From Brexit to Brent: Are Gulf Business Leaders Really That Worried?

23 Oct 2016

View the OBG Business Barometer: GCC CEO survey infographic

The OBG Business Barometer: GCC CEO Survey, in association with Saudi Hollandi Bank

2016 is likely to go down as one of those years where people will ask where you were and what you were doing when you heard about Brexit or one of the sadly all-too-familiar atrocities. Whilst I know the old adage that negative stories sell newspapers, even by the media’s usual standards, this year has had more than its fair share of gloom.

Ever sensitive to global influences, sentiment in the GCC has been hit not only by recent events, but also by a period of lower oil prices and heightened regional tensions. The knock-on effect has resulted in growing budget deficits, weak performance in equity markets and overall uncertainty as government and corporates alike tackle a new economic reality.

In the face of this it is all too easy to read one gloomy headline after another and conclude that the private sector is at best battening down the hatches and at worst retreating, and at just the time it’s expected to step to the fore. Indeed, this is a key component of all the various Gulf states’ diversification strategies.

Furthermore, good-news stories – such as the award of a multi-year contract by Boeing to Abu Dhabi’s Strata Manufacturing and the Saudi Public Investment Fund’s investment of $3.5bn into mobile taxi app Uber and Abu Dhabi’s Strata – have received very little media attention.

Numerous leaders, writers and experts have predicted that the region is in for a rough ride – lower revenues, reduced government spending, weaker GDP, heightened uncertainty…. And, yes, times are harder than they have been.

During the run-up to Brexit in the UK, Michael Gove, a pro-Leave member of House of Commons, said quite rightly that people “have had enough of experts”. He was, of course, speaking of the broader problem in Western politics, where cynicism is at an all-time high, as witnessed from the US presidential election debates to the inability of Spain to elect a majority government.

A more positive outlook

As I looked at the results of Oxford Business Group’s first Business Barometer, a survey conducted over the past six months across the GCC on an anonymous basis, with just over 200 senior business executives, Goves’ statement struck me as relevant.

Why? Well, as you will see, despite the prevailing opinion in the global media that the region is in the economic doldrums, the evidence in the results of the survey points to a rather more upbeat outlook.

Of course there are significant challenges – from tapping global debt markets to implementing major reform programmes (for example, Saudi Arabia’s new National Transformation Programme) – but the nearly 200 business leaders we spoke to, who come from all sectors and industries, clearly feel that it is also a period of opportunity.

What we found

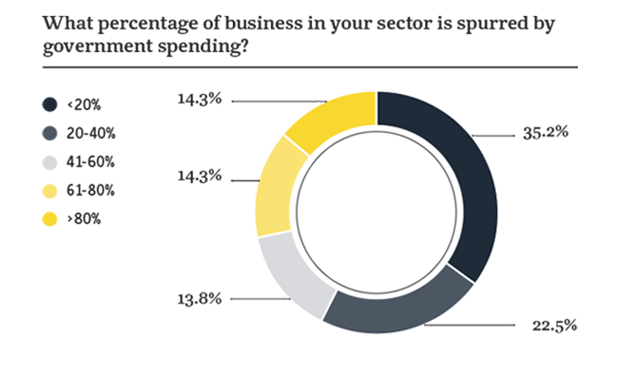

Perhaps the most interesting challenge to conventional opinion was that private sector businesses rely on government spending far less than many commentators imagine. The traditional narrative has been that public sector spending is a much bigger driver of the private sector than it should be, or would be in a so-called developed economy.

Yes, the private sector is less of a contributor to GDP than it might be, but it is posting stronger growth, and indeed, the non-oil sector is seeing something of a reverse in statistical fortunes. In the period of high oil price growth, it was difficult to show in percentage terms the growth of the non-oil sector simply because of the huge revenues oil was generating. Even when the non-oil segment was in fact growing, its contribution to many metrics were technically falling, masking the strides being achieved.

Continuing to invest in a competitive environment

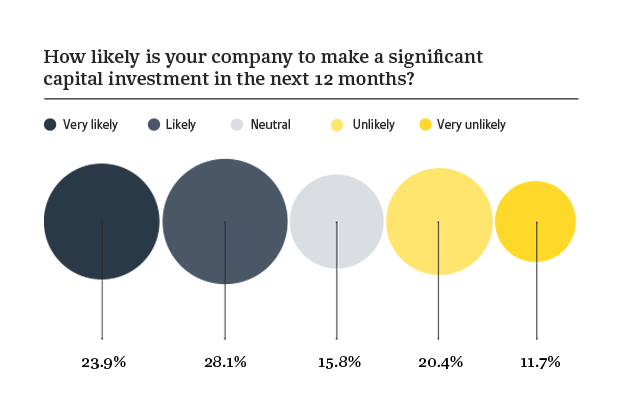

Another striking finding is that over half of the CEOs we spoke to are likely or very likely to make a significant capital investment over the next 12 months. Again, there is a whole panoply or reasons why a business might look to invest in the current environment, but this is certainly a positive sign.

Under these circumstances it is probably less of a surprise that competition is strong – these are markets that have seen rapid development and high GDP rates until very recently and therefore a period of slower development is set to favour those companies best placed to fight their corner.

