Myanmar's holds a diverse mix of mineral resources

While most industries have benefitted from an influx of foreign investment since the opening of the economy in 2011, the mining sector has yet to catch up. There are a few reasons for this, including legal inconsistencies and ongoing civil unrest in key areas. Through the implementation of mining law reforms passed in late 2015, many prospective investors’ concerns have been addressed by the legal amendments, and they are eagerly waiting in the wings to tap the country’s deposits of metals, ores, industrial minerals and coal.

With a total land area of 676,578 sq km, Myanmar is the world’s 40th-largest country and the second-largest in South-east Asia. Despite containing vast deposits of tin, tungsten, copper, gold, silver, zinc, lead and precious stones, the country’s diverse landscape remains relatively unexplored compared with other mineral-rich countries. Yet the newly elected government promises much-needed reform and foreign capital for a sector that is as opaque as it is profitable.

Geology

Wedged between the Himalayas in the north and the Andaman Sea to the south, Myanmar has a unique geology. Located in a suture zone on the Burma Plate, it resembles a sort of ancient tectonic jigsaw puzzle. With the Indian Plate to the west, Indochina Plate to the east and the Eurasian Plate to the north, the country is divided into four geographic belts: the Eastern Highlands, Central Lowlands, Western Ranges and Arakan Coastal Plain. Sloping downward from north to south, each belt has its own history as to the formation of the earth’s crust. Major known mineral belts also run from north to south. Key mining areas include the tin-tungsten belt of the Tanintharyi Region, running along the eastern border with Thailand; the antimony belt in the states of Shan, Kayah and Mon; the lead-zinc-silver-barite belt of Shan State; the porphyry copper belt in Monwya and Wuntho; the nickel-chromite belt of the northern Chin Hills and Tagaung Taung; the gold-copper belt in the Sagaing Region; the oil-gas belt of central Myanmar and Ayeyarwady Delta; and the precious stone belts in the Kachin and Mogok Regions.

Under-Explored

While the entire country was mapped under the British colonial era, and later through various agencies and foreign missions, there is still limited data in the form of modern geological surveys. According to the Department of Geological Survey and Mineral Exploration (DGSE), there are more than 2000 occurrences of 62 different commodities. These include precious stones, which remain off limits to foreign investors, and other minerals such as tin, copper, gold and zinc. The local authorities are actively marketing the available opportunities, as Myanmar largely lacks the capital and equipment to extract the country’s mineral wealth on a large scale.

From the establishment of the 1988 Foreign Investment Law through to October 2015, only $2.87bn of investment had been approved in the mining sector, or 4.95% of all foreign direct investment (FDI), around $58.03bn. According to the Myanmar Investment Commission, the mining sector received $6.26m in FDI for fiscal year 2014/15, the fifth-largest recipient by sector, though considerably less than the $3.22bn received for hydrocarbons (see Economy chapter).

Gold & Copper

Of the 13 existing foreign mining operations, gold and copper dominate, with a geographical concentration in the Sagaing and Mandalay Regions. Although a total of 32 foreign projects have been permitted along this belt, prior sanctions meant that only eight remain; with a total combined capital investment of $1.53bn, of which copper represents more than 90%. Notable foreign gold prospectors include PanAust from Australia and Nobel Gold from Hong Kong, which is currently exploring for gold and associated minerals in the Sagaing Region.

