How Mexico’s economic trajectory is polarising CEO opinion

16 Dec 2019

In a global political economy characterised largely by trade wars, polarised politics and economic populism, Mexico – despite being substantially affected by all three of these – has managed to remain impressively resilient in the face of what the IMF refers to “as an environment of elevated external and domestic risks”. Externally, the sluggish global economy and the trade war between the US and China coincided with instances throughout 2019 of US President Donald Trump using Twitter to be highly critical of Mexico’s internal and foreign policy. Looking at domestic political issues, at 60% the consistently resilient approval ratings of president Andrés Manuel López Obrador, known as AMLO, are in contrast to the heightened uncertainty with which the business community views his policies.

Following the publication of our CEO Survey on the country in June 2019, in this sixth edition we have looked to explore trends in ongoing issues with business leaders and poll them about new topics, such as the labour reform and their views on the structural challenges holding back economic growth.

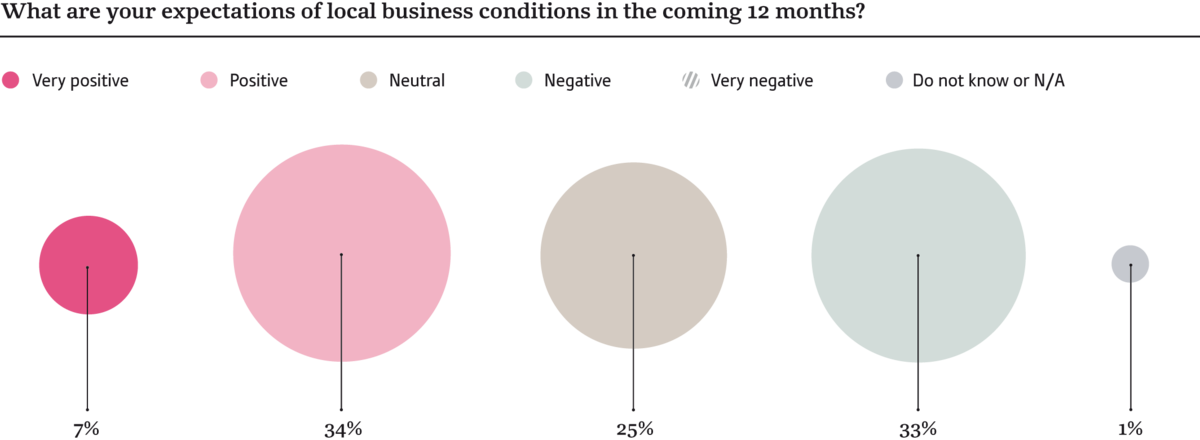

In our latest survey, the first observation is that business leaders’ opinions are much more polarised than before. The number of neutral responses fell from 39% to 25% when asked about expectations of local business conditions. Furthermore, more respondents were negative than in our previous survey, rising from 19% to 33%, while those answering positive fell slightly from 37% to 34%. By contrast, the number of very positive responses nearly quadrupled, growing from 2% to 7%, and those answering very negative fell from 3% to 0%.

This varied picture most likely reflects the diverging fortunes of the Mexican economy and, as a result, the possible paths it may take during the following 12-month period. According to even the most positive forecasts, the country may not achieve 1% growth this year. However, delving deeper into the growth figures for each state, a more varied picture emerges. While the border state of Chihuahua in the country’s north grew at a year-on-year rate (y-o-y) of 4% in the second quarter (the president’s current goal for the entire nation), some states – such as oil-dependent Tabasco – declined by 10.3%. Overall, the country’s economy grew by 0.3% in the same three months.

The diverging range of opinions can also be interpreted by the varying degrees of success reported by different economic sectors. While aerospace continues to post double-digit growth, delays to the energy reform have meant that oil production in the country is still in decline. With such varied outcomes for both states and sectors, it is understandable that CEOs’ opinions are shifting in different directions.