That said, increased competition tends to favour consumers and end-users, even if it can be a drain on source companies’ bottom-lines.

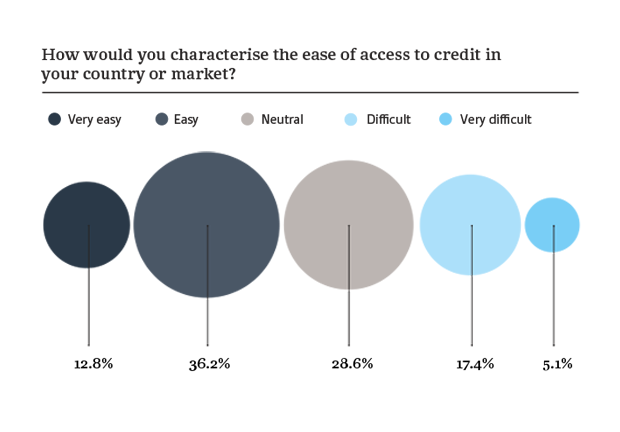

Access to credit and transparency

Access to credit is a perennial issue for corporates the world over, particularly since the banking crisis of 2008-09. This is equally true in the GCC. However, as you will see just under half of all respondents said access to credit was easy or very easy. Now, it is of course likely that the more established businesses will find it more straightforward to get credit lines than a start-up, but the overall picture is once again far from bleak.

One of the most frequently cited issues that investors I speak to at events around the world identify as an impediment to doing business in the GCC is that of transparency. From the robustness of contracts to terms of payment, transparency is vital to businesses. Here we can see that 54% of respondents feel the level of transparency for conducting business is very high or high.

![]()

Positive business sentiment overall

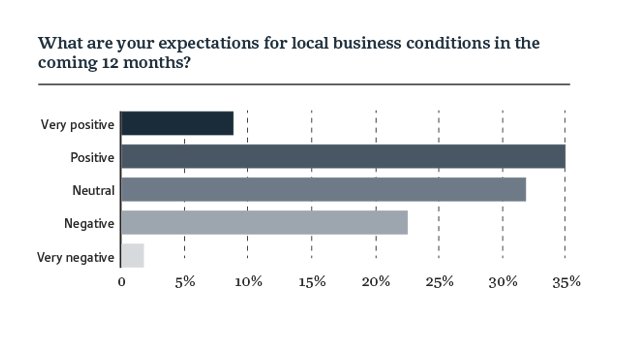

Finally – and perhaps most telling – is the expectations of those surveyed for business conditions over the next 12 months. Whilst the largest group of those surveyed felt positive, a significant proportion was neutral or negative. I don’t see this as particularly concerning as unless you are a die-hard optimist it would be very difficult not to accept that companies in the GCC face challenging headwinds.

However, taken within the context of the rest of the survey results, the picture remains broadly upbeat.

It is only just the end of the Q3 reporting season and the results for corporates are mixed but far from disastrous in a lot of sectors. And, whilst many would hope that the remainder of the year will see markets settle and geopolitical tensions ease, this is perhaps wishful thinking – oil prices seem to be settling at around the $50 per barrel rut, Chinese growth figures continue to act as a drag, the fallout of Brexit remains unclear and of course the US presidential election is imminent. And that’s just a couple of the factors at play.

Whilst it’s difficult to extrapolate firm conclusions from this first OBG Business Barometer, what can be deduced from the results, particularly regarding respondents’ capital expenditure plans, is that the region’s corporates remain engaged and are positioning themselves to be able to compete when stronger growth returns.

We will be continuing to survey the many business leaders we meet over the next six months and it will be fascinating to see how ongoing internal and external factors impact sentiment. Many of them, like me I suspect, will be hoping for rather fewer dramatic headlines and greater market stability.

OBG Business Barometer: GCC CEO Survey Copyright (c). All rights reserved.

This survey has been designed to assess business sentiment amongst business leaders (Chief Executives or equivalent) and their outlook for the next 12 months. Unlike many surveys, the OBG Business Barometer: GCC CEO Survey is conducted by OBG staff on a face-to-face basis, across the full range of industries, company sizes and functional specialties. The results are anonymous.

The data generated allows for analysis of sentiment within an individual country, as well as regionally and globally. Additionally, comparisons can be drawn between both individual countries and regionally. The results are presented statistically within infographics and discussed in articles written by OBG Managing Editors.

OBG provides this survey, infographics and accompanying analysis from sources believed to be reliable, for information purposes only. OBG accepts no responsibility for any loss, financial or otherwise, sustained by any person or organisation using it.

For further information on the content of the survey, please contact: ocornock@oxfordbusinessgroup.com

Should you wish to reproduce any element of this survey, infographics and accompanying analysis please contact mdeblois@oxfordbusinessgroup.com. Any unauthorised reproduction will be considered an infringement of the Copyright.

Covid-19 Economic Impact Assessments

Stay updated on how some of the world’s most promising markets are being affected by the Covid-19 pandemic, and what actions governments and private businesses are taking to mitigate challenges and ensure their long-term growth story continues.

Register now and also receive a complimentary 2-month licence to the OBG Research Terminal.

Register Here×