– Thailand and Malaysia led the region in terms of government stimulus

– Key digital solutions were developed in food delivery, education, health care and finance

– Despite falling globally, M&A increased in Asia throughout the year

– Emerging markets in ASEAN stand to benefit from the supply chain shift away from China

Closely linked both geographically and economically to China, the epicentre of the novel coronavirus outbreak, emerging markets in Asia were among the first to feel the effects of Covid-19 in 2020.

The year has undoubtedly been a difficult one, with the virus disrupting both daily life and the economy for months. However, the largely successful containment of the virus in most countries, the development of new digital solutions and the move to diversify supply chains away from China have left the region well positioned to capitalise on the post-pandemic changes in the global economic landscape.

Using OBG Advisory’s “4R” matrix for analysing national Covid-19 responses – encompassing Resilience, Response, Recovery and Reinvention – we highlight success stories and lessons from the region over the year, and look ahead to 2021.

Asian countries’ levels of resilience to the pandemic varied in line with their respective levels of economic development.

More developed economies with strong health care systems and financial reserves, such as Japan and South Korea, were naturally better prepared to manage the health and economic effects of the crisis.

Others with weaker infrastructure and lower average disposable incomes faced a more challenging proposition. To take an example, while Myanmar has experienced strong economic growth in recent years – averaging 6.6% annually between 2010 and 2019, according to the IMF – and invested significantly in health care infrastructure, it still lags behind other economies in the region and was therefore vulnerable to any significant outbreak of the virus.

Some emerging markets were better suited to cope with the pandemic than others. In particular, Thailand was already well established as a regional medical hub before the pandemic, positioning the country in good stead to manage the health impacts of the crisis.

The country is a regional leader in the provision of quality private medical facilities, according to US-based Joint Commission International (JCI). Last year it had 66 JCI-accredited hospitals, nearly double the number in the second-placed Asian country – India, which had 38.

In addition, Thailand was ranked the fifth-most medically resilient country in the world, according the 2019 Global Health Security Index, the only middle-income country to place in the top 10.

Economic resilience

Generally speaking, more diverse and digitalised economies were better able to withstand the challenges accompanying Covid-19.

For example, Malaysia, with its high-tech industry and strong services sector, has a more diversified base than some of its ASEAN neighbours, and was thus better prepared to absorb the losses associated with the economic downturn. Nevertheless, the economy is still forecast to contract by 6% in 2020 before rebounding to 7.8% growth in 2021 – the fastest rate among the ASEAN-5 countries.

Elsewhere, Thailand's key industries were badly affected by the pandemic. Heavily reliant on tourism and exports, the country was hit particularly hard by the closure of international travel and the drop in global demand for goods, with GDP falling by 12.1% and 6.4% year-on-year (y-o-y) in the second and third quarters, respectively.

Similarly, the Philippines continues to face challenges. The country imposed strict lockdown measures, with considerable restrictions in place until the end of the year. Moreover, the economy is heavily reliant on overseas remittances, which account for around 9% of GDP, and – with some 250,000 of the country’s 12m overseas foreign workers sent home over the course of the year as a result of the pandemic – remittances fells by 2.6% y-o-y in the first eight months of 2020.

While all countries have faced challenges in coping with the disruption, most had specific features that helped strengthen their resilience to the pandemic in one way or another.

In Indonesia, high foreign currency reserves and relatively low government debt before the outbreak – at 29.8% of GDP – provided fiscal stability, while the Philippines' stable credit rating and strong track record of external debt repayments helped it to alleviate some of the economic pressures through borrowings. Meanwhile, the dynamism of digital industries in Thailand, Malaysia and Indonesia allowed these countries to effectively pivot towards digital payment, e-health and online education services.

Given that the virus originated in China, Asian countries were among the first to experience – and thus respond to – outbreaks of Covid-19.

On January 23 the Chinese government implemented a strict lockdown in Wuhan and nearby cities to contain the virus. Although severely restrictive, the measures were credited with slowing the spread from the epicentre.