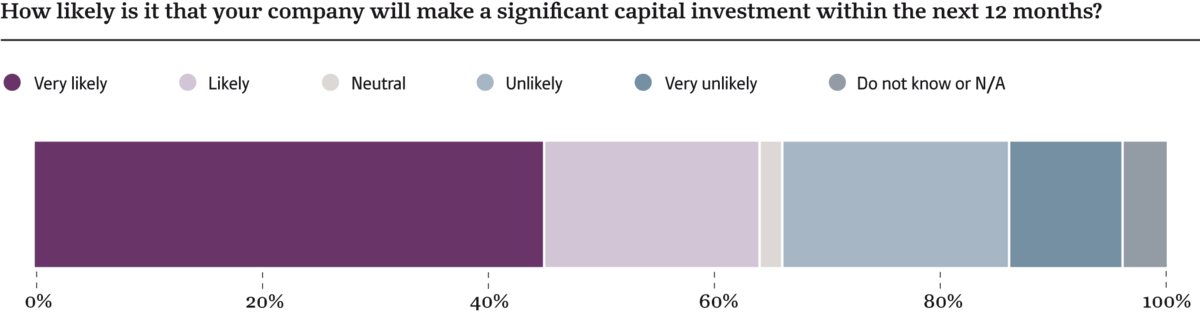

The theme of polarisation is also apparent in the question “How likely is it that your company will make a significant capital investment within the next 12 months?” Once again, the proportion of neutral responses to this question compared to the previous survey dropped from 11% to 2%. However, those answering unlikely increased from 11% to 20%. Although this largely offsets the fall in those answering likely, respondents who said that they were very likely to make a significant capital investment increased from 32% to 42%.

This could be interpreted by the varying fortunes of different states and sectors, or could even represent differing opinions of internal or external influencing factors affecting the country. Indeed, throughout 2019 the delayed ratification of NAFTA 2.0, known as the United States-Mexico-Canada Agreement (USMCA), has impeded the legal certainty needed for Mexico’s relationship to flourish with its most important trading partner, and the world’s largest economy, the US. In spite of the Democrats’ recent willingness to move forward with ratification, it is uncertain when it will pass through the US Congress, as the Senate majority leader, Mitch McConnell, suggested a vote would not be initiated until after impeachment proceedings. This was contradicted by a White House spokesperson who signalled that they would “push hard” for the deal to pass by the end of the year.

