How is Oman working to diversify away from hydrocarbons?

30 Apr 2018

When I wrote about a year ago on the findings of our inaugural Oxford Business Group Business Barometer: Oman CEO Survey, I talked of the “no pain, no gain” scenario for the sultanate’s planners. Our findings back this up – if anything, more explicitly – 12 months later.

Oman traditionally has neither experienced the same highs as some of its GCC neighbours, nor has its economy bottomed out so dramatically. Indeed, it has earned a reputation for prudence and moderation in its economy and politics, where it has regularly acted to bridge regional tensions.

Although oil prices rose in the first quarter of 2018, with Brent crude currently trading at $72 per barrel, Oman’s finances have taken a significant hit in recent years.

So while it is welcome news that the current account deficit narrowed over the first 11 months of 2017 to OR3.3bn ($8.6bn) from OR4.9bn ($12.7bn) in the same period of 2016, this remains a concern.

Indeed, the credit ratings agencies have all reflected this in their sovereign ratings for the sultanate, with the Big Three downgrading Oman in the past six months. This will affect its cost of borrowing, and likely investor sentiment.

Economic growth accelerates with hydrocarbons rebound

The contribution of hydrocarbons as a percentage of GDP has fallen in recent years. However, this is more a reflection of reduced prices than a realignment; as prices have recovered, so too has the sector’s contribution. Having accounted for 46.4% of GDP in 2014 and 27.1% in 2016, the figure rebounded to 32.5% in the first half of 2017 as oil prices strengthened.

All of this underscores the sultanate’s continued dependence on hydrocarbons and the importance of maintaining its drive towards diversification. All GCC states – and indeed any country that relies on a single commodity for the bulk of their income, as many of the markets OBG covers do – battle with this.

Any of us who watch the GCC markets will be familiar with the various initiatives to diversify income away from oil and gas, and encourage the private sector to play a more prominent role. Oman is no different.

Nor is it any different in the challenges it faces in making the changes necessary to enable this. Autonomous private sector growth is far from easy to achieve. Furthermore, the authorities have had to streamline spending and reduce subsidies in efforts to curb their accruing deficits.

In turn, this has meant that the private sector – the identified antidote – has been negatively affected. This should not be any surprise to us.

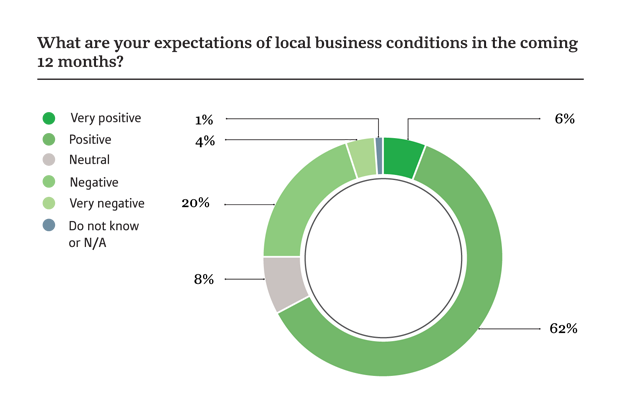

As we have seen elsewhere in the GCC, notably in our recent OBG Business Barometer: UAE CEO Survey, the benefits of the oil recovery are taking time to translate to the non-hydrocarbons private sector. It is therefore interesting that some 68% of our respondents had either positive or very positive expectations of local business conditions in the coming 12 months.

This will undoubtedly be welcome news for the authorities and supports the IMF’s more robust real GDP growth projection of 3.7% for 2018, up from a 0.02% contraction in 2017.

Tax reforms influence investor sentiment

While many of the businesspeople we speak to in the sultanate recognise the importance of introducing value-added tax (VAT) as part of the broader GCC initiative, the delay in its implementation sends mixed messages.

On the one hand, it is understandable that businesses need time to put systems in place to process VAT. On the other hand, it is one more year in which the Treasury misses out on much-needed income: the IMF predicts $1.3bn per year could be generated by the tax, equivalent to 1.7% of GDP.

The government has, however, said that it will implement other taxes sooner, such as the so-called sin tax on sugary drinks slated for this summer.

Over 80% of survey participants felt that Oman’s overall tax environment was either competitive or very competitive on a global scale, despite the imminent taxation plans.

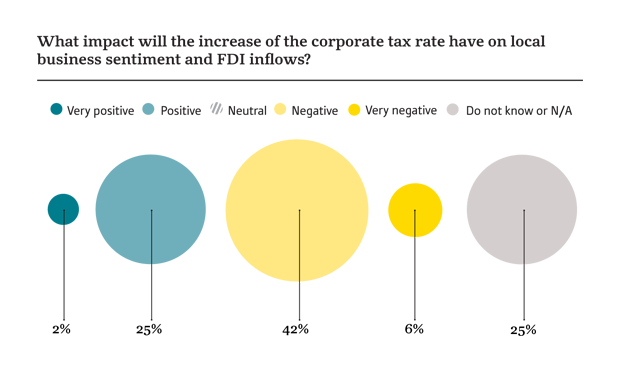

However, 42% – by far the largest portion of respondents we spoke with – felt the increased corporate income tax rate (from 13% to 15% in February 2017) would have a negative impact on business sentiment and foreign direct investment flows. A further 6% felt it would be very negative, and 25% thought it would be positive.

Herein lies the conundrum for Oman’s government. It is vital that alternative sources of revenue are raised – with VAT having the added advantage of increasing reporting and thereby transparency – but at the same the business community sees it as harmful to raise taxes for private sector companies already feeling the trickle- down effects of lower oil prices.

However, it is worth revisiting the broader taxation question, where the environment is overwhelmingly considered competitive: VAT is 19% in Germany and 20% in the UK. It’s all relative.

While some believe the new levy could have negative effects, this is of course a sentiment survey, and it will be interesting to see in a year’s time if these negative feelings towards the increased corporate tax persist.

Although the survey’s findings were broadly positive, it identifies clear areas drawing CEOs’ attention and concerns. Economic diversification has taken on a renewed focus, but the conditions for this to succeed will require a delicate balancing act.

While progress along this road has been made, of those OBG surveyed, 71% identified oil prices as the top external factor that could affect the sultanate’s medium-term growth. Regional political volatility came in second, at 20%. Not only does this reflect the continued centrality of hydrocarbons to sentiment, but it also seems a clear indication of how much more progress is needed.

Covid-19 Economic Impact Assessments

Stay updated on how some of the world’s most promising markets are being affected by the Covid-19 pandemic, and what actions governments and private businesses are taking to mitigate challenges and ensure their long-term growth story continues.

Register now and also receive a complimentary 2-month licence to the OBG Research Terminal.

Register Here×