CEOs in the UAE Optimistic as the Country Enters a Period of Tax Reform and Economic Rebound

10 Apr 2018

While recently introduced, a new value-added tax (VAT) – previously a relatively contentious issue – has raised hopes in terms of public revenue generation and transparency.

The UAE, along with Saudi Arabia, implemented the flat 5% tax on January 1, 2018, becoming the first in the GCC to do so. This move will serve as a valuable example for the other Gulf countries, which pushed their VAT implementation to 2019.

Our second and most recent survey of top executives in the UAE, the Oxford Business Group Business Barometer: UAE CEO Survey, offers some early insights into the ways business leaders are interpreting these developments.

Taxes to boost public revenue

The year 2017 was one of consolidation in the UAE, with both the federal government and individual emirates continuing to streamline spending in a time of lower oil prices and government income.

In this regard, VAT will provide a valuable contribution to government revenue and – as I have written before – represents an important maturation of policy. The tax is set to generate $3.3bn in 2018 and $5.4bn in 2019, according to IMF estimates, and arguably more importantly, will enable the authorities to assess and track businesses and spending in a way that has not been possible before.

While VAT was responsible for a one-off uptick in inflation of 2.67% month-on-month in January, it seems to have had a relatively moderate impact on retail spending so far.

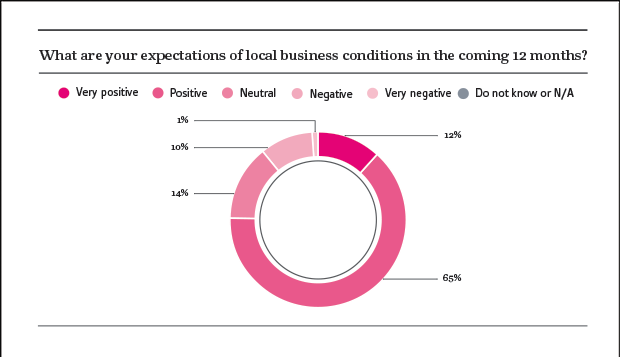

This may help maintain bullish sentiment among business leaders: 76% of those surveyed had positive or very positive expectations of local business conditions in the coming 12 months.

Furthermore, it is important to remember that the UAE’s free zones, particularly the more than 20 in Dubai, offer either zero or minimal taxation, as well as tailored regulatory environments for businesses established there, which will be largely unaffected by VAT.

It is perhaps unsurprising, therefore, that 89% of CEOs described the local tax environment as competitive or very competitive relative to the wider region, when surveyed in the months leading to the January implementation of the tax. Moreover, with VAT to be levied at a relatively low rate of 5% – compared to 19% in Germany, for example – many executives felt it was unlikely to significantly impact the cost of doing business.

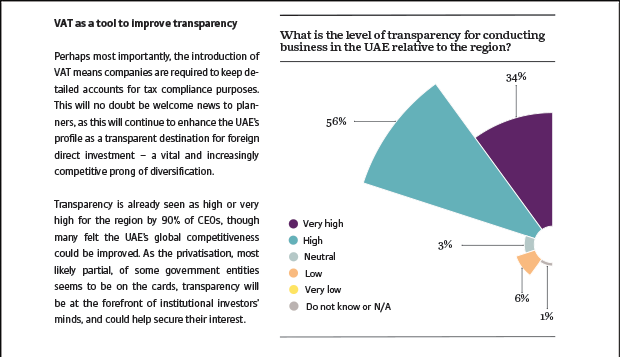

VAT as a tool to improve transparency

Perhaps most importantly, the introduction of VAT means companies are required to keep detailed accounts for tax compliance purposes. This will no doubt be welcome news to planners, as this will continue to enhance the UAE’s profile as a transparent destination for foreign direct investment – a vital and increasingly competitive prong of diversification.

Transparency is already seen as high or very high for the region by 90% of CEOs, though many felt the UAE’s global competitiveness could be improved. As the privatisation, most likely partial, of some government entities seems to be on the cards, transparency will be at the forefront of institutional investors’ minds, and could help secure their interest.

