– Economies in the region were hit by reduced trade volumes and lower oil prices

– Governments launched extensive stimulus packages to stabilise their economies

– Short-term recovery will be tied to oil prices and the resumption of travel

– The pandemic looks set to accelerate economic diversification efforts

Facing the twin challenges of a sharp reduction in trade and a steep drop in the price of oil as a result of Covid-19, countries in the Middle East have weathered a particularly difficult 2020.

While circumstances have been challenging, the region has looked to digital innovation as a path to recovery, and a number of governments have accelerated their existing plans for economic diversification.

Using OBG Advisory’s “4R” matrix for analysing national Covid-19 responses – encompassing Resilience, Response, Recovery and Reinvention – we highlight success stories and lessons from the region over the year, and look ahead to 2021.

As a region in which a number of countries derive significant proportions of their GDP from hydrocarbons, the Middle East was particularly vulnerable to the immediate effects of the pandemic.

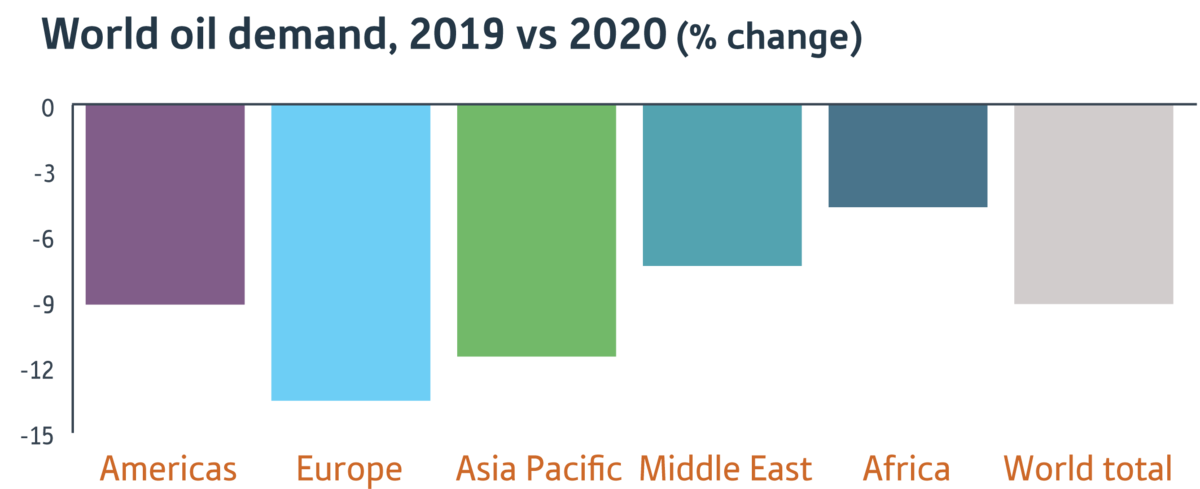

Global efforts to contain the virus – which included severely restricting, and in some cases prohibiting, transport and cross-border travel – ultimately led to a sharp reduction in demand for oil.

This fall in demand, exacerbated by a price war between Russia and Saudi Arabia in the first half of the year, resulted in the price of oil falling from year-opening values of $66 per barrel to less than $20 in late April.

While prices have since recovered to around $50, partly on the back of a historic production cut agreement from oil-producing nations, the fall has nevertheless had a significant impact on major oil-producing nations in the region.

For example, both Saudi Arabia and Oman derive around 75% of export revenue from oil and gas, while the sector contributes an estimated 45% to Kuwait’s GDP.