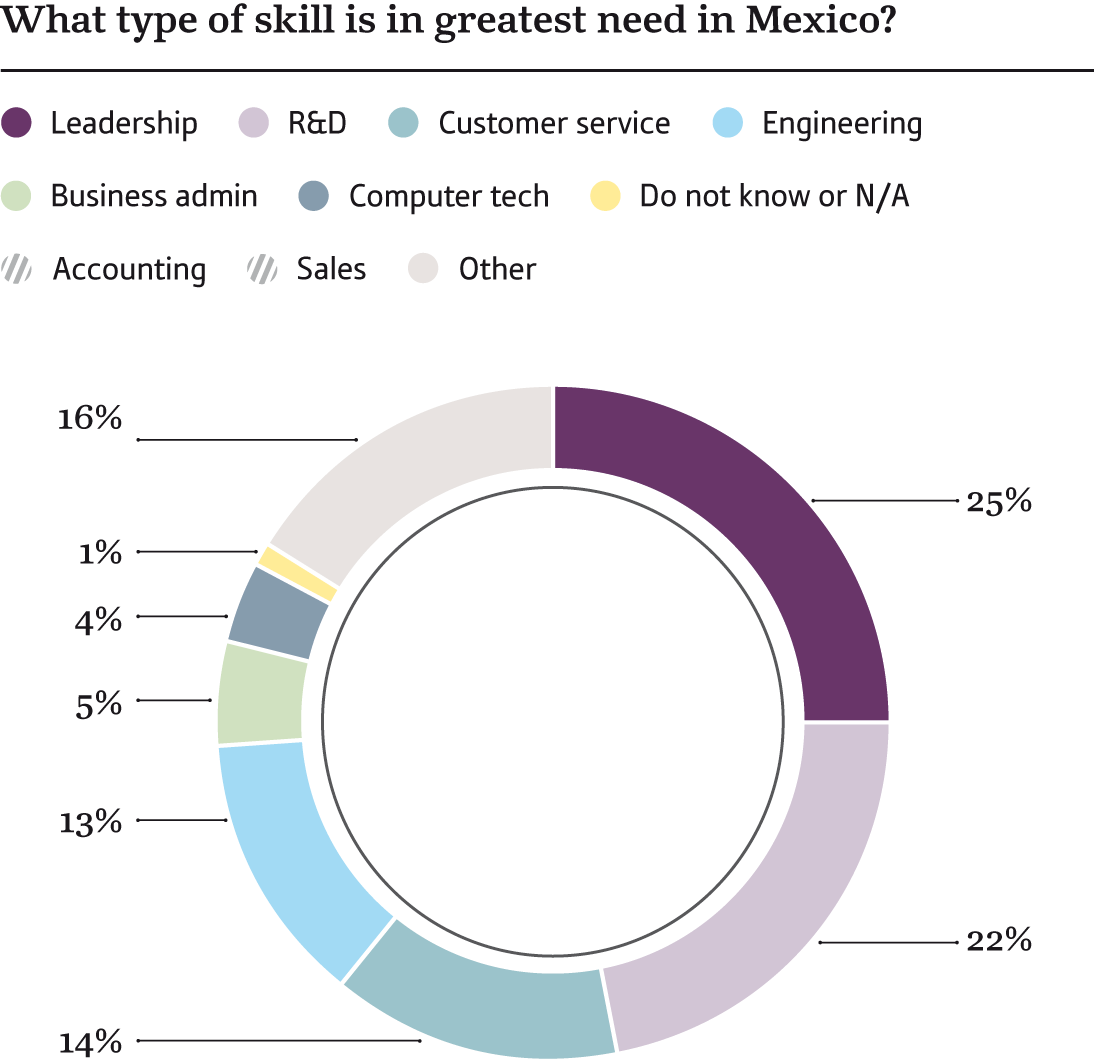

The question about human capital also sheds light on shifting trends. While leadership and research and development have consistently been among the most popular choices, it is the first time that leadership topped the poll. While this may implicitly relate to frustrations over slowing economic growth, AMLO has also made a number of decisions deemed unfavourable by the business community, such as the dissolution of ProMéxico, the investment promotion agency. However, both state authorities and the private sector have taken on their own initiatives to lead in investment promotion. These include the Alianza Centro-Bajío-Occidente (ACBO), representing the Bajío region, widely regarded as the country’s industrial powerhouse. This decentralisation of leadership could also be connected to the shift in responses in the latest survey, and new initiatives such as the ACBO may be an appropriate antidote to political uncertainty at the federal level.