Services and trade to drive diversification

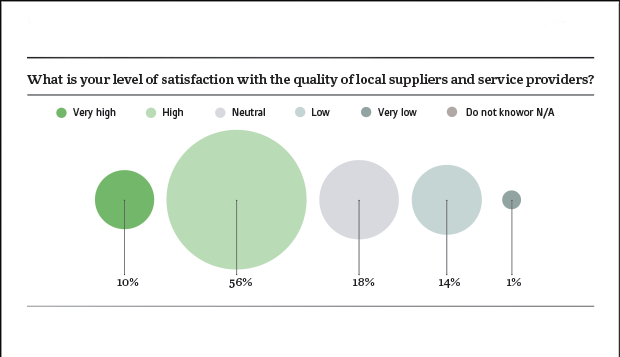

CEOs already find the local business environment largely favourable in regional terms: around 66% had high or very high levels of satisfaction with the quality of local suppliers and service providers relative to the region.

However, given the prominent role of services, particularly in Dubai, but more broadly as part of diversification efforts, this shows that there’s room for improvement, particularly as this is an area every market is looking to compete in. The UAE has significant competitive advantages in this regard, not least as one of the best-established transport and logistics hubs: it is just eight hours’ flying time from two-thirds of the world’s population.

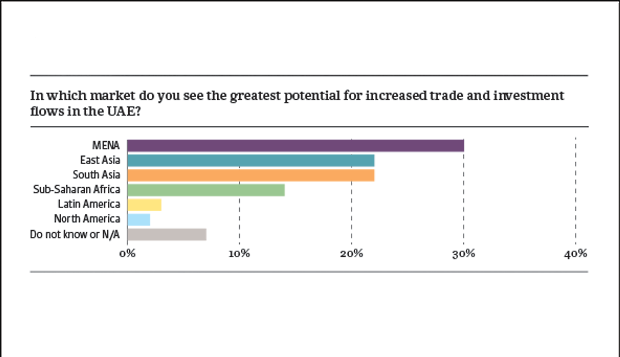

So while the MENA region was identified by the plurality (30%) of respondents as having the greatest potential for trade and investment flows, it was particularly interesting to see that areas further afield were ranked so highly: collectively, South Asia and East Asia accounted for 44% of responses, while sub-Saharan Africa received 14%. With the 2018 Global Business Forum on Latin America hosted in Dubai in late February, after the survey concluded, it will be interesting to see if Latin America’s position, currently at 3%, improves in subsequent editions of the Business Barometer.

Economic rebound on the cards

Infrastructure spending at the federal and emirate level has underpinned both foreign trade and economic development. The Central Bank of the UAE estimates GDP growth was around 1.5% in 2017. Crucially, the non-oil sector – vital to the UAE’s diversification strategy – is bearing fruit, with non-oil GDP having significantly outpaced headline growth, at 2.9%.

Despite last year’s challenges, economic expansion appears set to bounce back: the IMF and others have significantly higher projections for 2018, of between 3.4% and 3.6%, broadly in line with the global average. Executives, however, reported a somewhat less optimistic outlook: less than one-quarter anticipated GDP growth of 3% or higher in the coming 12 months.

Sentiment is, of course, about the here and now: what CEOs are experiencing at a particular moment. Importantly, the benefits of steadier oil prices may not have trickled down to all business yet, which could help to explain their lower growth projections.

Although some challenges persist, such as translating more stable yet lower oil prices into a new economic model, managing the cost and quality of services and regional political volatility – which two-thirds of participants identified as the top external risk factor – the conclusions are largely, if cautiously, upbeat.

As with VAT, regional political volatility will have already been built into most business plans and pricing; it is the macroeconomic environment that will likely be most important to businesses over the next 12 months.

Covid-19 Economic Impact Assessments

Stay updated on how some of the world’s most promising markets are being affected by the Covid-19 pandemic, and what actions governments and private businesses are taking to mitigate challenges and ensure their long-term growth story continues.

Register now and also receive a complimentary 2-month licence to the OBG Research Terminal.

Register Here×