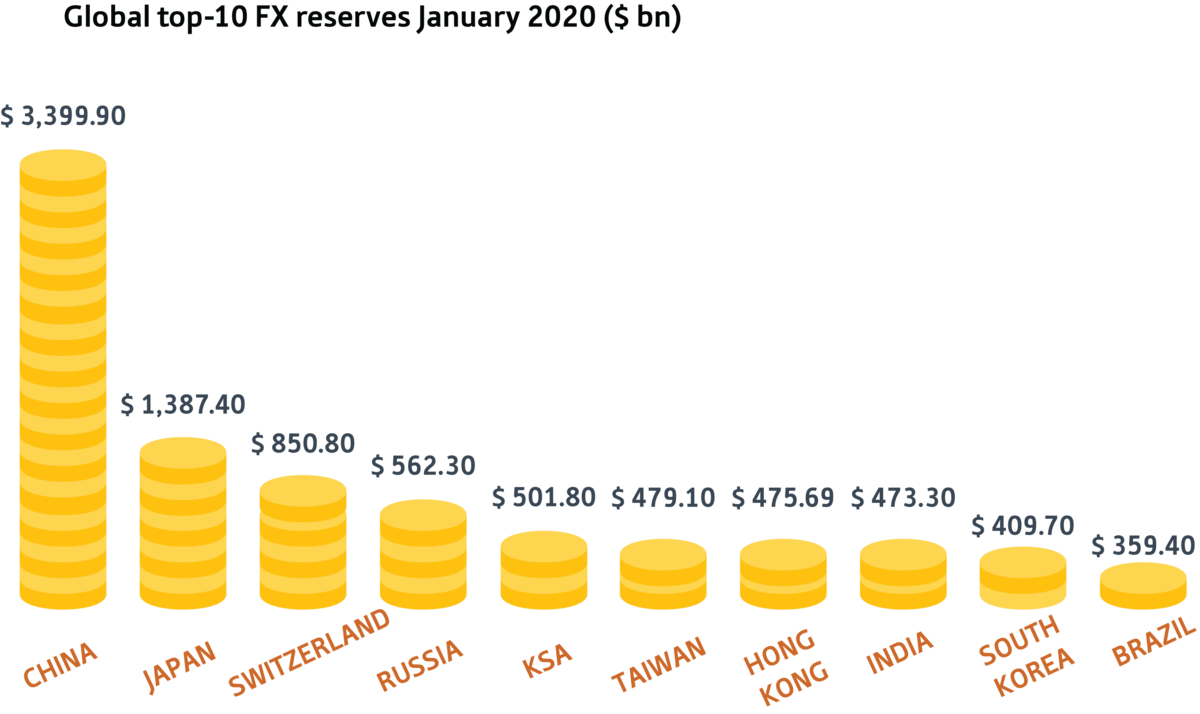

Although this focus on energy made these countries particularly vulnerable to a fall in revenue, their strong foreign currency (forex) reserves – largely the fruit of strong hydrocarbons earnings in the past – helped bolster their resilience.

For example, in January 2020, just prior to the pandemic, Saudi Arabia had the fifth-highest forex reserves in the world, at $501.8bn, and relatively low public debt, at 22.8% of GDP.

The UAE was similarly well insulated, entering the crisis with record forex, at $110bn, and low debt – equivalent to around 20% of GDP.

Infrastructure resilience

Aside from economic pressures, countries in the region had varying levels of resilience when it came to handling the health challenges posed by the pandemic.

Recent investment in the health care systems helped many countries cope with increased pressure as infections spread.

Saudi Arabia recorded a compound annual growth rate of 21% in its health care budget between 2010 and 2019, with the number of hospitals and hospital beds increasing by 9.1% and 10.7%, respectively, during 2014-18.

In contrast, lower-income and conflict-affected nations in the region, such as Yemen, Syria and Iraq, had less developed health infrastructure, leaving them more vulnerable.

Meanwhile, in Lebanon the August 4 explosion in the Port of Beirut destroyed half of the city’s medical centres and left three of its hospitals “non-functional”, according to the World Health Organisation, placing significant strain on the health care system.

Despite these challenges, most countries in the Middle East benefitted from their favourable demographic profiles. With a large proportion of their populations below 30 years of age, they benefitted from a relatively small number of people in high-risk groups.

Elsewhere, another factor that helped build resilience was the state of ICT networks.