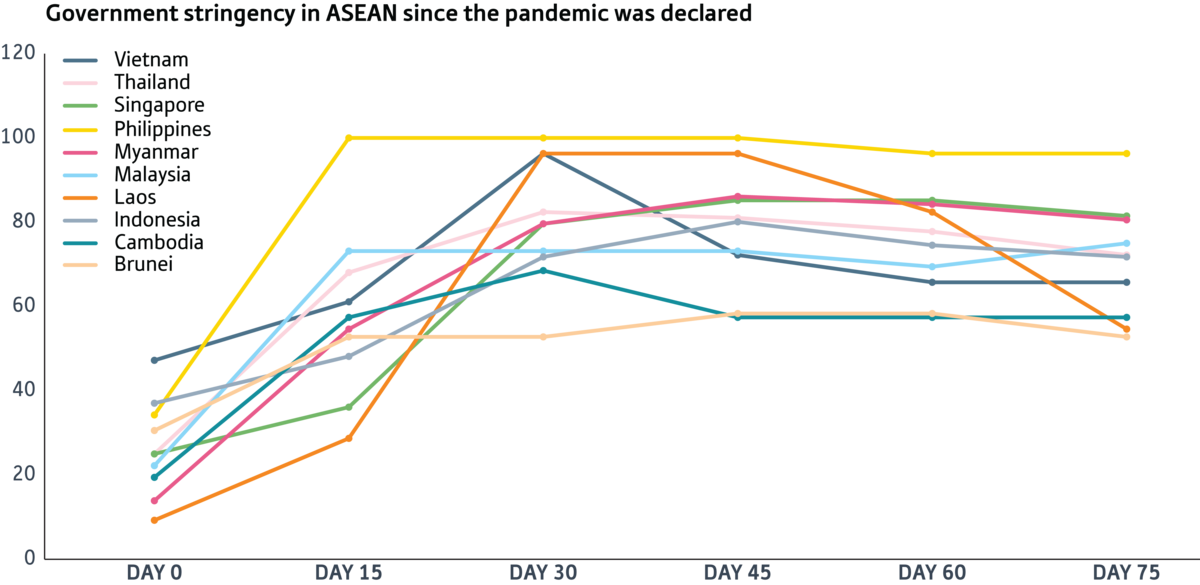

As the virus nonetheless spread to other countries in the following weeks and months, governments across Asia implemented lockdowns and restrictions on the movement of people and goods.

While most strategies consisted of broadly similar measures, some were stricter than others. Among those with tighter restrictions was the Philippines, whose enhanced community quarantine – imposed on the island of Luzon – severely restricted the movement of people, except for essential work and health purposes, and led to the closure of all businesses deemed non-essential.

By and large, the region has been reasonably successful in slowing the spread of the virus, particularly when compared to other parts of the world.

For example, as of November 29 the total number of infections in Vietnam – a country with a population of around 95m – was just 1343, while virus-related deaths numbered 35. Thailand was another success story, with infections and deaths standing at 4000 and 60, respectively.

Malaysia and Myanmar, with 65,700 and 89,500 respective totals of infections, have fared far better than countries with similar populations elsewhere in the world, while even China, which had a dramatic early spike in cases, has managed to restrict the total infection count to around 86,500.

In absolute terms, Indonesia has been the most affected on a medical level in East Asia, with 539,000 cases and 17,000 deaths, followed by the Philippines, with 432,000 and 8400, respectively. However, the large populations of these countries – with Indonesia at 270m and the Philippines at 108m – must be taken into account.

Institutional response

Aside from the medical crisis, governments and other key institutions in Asia responded to the subsequent economic fallout.

