could well be in for busier times ahead. That said, those OBG have spoken to still say there’s a chicken and egg scenario when it comes to mortgages – there’s definitely demand, but the mortgage law is not fully tested, and developers are still not completely on board with building the types of housing units most needed.

Private sector flourishing

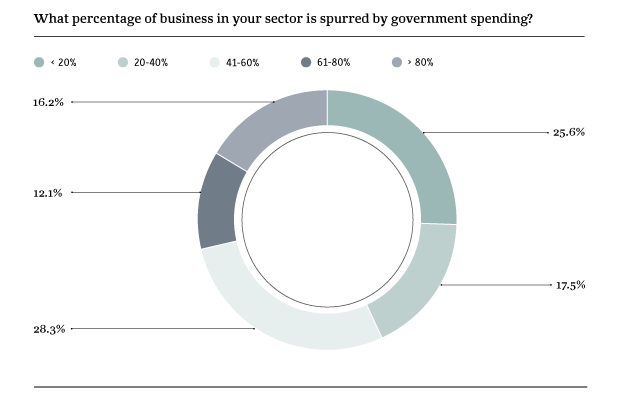

When it comes to the amount of business companies receive from government, those surveyed by OBG said they rely on government spending less than might be imagined, though it is relatively high by international standards, and reducing this is one of the key tenets of the Vision 2030 strategy. Creating an enabling environment for the private sector to flourish is receiving an ever greater amount of attention from the government, however, autonomous private sector growth will not happen overnight, so it is crucial the building blocks are put in place.

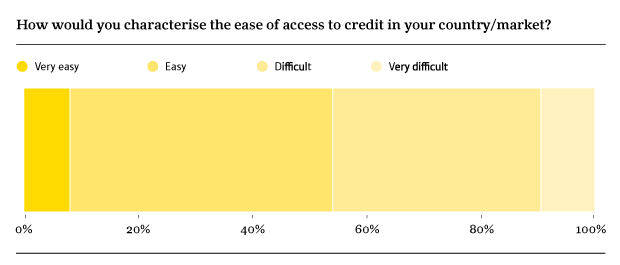

One of these is access to credit, and just over half of respondents – 54% – found this aspect of doing business easy or very easy, whilst 46% said it was difficult or very difficult. The reason that such a relatively high proportion are finding it difficult may well be a reflection of tightened liquidity within the banking sector, as well as a reluctance to lend to small and medium-sized enterprises – important elements of the Vision 2030 goals. That said, it was interesting to note that there was no particular difference in whether a company was large or small as to how they responded.

Those of us familiar with GCC economies will have frequently heard and read about skills shortages. Those surveyed identified three areas with significant shortfalls: research & development (R&D), leadership and engineering. The area that struck me as of particular note was R&D, something that we have been increasingly hearing about in relation to developing the industrial base of the economy, the all important value addition that will lead to a higher level of maturity and, crucially, jobs.

When it comes to downsides and specifically exogenous risk, survey respondents overwhelmingly felt that regional security was of most concern – 78%. This is in line with what one might imagine. What was more of a surprise is that 31% identified the slowdown of the Chinese economy as a significant risk; this speaks to the growing influence this key market has on the Saudi economy – and its increasing exposure on the global stage.

So in light of the major changes afoot in the Saudi economy and the ongoing impact of lower oil prices, the survey in most respects reflects the understandable concerns of CEOs. When it comes to the all-important outlook for GDP over the next 12 months, the respondents tended to overshoot the IMF and SAMA estimates for 2016 (1.4%), with the majority pitching for between 1.5% and 2%. Pleasingly for all concerned, only 2.7% of those surveyed felt that GDP would be below 1% – although the IMF has put its prediction for 2017 at 0.4%.

These are undoubtedly uncertain times of transition for the Saudi economy, but it is increasingly apparent that the private sector, which is expected to play a much greater role in the economy in the future, remains broadly optimistic. Yes, there are clear areas where there is cause for concern. And sentiment, though dampened in some respects, appears to be cautiously turning a corner. The $300bn worth of deals signed with US businesses during President Donald Trump’s visit to the Kingdom is a reflection of the bilateral political relationship, for sure, but it also sends an invigorating message to the business community too, who will be hoping that there will be significant opportunities presented to them as a result.

The development of a burgeoning private sector in Saudi Arabia is not going to happen overnight. However, if the huge levels of public spending that have been made and continue to be made are to bear fruit, and the goals of Vision 2030 achieved, they will require a robust private sector alongside them.

OBG Business Barometer: Saudi Arabia CEO Survey Copyright (c). All rights reserved.

This survey has been designed to assess business sentiment amongst business leaders (Chief Executives or equivalent) and their outlook for the next 12 months. Unlike many surveys, the OBG Business Barometer is conducted by OBG staff on a face-to-face basis, across the full range of industries, company sizes and functional specialties. The results are anonymous.

OBG Business Barometer is based on data from companies with revenue within the following parameters, among others:

- 96% of companies surveyed were private

- 28% of companies surveyed were international

- 51% of companies surveyed were local

The data generated allows for analysis of sentiment within an individual country, as well as regionally and globally. Additionally, comparisons can be drawn between both individual countries and regionally. The results are presented statistically within infographics and discussed in articles written by OBG Managing Editors.

OBG provides this survey, infographics and accompanying analysis from sources believed to be reliable, for information purposes only. OBG accepts no responsibility for any loss, financial or otherwise, sustained by any person or organisation using it.

For further information on the content of the survey, please contact Oliver Cornock, Editor-in-Chief, at ocornock@oxfordbusinessgroup.com.

Should you wish to reproduce any element of this survey, infographics and accompanying analysis please contact mdeblois@oxfordbusinessgroup.com. Any unauthorised reproduction will be considered an infringement of the Copyright. For further details about OBG and how to subscribe to our widely acclaimed business intelligence publication please visit www.oxfordbusinessgroup.com

Covid-19 Economic Impact Assessments

Stay updated on how some of the world’s most promising markets are being affected by the Covid-19 pandemic, and what actions governments and private businesses are taking to mitigate challenges and ensure their long-term growth story continues.

Register now and also receive a complimentary 2-month licence to the OBG Research Terminal.

Register Here×