Once again, technologically advanced nations such as Saudi Arabia, the UAE and Qatar had stronger digital infrastructure, which allowed them to adapt more easily to the shift towards digital payments, online health initiatives and remote-working practices.

To limit the spread of the virus, governments in the Gulf implemented a series of restrictions on businesses and movement throughout March and April.

While these strategies varied from country to country, they usually included the closure of businesses deemed non-essential, along with curfews and lockdowns.

Some countries acted before widespread infections, with Saudi Arabia banning pilgrimages to Makkah and Medina, as well as preventing access to specific religious sites in the cities, from as early as February.

Others implemented strict penalties for non-compliance with social -distancing guidelines, with those found to have broken the rules subject to heavy fines and even prison sentences in Jordan, Saudi Arabia and the UAE.

Accompanying the restrictions were significant testing and containment measures. The UAE was a world leader for testing in the early stages of the pandemic, pioneering a drive-through testing centre as early as April. Meanwhile, Bahrain received international recognition for its so-called war room initiative, which consisted of a stringent screening and testing centre for citizens returning to the country.

Such measures had varying degrees of success throughout the region. For example, Iran has been badly affected by the virus, with 1.1m cases and 53,000 deaths as of mid-December.

While there has been a substantial number of infections in other Middle Eastern countries, such as Saudi Arabia (360,000), the UAE (187,000), Kuwait (147,000) and Qatar (141,000), they have, on the whole, experienced a low number of deaths, especially when compared to other continents. As of December 16, virus-related fatalities stood at 6070 in Saudi Arabia, 913 in Kuwait, 622 in the UAE and 241 in Qatar.

Institutional response

In addition to the medical response, governments in the region passed significant financial stimulus packages to help offset the economic fallout of the pandemic.

This was the case in Bahrain, where the government launched a BH4.3bn ($11.4bn) stimulus, equivalent to around 30% of GDP, in mid-March.

In addition to increasing liquidity support funds and loan facilities from the central bank, the package paid the salaries of all private sector employees, along with the electricity and water bills of citizens and businesses, for three months. Certain bills and tax payments were also deferred.

Elsewhere, in mid-April the Saudi government launched a multifaceted SR132bn ($35.2bn) stimulus package, consisting of SR70bn ($18.7bn) in support for the private sector, SR50bn ($13.3bn) in stimulus for the banking sector and small and medium-sized enterprises, and SR12bn ($3.2bn) in social assistance, including support for low-income families and micro- entrepreneurs, among others.

Cooperation on food security

With the pandemic leading to the closure of many borders and the disruption of supply chains, there were region-wide collaborative efforts to shore up supplies of essential items such as food, water and medicines. As a region that is a net importer of food and water, this was of particular importance.

To this end, in mid-April the GCC adopted a Kuwaiti proposal to create a joint food supply network across the bloc. Concerned by disruptions to trade, the countries set up special arrangements at border control and Customs posts that facilitated the movement of food and medical supplies.

Meanwhile, in an attempt to further strengthen its food security, Kuwait struck a deal to streamline the import of Egyptian products, which were previously subject to extensive testing, while it also approved imports of beef from Brazil.

Private sector response

Companies in the private sector were also forced to adapt to the new normal. In response to the sharp increase in demand for online services, many retail companies worked to upgrade their digital offerings, particularly in the areas of ordering, delivery and payment.

One particular example is Dubai, whose shopping malls act as a top tourist attraction.

Following the implementation of health restrictions, which led to the closure of all non-essential businesses, The Dubai Mall, the largest retail space in the UAE, launched its own virtual store on Gulf e-commerce platform noon.com.

This came as Mall of the Emirates, Dubai’s second-largest mall, launched its own online shopping platform, called Trends at Your Doorstep, while hypermarket chain Carrefour UAE upgraded its portal to a full-scale online marketplace.