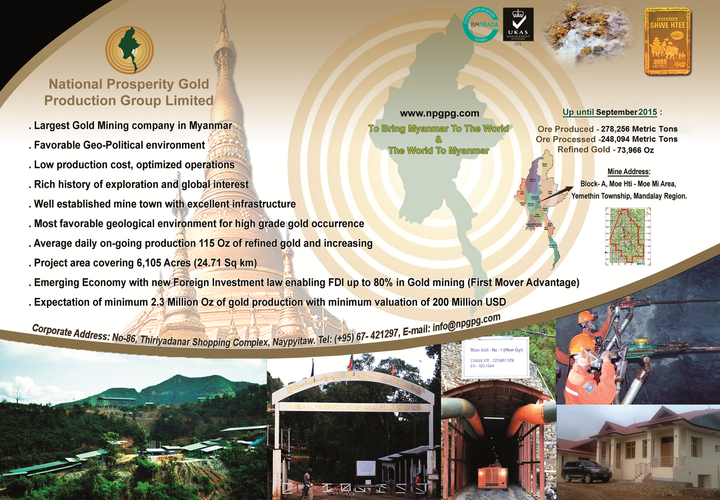

The largest local player in gold production is the National Prosperity Gold Production Group, which operates the Modi Momi mine. A 2011 survey of the concession estimates it holds more than 2.3m oz of gold, and refined gold production reached 52,600 oz from September 2011 to March 2015. According to company representatives in late 2015, the firm was in the final stages of commissioning a new plant that will increase production from 80 oz to 400 oz per day.

Until the modified laws usher in a new wave of foreign exploration, Chinese-led projects are likely to dominate operations in the sector for the foreseeable future, particularly the Monywa copper project, which comprises the Sabetaung and Kyisintaung and Letpadaung copper mines (which were initially operated by Canadian firm Ivanhoe from 1994 to 2007). The latter exited due to the previous sanctions, selling their stake for a reported $103m to the Myanmar Wanbao Mining company under the Ministry of Mines (MoM).

After a lengthy brokerage process the mine was taken over in 2011 under a joint venture (JV) between the Union of Myanmar Economic Holdings (UMEHL), the economic arm of the military, and Wanbao Mining, which falls under the umbrella of Norinco, a Chinese state-owned military-industrial conglomerate, which provided $250m for a stake in the venture. As of July 2013 a revised contract gave Wanbao 30% of the mine’s profits, down from the initial 49%, while the government received 51% with the remaining 19% paid to the UMEHL. Although the project has come under much scrutiny, National League for Democracy chairperson Daw Aung San Suu Kyi voted in favour of the project in 2013. Since then approximately $1bn has been committed to expanding the site, with an annual production target of 139,000 tonnes of copper. Despite the potential, ongoing land disputes continue to delay the project.

Nickel

In terms of total invested foreign capital, nickel is the third-largest recipient, with one project under China Nonferrous Metal Mining (CNMC), followed by lead, silver and zinc, which have four existing foreign investors and a total of $20m. The Tagaung Taung Nickel Mine, located in Mandalay Region, is the largest nickel-laterite ore exploration project by a Chinese enterprise overseas, with an investment of some $800m for an estimated 700,000 tonnes of nickel. Commenced in 2011 under CNMC through a production-sharing contract (PSC) with No. 3 Mining Enterprise ( ME-3). The production process consists of strip mining and coarse-size separation processes, after which qualified ore is transferred to the smelting plant to produce ferronickel. According to the Metallurgical Corporation of China, the site will produce an annual output of 25,000 tonnes of nickel ferrite and nickel metal. According to the International Trade Centre, the mine produced some $11.5m worth of ferronickel in 2013.

Marble

Statistics from the Directorate of Investment and Company Administration Myanmar show that Vietnamese group Simco Song Da is the third-largest foreign investor in mining. The group is focused on large-scale marble extraction and manufacturing in Nayputaung quarry in Rakhine State, some 500 km from Yangon. According to Myanmar Ceramic Industries, Simco Song Da had invested $18m in the country as of 2012.

The reserve is estimated to hold 87m tonnes of marble, with an ore reserve measuring 914-metres long, 457-metres wide and 244-metres high. To date, commercial production of marble slabs has been above 100,000 sq metres annually, producing Nayputaung marble in three major colours: dark grey, light grey and chocolate brown. The Vietnamese company signed a PSC with ME-3 based on an agreement of 80:20 to 70:30 correlating to the quality and price of marble extracted.