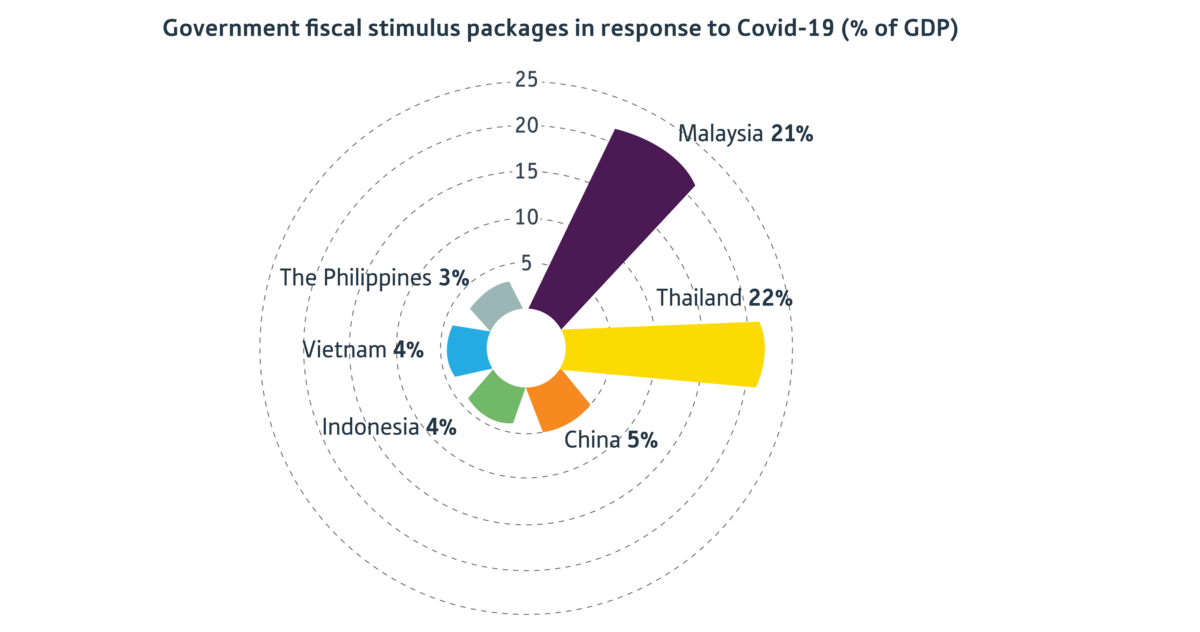

While all countries implemented some form of stimulus plan or state support package, these varied in scope and focus.

For example, stimulus measures released by Thailand’s government were proportionally the largest in the region, equivalent to 22% of GDP. This was closely followed by Malaysia, which offered support totalling 21% of GDP through its various packages.

These measures went far beyond most others in the region, with the fiscal stimulus offered by China (5%), Indonesia (4%), Vietnam (4%) and the Philippines (3%) being considerably lower.

Support funds were typically followed by central bank efforts to boost liquidity. Thailand, Malaysia, the Philippines and Indonesia all reduced their benchmark rates to record lows throughout 2020, at 0.5%, 1.75%, 2% and 3.75%, respectively.

Business response

Digital solutions were essential in enabling businesses to adapt to the new normal.

Given the restrictions on movement and social distancing guidelines, the expansion of online platforms offering payment, food delivery and medical advice was not only key to providing basic goods and services to the general public, but also a necessity for companies looking to adapt to rapidly changing demand.

“While e-commerce was just an option before Covid-19, it is now essential for retailers and producers to sell their products through e-commerce platforms in order to survive,” Kusumo Martanto, CEO of Indonesian e-commerce platform Blibli, told OBG in April. “The long-term impact will be positive for online shopping, as it will start to become habitual for consumers.”

Such a phenomenon was clearly evident in Indonesia, South-east Asia’s largest digital economy and home to five of the region’s 11 unicorns.

In addition to online platforms Gojek (Indonesia) and Grab (Singapore) adopting contactless delivery payment methods, innovations were made in other areas.

For example, in March local company Halodoc teamed up with Gojek to launch a telemedicine service called Check Covid-19, which allows Gojek users to remotely check their symptoms with the 20,000 doctors in the Halodoc system, helping to reduce the risk of further transmission.

Elsewhere, educational technology firm Ruangguru launched the Ruangguru Online School Programme, offering daily virtual classes to students of all grades via the company’s platform.

For Asia, the region’s ability to control infections has been key to facilitating economic recovery.

According to IMF growth projections released in October, the Asia-Pacific region is expected to contract by 2.3% this year. Although this will prove the worst performance for more than 40 years, it is still above the global forecast of -4.4% for 2020.

Despite the considerable economic and social upheaval caused by Covid-19, Myanmar (2%), China (1.9%) and Vietnam (1.6%) are still expected to record growth this year.

Much of this resilience was due to the performance of digital services. According to the “e-Conomy SEA 2020” report, released by Google, Singapore’s Temasek and US consultancy Bain and Company in November, the internet economy in South-east Asia is set to expand by 5% this year, to a gross merchandise volume of $105bn.