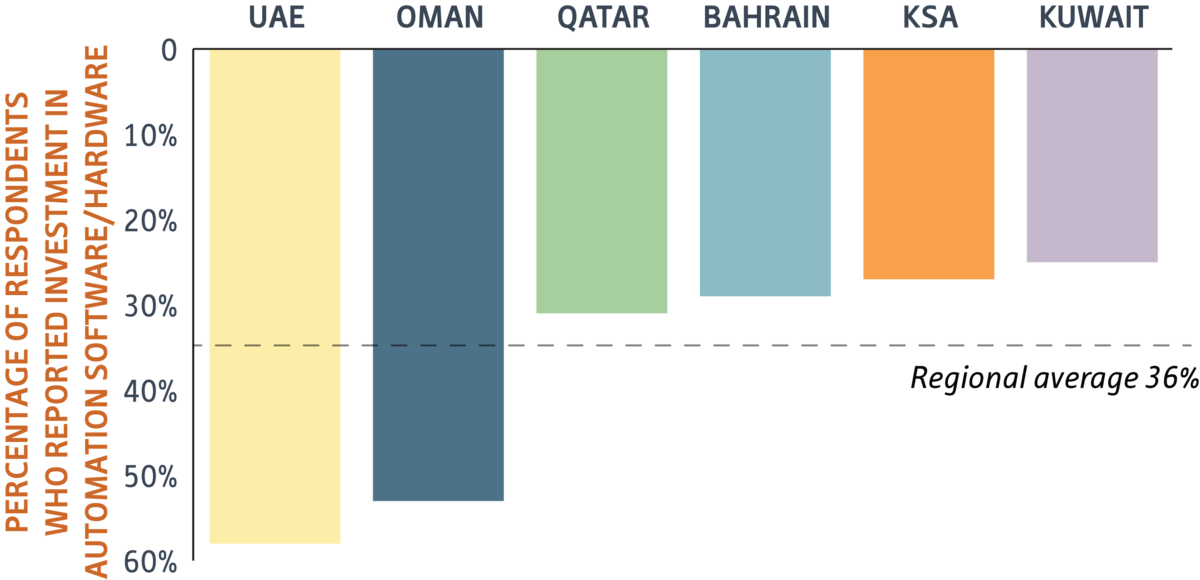

The private sector response was also related to investment in digital technology. According to OBG’s Gulf Covid-19 CEO Survey, conducted in July, 36% of CEOs said they had invested in automation software or hardware, with the figure almost 60% in the UAE.

As a region with a high proportion of oil-producing and exporting countries, the Middle East was disproportionately affected by Covid-19.

The region’s economy is expected to contract by 6.6% in 2020, according to estimates from the IMF, a larger downturn than the global average of -4.4%. Looking ahead, the fund expects the Middle East to rebound to growth of 2.6% in 2021, below the global forecast of 5.2%.

Oil and travel key to rebound

Notwithstanding the considerable efforts towards economic diversification in various countries, the region’s short-term recovery is likely to be closely linked to the price of oil.

Underlining this, 67% of respondents in OBG’s Gulf Covid-19 CEO Survey said that oil prices will either significantly or very significantly impact their respective economic recoveries.

Another key factor will be the resumption of travel.

With countries such as the UAE, Qatar and Bahrain home to significant leisure and entertainment sectors, often closely tied to their respective aviation industries, the severe restrictions on cross-border travel throughout 2020 have taken their toll.

