Adapting to Change: Qatar’s CEOs Identify Alternative Solutions Going Forward

04 Feb 2018

As I write this in January 2018 and look back to a year ago, the economies of the GCC were hoping that oil prices had bottomed out and that the next 12 months would herald greater market stability.

While it would take until the early summer for oil prices to stabilise and settle, albeit at rather more muted levels than their heady highs a few years previous, Gulf watchers anticipated a moderate year of growth. This was in large part down to much lower oil incomes, which remain the central engine of economic growth despite diversification efforts.

Initiatives to boost non-oil and autonomous private sector growth have begun to bear fruit, but not as rapidly as planners would like. The reduced state coffers across the region have added greater emphasis to policymaking with regard to driving diversification, and in turn streamlining government spending. In short, 2017 was always going to be a year of continued consolidation.

Business sentiment grows more positive after blockade

So, when in June Saudi Arabia, the UAE and Bahrain announced a boycott of Qatar, something that would have been dramatic in any event, their actions took on even greater economic weight.

However, as OBG’s Business Barometer: Qatar CEO Survey, a review of more than 100 CEOs in Qatar interviewed both before and after the blockade, shows, the impact has been far less negative than one might have expected.

On one level, while it is possible to argue that the overall positive sentiment may well be a reflection of rather jingoistic CEOs, the reality is that in an anonymous survey this is a less convincing argument.

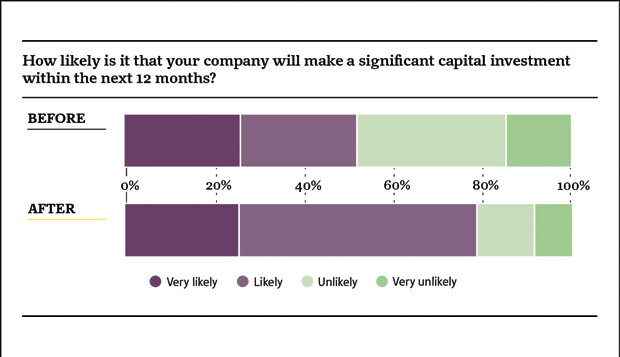

Case in point: of the CEOs surveyed after the boycott began in mid-June, nearly 80% said they were likely or very likely to make a significant capital investment; before June this was about 50%.

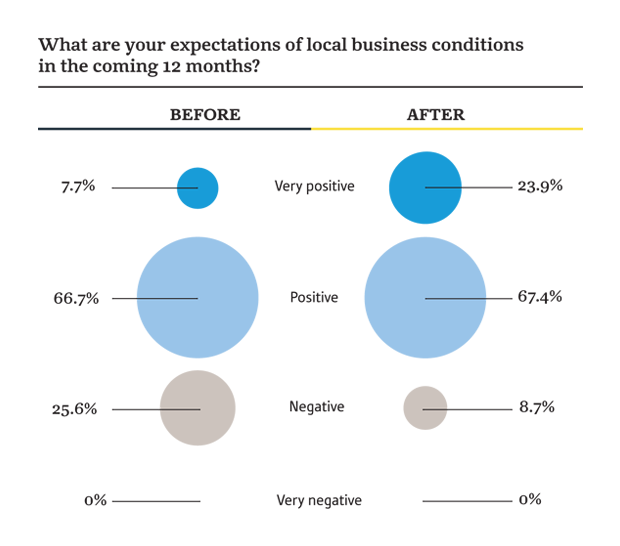

Similarly, our results show that after the boycott, sentiment with regard to local business conditions actually increased. Indeed, before the embargo 25.6%

of respondents said they were negative about local business conditions in the upcoming year; afte June this figure dropped to 8.7%.

One might think that for an economy that has traditionally relied on importing much of its raw materials and supplies from neighbouring Saudi Arabia, satisfaction regarding local suppliers post-embargo would have been lower than before. In fact, as with other findings, the opposite is true: the number of respondents who

were satisfied with local suppliers increased by nearly 15 percentage points post-blockade.

So it seems fairly clear that, if anything, the current situation has led local businesspeople to feel more upbeat about their prospects rather than less.

Adaptation remains key

Indeed, the speed and ease at which Qatar has managed to find alternative sources for goods previously imported from GCC neighbours has no doubt boosted business sentiment, not to mention resourcefulness.

Faith in business practices was also rated highly by all respondents, with nearly 80% saying the level of business transparency was either high or very high relative to the broader region.

![]()

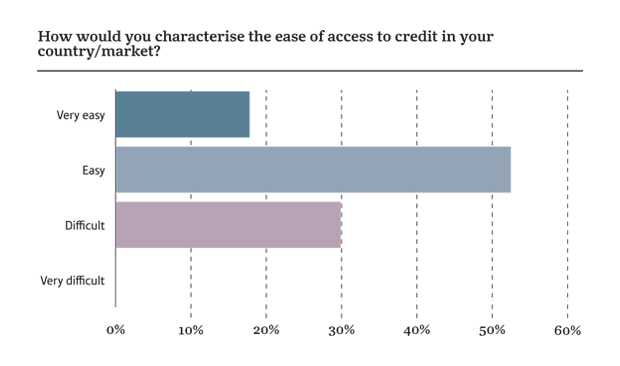

However, anecdotally and in our many meetings, one area which often seems to be of concern is access to credit. Some 30% of our respondents said it was difficult to get financing, while the remaining 70% said it was either easy or very easy.

This finding is broadly in line with other GCC economies, but this is particularly important for the development of a stronger non-oil economy. In the Gulf, many private sector businesses have traditionally benefitted from their proximity to significant family wealth or patronage, the classic example being family holding companies, a near ubiquitous model in the region. While that continues to be the case, its prevalence is decreasing. Furthermore, a combination of succession planning and younger generations taking over sections of these large established businesses, as well as the growth of smaller stand-alone start-ups, has lead to greater demand for credit.

The result of this is that the headline figure in this particular finding perhaps hides the difficulty for those businesses without family backing and support – the classic start-up, for example – when they try to get credit. Banks will understandably favour a well-known business with years of balance sheets over a new venture.

However, for the sort of economic transformation Qatar and other GCC countries are looking to stimulate, this is one area where the authorities will no doubt be seeking improvement.

Alternative routes and methods embraced by local businesses

It is undoubtedly in everyone’s interest that a solution to the current political stand-off between Qatar and its GCC neighbours be found. However, for the time being, these results show that the business community feels perfectly capable to carry on with business, if not quite as usual, then via alternative routes – just like the supply chain.

As I have already said, there is perhaps an element of defiance in some of the responses, but this can only account for a proportion of the overall upbeat nature of the findings.

Despite the knocks that globalisation has taken over the past 18 months, not least with the rhetoric of US President Donald Trump, and the clear messages to this end evidenced in European elections and the vote for Brexit in the UK, the increasingly interconnected nature of global markets and the ease with which trade and

commerce is done means that new partners and different routes can easily be identified and exploited.

It will be interesting to see how sentiment is holding up when we look at the results of the OBG Business Barometer: Qatar CEO Survey this time next year.

Covid-19 Economic Impact Assessments

Stay updated on how some of the world’s most promising markets are being affected by the Covid-19 pandemic, and what actions governments and private businesses are taking to mitigate challenges and ensure their long-term growth story continues.

Register now and also receive a complimentary 2-month licence to the OBG Research Terminal.

Register Here×