Kenya and other African governments seek to attract private sector players

Power is one of the biggest hurdles to stronger growth in sub-Saharan Africa, with households and industrial firms struggling to ensure a reliable supply of electricity. A number of solutions are being rolled out, from off-grid networks to new transmission infrastructure, but one of the most necessary is new generation capacity.

However, the continent needs far more power than its governments can afford to build: $490bn in new projects would be required in sub-Saharan Africa to meet a projected four-fold surge in demand. As a result, there has been a push to incentivise private sector participation. This has come through a mix of models – such as privatisation in Nigeria and unbundling in Kenya – but one of the most common solutions is independent power producers (IPPs).

There is significant diversity in project structuring across Africa’s IPP landscape. Early investors received risk protection in the form of generous power purchase agreement (PPA) terms, government guarantees and escrow accounts. Such protections and assurances are more difficult to attain now, but as the market evolves these tools are becoming available from an increasing number of multilateral and bilateral actors.

Growing Market

South Africa currently has the largest number of IPPs, with 67 plants providing a total of 11.01 GW of generation capacity. Almost half of that has come in the last four years through the Renewable Energy IPP Procurement Programme, in which investors participate in bidding rounds for new IPPs, the majority of which are under 100 MW. In all other sub-Saharan African countries combined there are a total of 59 IPPs either operating or fully financed and under construction. They are spread across 17 jurisdictions and have a total capacity of 6.8 GW. The list counts projects that have been developed, financed, built, owned and operated mostly by private interests, and holding a long-term PPA with a major utility or other offtaker.

Some of the largest IPPs on the continent have been in West Africa, such as the 459-MW Azura-Edo IPP in Nigeria, and the 543-MW Ivorian Electricity Production Company IPP and the 430-MW Azito IPP, both in Côte d’Ivoire. IPPs of that size have been a rarity. Around half of the market in 2014 comprised IPPs of under 20 MW in capacity and those of 51-100 MW.

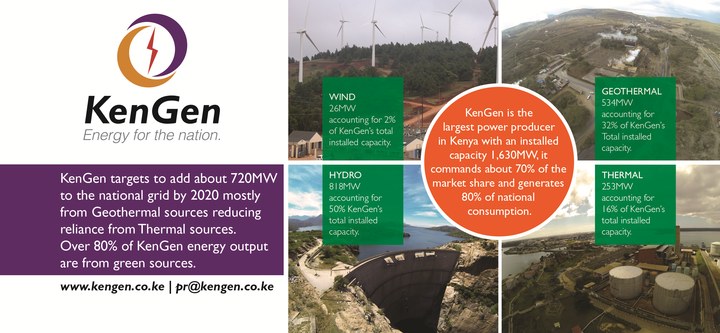

IPPs both extant and planned have not limited themselves to any one energy source, with wind, hydro, bagasse (residual material from the processing of sugar cane), coal, geothermal, methane and biomass included on the roster. However, the majority of projects are designed to run on gas or have combined-cycle technologies that can also use heavy fuel oil or diesel.

Shifting Sands

The market is still in its adolescence, however, and as new projects close they are likely bring significant shifts to the distribution of IPPs and introduce new trends and market leaders. Uganda, for example, could soon see 10 new IPPs reach financial close, and would at that point account for more than a quarter of total IPP projects. The market is also likely to broaden to other countries, with one significant newcomer being Ethiopia, where the first IPP in the country will be a 1000-MW geothermal plant. One reason why the IPP landscape is expected to change is the level of flux in many utility sectors. Several governments – from Ghana to Kenya to South Africa – are in the process of unbundling, privatising and deregulating legacy structures that were previously composed of a single state entity responsible for generation, transmission, distribution and, in some cases, regulation.

Financing

The rise of IPPs is crucial in part because of the challenges legacy power companies face in amassing capital and financing new projects. Many state-owned companies – particularly those that are also involved in distribution and transmission – have long struggled to keep up with funding demands, which is one of the factors driving the trend of unbundling activities, privatising state assets and seeking outside investment. This is in part a result of underinvestment during the continent’s downturn in the 1980s and 1990s, when utility infrastructure was poorly maintained, leading to reduced efficiency and output. The balance sheets of national power companies have also been weighed down by poor collections and outstanding payments, dramatically limiting their cash flow.

Multilateral Support

Development finance institutions such as the World Bank, the International Finance Corporation and the African Development Bank have stepped in to offer partial-risk guarantees (PRGs) and financing for IPPs. A PRG is a guarantee to cover a limited amount of an investor’s losses from multiple risks. For IPPs typically the main one is a power offtaker that does not pay for what it takes. This is often structured as a letter of credit or another instrument from a commercial bank, but routed through the World Bank with the government as the ultimate provider of the guarantee. If an investor were to call on a PRG it would collect from the World Bank, which would then have recourse to call on its entire financial relationship with the country to recover the funds. However, no PRG has ever been called on, as the World Bank has always been able to negotiate settlements. These instruments are seen as a good fit with the power sector.

While PRGs provide a measure of cover, there are also other multilateral initiatives in play to strengthen financing access elsewhere in the project life cycle. The African Development Bank, for example, has established a $100m fund for renewables projects called the Facility for Energy Inclusion. It will provide senior and mezzanine debt to IPPs whose projects cost $30m or less. It also plans to seek funding from others to boost available capital to $500m, it said in December 2016.

Bilateral Aid

Several bilateral initiatives are also under way to support IPPs in Africa. China offers concessional loans from state-owned enterprises, such as the China Development Bank or the Export-Import Bank of China. Financing also comes from commercial or quasi-state entities, such as Industrial and Commercial Bank of China and China Construction Bank.

The US government’s Power Africa programme has also played a role in supporting inbound investment by strengthening government support for US investors in regional power projects, including IPPs. The initiative offers investors a range of risk mitigation tools and financing to overcome last-mile obstacles. Nigeria’s Azura has a PRG as well as multiple Power Africa benefits, for example, while the US’ Millennium Challenge Corporation is providing up to $498.2m in support to the Electricity Company of Ghana, the state power distributor. This money will be used to help clear up old arrears, train employees and modernise operations. The Power Africa programme follows a model of multilateral and bilateral investment catalysing private investment in Africa’s power sector. Since 1994 the rise of private investment in IPPs has tracked the involvement of governments and international organisations. Typically a small rise in investment from the latter has been accompanied by a larger boost from the former.

You have reached the limit of premium articles you can view for free.

Choose from the options below to purchase print or digital editions of our Reports. You can also purchase a website subscription giving you unlimited access to all of our Reports online for 12 months.

If you have already purchased this Report or have a website subscription, please login to continue.