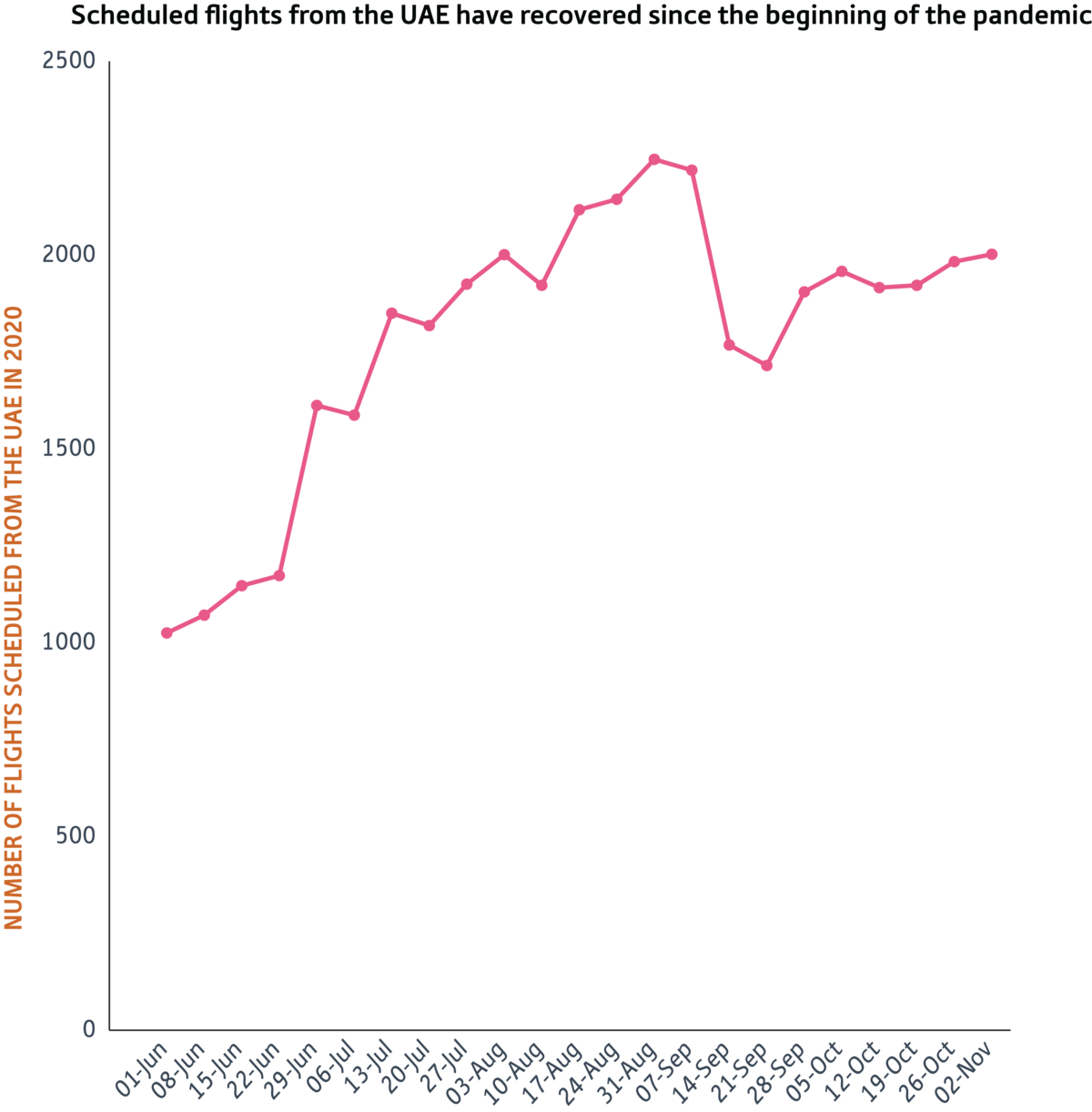

Although badly affected overall, there was a gradual recovery in aviation activity in the second half of the year.

The number of flights from the UAE doubled between the beginning of June and early November – and while the number of passengers handled at Dubai International Airport was down 70% year-on-year in October, at 1.6m, this was around 25% higher than the previous month.

Although airlines have implemented strict temperature controls and social-distancing protocols to encourage travel, most industry stakeholders believe that significant progress will only be made once an effective vaccine is widely available.

To this end, the development – and in some cases initial deployment – of Covid-19 vaccines bodes well for 2021.

Aside from freeing up travel, the vaccine could provide business opportunities for logistics companies in the region.

Kuwaiti logistics firm Agility Public Warehousing is in discussions with governments and vaccine producers to help distribute doses once they become available.