Down But Not Out

Once coined the “Timber Mine” for its hardwood inner structure, the concession to the Namtu Bawdwin mine in northern Shan State is operated by Win Myint Mo Company Limited. In its prime, the mine descended around 366 metres over 12 levels, and became the largest producer of lead, silver and zinc in the world. The compound dates back more than 400 years and is described in an article by JD Hoffman in 1916 as one of the world’s leading deposits. In August 1915 the deposit was estimated at some 2m tonnes, containing about 25 oz of silver per tonne as well as 27% lead and 22% zinc, an impressive concentration even by today’s standards.

During the Second World War, the mine changed hands to the Japanese, producing 200,000 tonnes of high-grade ore between 1942 and 1945. Once Myanmar gained independence in 1962 very little of the mine’s rich resources were tapped, with production dwindling for decades. According to local sources, a feasibility study by a German company in 1975 found the location to be highly profitable, but no advancements were made as the company and government at the time could not agree on processing technology. While it has been thought in recent years that a foreign investor would jump-start the mine, nothing had materialised by November 2015. However, investors are keen on the area, in particular Hong Kong-based Asia Pacific Mining, which has been granted an exploration licence nearby the old mine.

Tin

Another mineral attracting significant attention is tin, which is bolstering Chinese supply to such an extent that China has gone from a net importer of refined tin to a net exporter within six years. This is mostly due to the sharp rise in tin-concentrate imports from Myanmar ( production rose 4900% between 2009-14), allowing Chinese refineries to increase tin production by 10% to 175,000 tonnes as of the end of 2014.

The rise in exports of tin concentrate from the Tanintharyi Region into China, from almost zero a few years ago to more than 20,000 tonnes per year, played a key role in the drop in tin prices on the London Metal Exchange, which hit a five-and-a-half-year low in April 2015. The exchange’s prices had fallen by as much as 9% in one day to $14,850 per tonne, representing a 22% decline on the start of 2015. As of late 2015, experts were predicting a further drop to $12,000 per tonne before any recovery takes place. The price drop is even more notable as it coincides with efforts by Indonesia, the world’s largest exporter of tin, to limit its outbound sales and thus support global prices. In the same month as the six-year low, April 2015, imports from Myanmar into China hit a record high of 33,095 tonnes in April 2015, according to the International Tin Research Institute’s China office.

The DGSE notes 480 deposits of tin-tungsten with a total potential of 40m tonnes. This includes the Mawchi mine, which is owned by major player UMEHL and operated by the Ye Htut Kyaw Mining Company. Tin exploration is currently dominated by local mining companies and affiliates of UMEHL. There have been seven foreign exploration projects for the mineral since the early 1990s. The two remaining projects, in Dawei in the southeast of the country, fall under De Rui Feng Investment of China and Myanmar Pongpipat Company of Thailand, which together had brought in investment of $16.33m as of November 2015.

Other Projects

Notable players from outside Asia include Cornerstone Resources from Australia, which is prospecting for zinc in Shan State’s Mong Pan Township, and Canada’s Centurion Minerals, which is partnered with local firm Crown Minerals in an 80:20 joint venture. The latter, which has a history of mining activity in Indonesia, is evaluating two gold-exploration concessions by the MoM in late-2013. The first includes the 692-sq-km “slate belt” south of Mandalay. The area encompasses Modi Taung gold mine in the south and Lebyin gold and polymetallic mine in the east, both discovered by Ivanhoe Mines prior to their exit in the mid-2000s. The second concession, which covers 900 sq km and is located 40 km north of Mandalay, is bordered by two operating gold mines. Although phase I of the exploration yielded positive data, no announcement for phase II had been announced at the time of publication.