Looking ahead, the region is tipped to grow by 6.7% in 2021, above the global average of 5.2%.

M&A activity

The recovery in sentiment has been reflected in mergers and acquisitions (M&A).

Although global cross-border M&A fell by 15% y-o-y in the first nine months of the year, according to the UN Conference on Trade and Development, comparable activity in Asia rose by 60% y-o-y over the period.

Just as has been seen on a global scale, much of the M&A activity has been focused on virus-resilient industries like ICT and health care.

As many analysts have pointed out, M&A has in many cases been the perfect strategy for cash-strapped start-ups and larger companies looking to make cheaper strategic investments.

This approach has been evident among the region’s super apps.

Demonstrating the shifts in customer activity over the past year, the “e-Conomy SEA 2020” report found that while the food delivery (34%), online grocery (33%), education (22%) and video streaming (21%) segments all increased significantly, the previously core function of the apps – ride-hailing services – fell by 13%.

While in recent years these apps – led regionally by Gojek and Grab – have sought to expand their offerings, Covid-19 has forced them to reassess their plans, with many looking towards consolidation rather than expansion.

For example, in June Gojek announced that it would lay off 9% of its workforce and close GoLife, which offered household cleaning and on-demand massage services, as well as GoFood Festivals, the arm that operated physical food halls.

Grab also laid off 360 employees – around 5% of its workforce – and announced it would close some “non-core projects”.

The economic realignment caused by the pandemic has led the companies to refocus on their core businesses, which Fitch predicts will be ride-hailing, food and grocery delivery, and payments.

To this end, in February Grab purchased fellow Singaporean start-up Bento, a ‘wealth-tech’ business advisory company, while Gojek acquired Indonesian point-of-sale start-up Moka in April and Vietnamese e-payment start-up WePay in September.

Notwithstanding the challenges associated with coronavirus, the region stands to benefit from post-pandemic opportunities.

With much of the world’s production capacity based in China, virus-related restrictions on trade laid bare the risks associated with highly concentrated supply chains. This has in turn encouraged many companies to diversify their industrial and logistical operations.

As OBG has detailed, this process, known as China +1, was already under way before the outbreak of Covid-19, as rising labour costs and tariffs associated with the US-China trade war saw some companies relocate business operations.

Given their proximity to China, developed industrial sectors and low labour costs, a number of emerging markets in the region have become frontrunners in the race to attract industrial activity.

For example, in May regional media reported that US tech giant Apple was set to shift the production of around 30% of its AirPods from China to Vietnam. This was followed by a report from international media in November that plans were also in motion to relocate iPad and MacBook production to the country.

Elsewhere, in late November the Philippines’ Senate approved a bill that will immediately slash corporate tax from 30% to 25% and offer a series of incentives to major projects.

Similarly, in October Indonesia’s Omnibus Bill on Job Creation – aimed at reducing red tape and incentivising investment – was passed into law.

In Thailand, meanwhile, the Eastern Economic Corridor special economic zone is set to play a key part in the government’s goal to transform the country into a regional centre for high-tech manufacturing and digital innovation.

With a series of incentives for potential investors and ongoing efforts to update logistical and industrial infrastructure, the zone also represents a major attraction for companies looking to diversify industrial production away from China.

Moving forward, this broader shift away from China, coupled with the incentives offered by governments in ASEAN, could see the region become a major producer of next-generation industrial products.

RCEP and closer regional ties

In a further boost to recovery prospects, on November 15 the 10 ASEAN countries, along with Australia, China, Japan, New Zealand and South Korea, signed the Regional Comprehensive Economic Partnership (RCEP).

With its members making up around 30% of the world’s population and GDP, RCEP will become the world’s largest trade bloc.

The deal, which is a major vote of confidence in multilateralism and bucks the recent trend towards protectionism, aims to eliminate 90% of import tariffs between signatories within 20 years, and establish common rules for e-commerce, trade and intellectual property.

These closer ties should act as an additional incentive for companies looking to invest in the region, and at the same time allow Asian firms to expand more easily into neighbouring markets.

Given that many Asian countries, particularly those in ASEAN, are actively courting large-scale industrial investment, closer trade ties bode well for future growth.