The company, which has a logistics network covering 120 countries, says it has significant cold storage capability in many emerging markets, something that is crucial considering that the Pfizer and BioNTech vaccine must be stored at the ultra-low temperature of -80°C to work effectively.

With the region particularly affected by the economic fallout of the pandemic, a number of countries have sought to make structural reforms to provide a more stable platform for future prosperity.

Given their reliance on hydrocarbons revenue, many governments have reassessed – and in some cases accelerated – their long-term plans for economic diversification.

Although the downturn has prompted the Saudi government to reduce the budget for implementing Vision 2030, its long-term economic development plan, the country is pressing ahead with efforts to generate new revenue streams.

In May the government awarded the Public Investment Fund (PIF), the Kingdom’s sovereign wealth fund, an additional $40bn in government reserves to tap investment opportunities.

Over the past few months the PIF has invested in a wide range of companies across different industries, including Uber, Softbank’s Vision Fund, electric carmaker Lucid Motors, Disney and Bank of America.

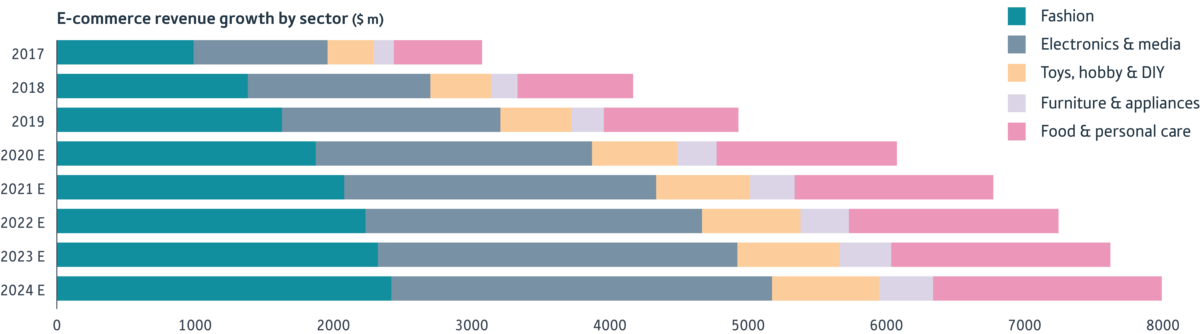

In a sign that these investments, particularly those in the digital payments space, are on track to bear fruit, data analytics agency Statista estimates that e-commerce revenue in the Kingdom will rise from $5bn in 2019 to around $6bn this year, with the figure set to reach as high as $8bn in 2024.

Mubadala Investment Company, Abu Dhabi’s private investment vehicle, has also made a series of strategic investments in sectors such as tech and renewable energy. These include $3bn in Waymo, Alphabet’s self-driving technology arm; $700m in US start-up Reef Technology, which manages logistics centres and neighbourhood kitchens; and $235m in German pharmaceutical company Evotec.

Increased taxes

Although many governments waived certain tax payments in the immediate aftermath of the pandemic, some have in recent months sought to broaden their revenue base by increasing tax collection.

As part of the Omani government’s fiscal plan for 2020-24, released in October, policymakers outlined efforts to improve tax collection efficiency and introduce a value-added tax in 2021. For the first time, the government is also considering the establishment of personal income tax.

This trend was also seen in Saudi Arabia, which tripled its value-added tax rate in July, from 5% to 15%.

While these changes are often direct reactions to the crisis, they may prove to be the forerunners of longer-term tax reform.

Manufacturing

Another development that could provide the region with a platform for reinvention is the global shift towards more diversified supply chains and industrial capacity.

Although a number of companies had in recent years already embarked on a so-called China +1 strategy – whereby firms seek to diversify production capacity by setting up factory lines in other countries while maintaining significant operations in China – the process is expected to accelerate following Covid-19.

Indeed, as the most recent OBG Gulf CEO Survey results show, 33% of respondents believed the crisis would bolster industry and manufacturing in their domestic markets. In turn, this should strengthen the region's resilience against future shocks to global supply chains.