Off Limits

Not to be outdone by lucrative metals, precious stones are Myanmar’s most valuable mineral by some stretch. Besides the prized rubies of Mogok Valley, the northern hills of Kachin State are home to the world’s highest quality jadeite, known as “imperial jade”. Despite the undeniable growth potential of the country’s gem industry, particularly in downstream processing, questions remain around accessibility, with many areas off limits due to armed conflict between the military and a number of rebel groups. According to local industry leaders, the lack of a systematic value-chain hurts a sector that only receives an estimated 10% of the final sale price. The remainder is pocketed by countries such as Thailand, which cuts and polishes the stones. “There is no export licence for finished products,” Daw Thet Thet Khine, managing director of Golden Palace Gold and Jewellery, told OBG. “Myanmar is rich in natural resources, but policy does not enable us to leverage off this. Thus, neighbouring countries reap the rewards by carrying out value-added services for raw materials from Myanmar,” she added.

Quest For Transparency

Reliable data on Myanmar’s gem market has long been difficult to come by, and significant challenges remain around transparency and accountability in the industry’s role in armed conflict. A report issued by Global Witness in October 2015 shed light on the jade industry, in particular shadowy relations between factions of the army, the Kachin Independence Army, so-called drug lords and various business elites. The report estimated that the industry was worth $31bn in 2014 alone, which if true would account for around half of national GDP. The vast majority of funds, it said, were leaked via illegal routes with China, where buyers have been known to spend up to $5m for a necklace adorned with the stone. The report’s figure dwarfs a previous estimate by the Harvard Ash Centre for Democratic Governance, which put unofficial sales at approximately $8bn in 2011. According to Global Witness, associated parties earned a total of $122.8bn from 2005 to 2015.

Some of those parties have since come forward claiming that their profits are via official routes through emporiums organised by the government. According to official statistics, Myanma Gems and Jade Emporium generated a record $3.4bn in October 2014. However, sales were down by more than 33% at the 2015 event. To explain this, analysts point to more stringent regulations, including a 5% deposit up-front, which was imposed after a number of past bidders failed to deliver. The new policy reduced the number of buyers, particularly Chinese ones, by 60% at the 2015 auction.

The first report of the Myanmar Extractive Industries Transparency Initiative (MEITI), due in early 2016, will contain information about the amount of tax paid on natural resources. Success of the MEITI application will greatly depend on how the report accounts for the jade industry.

Legal Framework

The industry is currently regulated by the Myanmar Mines Law of 1994 and Myanmar Mines Rules of 1996. In late December 2015, however, Parliament adopted a number of long-discussed amendments to the country’s mining laws. The changes outlined in the legislation will be implemented in the coming months, starting with draft regulations from the MoM to be finished within 90 days (see analysis).

In line with the current regulations, a foreign company wishing to invest in mining in Myanmar needs to arrange a field visit with the MoM should it wish to explore investment opportunities. If, after the field visit, the investor expresses an interest to proceed, they must submit a letter of proposal, which needs to include, among other things, the intended prospecting area, amount of capital or estimated cost of the project, technology that will be used, and the mineral of interest. This process is similar for prospecting, exploration, feasibility studies and production permits.

Once those requirements have been met the foreign company must agree, by way of contract with the DGSE, that they will explore the given area for the stated minerals of interest and pay $250 (on average) per sq km for land rent, a signature bonus between $50,000 and $100,000, and a bank guarantee ranging from $100,000 to $200,000, which is held for the duration of the venture. The company then needs to negotiate a minimum expenditure amount based on the size of the project. Royalties are also agreed in advance, spanning a range of rates for various minerals. Once signed by both parties, the investor needs to acquire regional approval from the local authority, which can be time-consuming. The whole process from start to finish can take a few months, and even as long as two years.

In an effort to expedite the process, the MoM has removed the requirement to obtain an operating licence from the Myanmar Investment Commission prior to the company’s permit application. If exploration is successful, companies need to sign a PSC with ME-1, No. 2 Mining Enterprise ( ME-2) or ME-3. At present, ME-1 is responsible for the production and marketing of antimony, lead, zinc, silver, iron, titanium and copper ores, while ME-2 is responsible for the mining, production and marketing of gold, platinum, tin, tungsten and other heavy minerals. ME-3 oversees the production and supply of industrial raw minerals.

Hurdles

The older mining regulations are widely seen as outdated and costly, in particular the PSCs. The result has been limited foreign investment and sufficient pressure for the ministry and central government to amend the existing legislation. PSCs, which are often viewed as a significant deterrent, could range from 10-30%, based on the quantity and quality of the mineral produced. Aside from land rents and signature bonuses, project earnings are also impacted by various forms of taxation, calculated on income, imports and royalties (see Tax chapter). On top of these, an unstable supply of electricity, lengthy licensing process and ethnic conflict weigh heavily on project execution.

Though the reforms represent a big step forward, external factors will also need to improve before the sector benefits fully from the legislative changes. “There is a downturn in mining activity around the world, so even with passage of the Myanmar Mining Law by Parliament there will be less interest in the sector than originally anticipated,” U Than Tun Win, managing director of local group TA Resources, told OBG. “However, this will improve as commodity prices balance out.”

Another challenge is dealing with multiple levels of government. Following a lengthy exploration and licensing process, the mining company also needs approval from the provisional government. “In order to mitigate risk it is important to engage with the local or state government from the get-go,” Michael Phin, head of finance for Valentis Resources, told OBG. “Working with the local land and forestry departments in the particular region is important because each state is dynamic and operates in a unique way,” he added.

Sticking Points

Small-scale mining presents its own challenges. As of November 2015, the MoM had licensed just under 2500 mining operations, most of them small, locally owned projects using outdated methods. Many reportedly practice techniques harmful to the environment and in contravention to basic human rights. Indeed, the role of small-scale mining was among the key issues that held up the amendment process, which had been under way since 2013. Proposed amendments led to much debate between the Lower House and Upper House, with the latter arguing they would benefit small-scale miners by allowing them to enter into JVs with foreign investors, while the Lower House opposed this, leading to a postponement of the bill. In the end, with some adjustments, the outgoing parliament headed by the Union Solidarity and Development Party adopted the law just days before January 1, 2016.

Several sticking points remain, however. According to Andrew Mooney, CEO of Asia Pacific Mining, investors need to be patient. “People have to understand that the country is going through a massive change. There are many hoops that you need to negotiate,” he said. “Mining companies need support from the central and regional governments, as well as from the local community. If you fail to reach an understanding with any one of those, then it will be difficult to succeed.” Industry experts believe that certain measures would act as a catalyst for prospectors. “There are three pieces to the puzzle that need to be solved: political transparency, conflict resolution and legal reform,” Lachlan Foy, head of commercial affairs at local mining consultancy Valentis Resources, told OBG. “With the recent political transformation, the new nationwide ceasefire agreement and recently enacted legislation, the industry is likely to experience a step-change,” he added.

Outlook

Depressed commodity prices ensure that China will remain a dominant force in Myanmar’s mining industry, at least in the short term. Nonetheless, firms from around the globe will continue to position themselves to capitalise on the easing of legislative barriers, with a close eye on implementation of the new amendments. In many respects, increased foreign involvement remains more a question of when than if, as the speed of the sector’s development will greatly depend on the participation of foreign players with the technology, equipment and capital to fund milestone projects. Existing exploration schemes may take a few years to lead to production, and the number of multinationals entering should rise as the reforms take root. New concepts of profit-sharing will put investors at greater ease, yet a period of testing the waters will still need to be overcome as Myanmar enters into yet another phase of reform.

You have reached the limit of premium articles you can view for free.

Choose from the options below to purchase print or digital editions of our Reports. You can also purchase a website subscription giving you unlimited access to all of our Reports online for 12 months.

If you have already purchased this Report or have a website subscription, please login to continue.