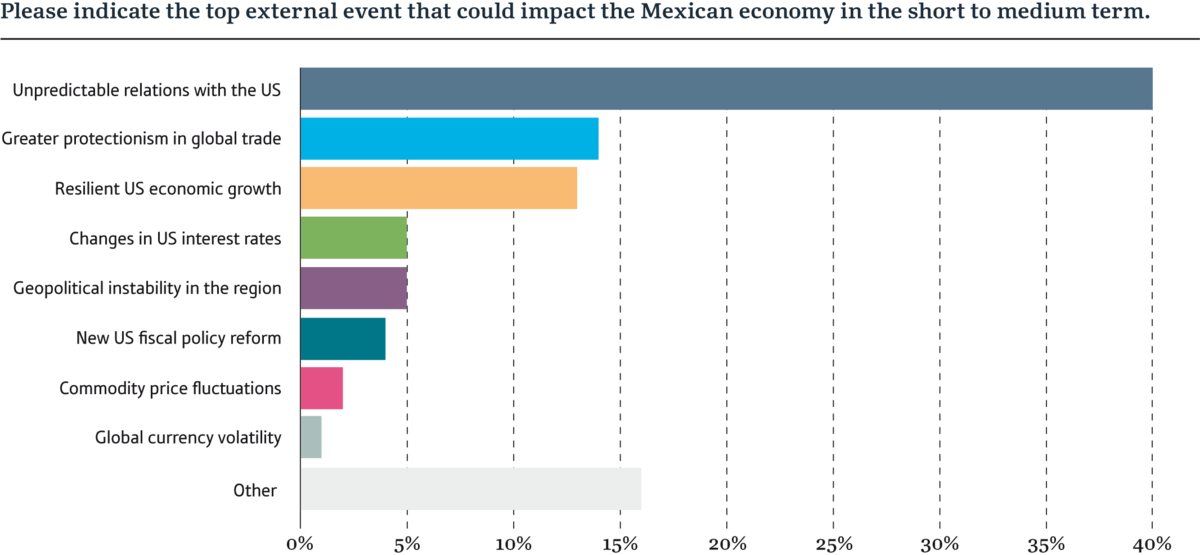

In terms of the external factors that could impact economic growth in Mexico, business leaders’ most chosen option was unpredictable relations with the US. After being signed by the countries’ three leaders over a year ago, the move Democrats in early December to publicly back an amended USMCA will undoubtedly help quell the business community’s frustration surrounding the lack of progress in ratifying the tri-nation trade deal. The concern about US relations from CEOs in Mexico could also be linked to two instances in 2019 of Trump publicly pressuring Mexico. On May 30 he used Twitter to threaten Mexico with the imposition of incremental tariffs on all goods exported from Mexico to the US, should they not do more to combat illegal migration into the US, and in early August Trump criticised Mexico for its handling of security within its own borders, and threatened to “decertify” the country.

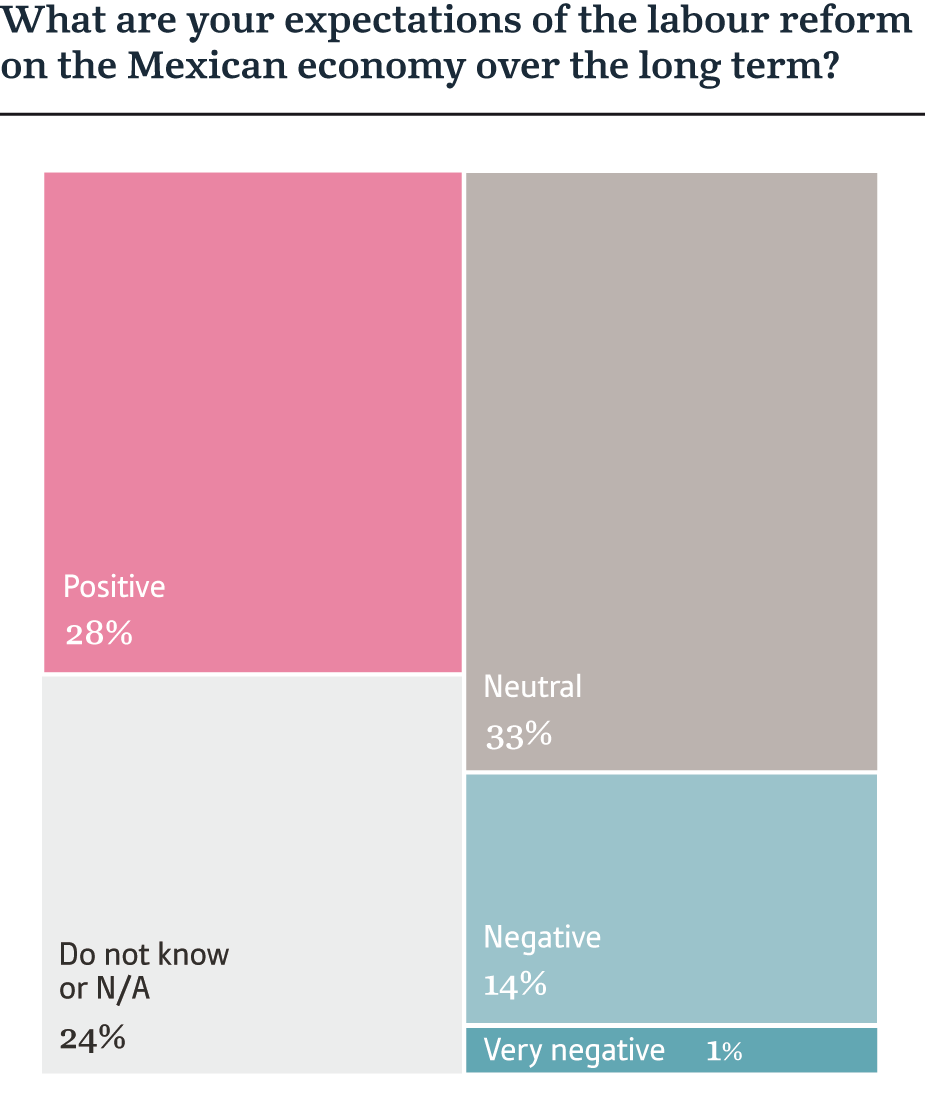

The major legislative change that has taken place since the publication of our last CEO survey is the passing of the landmark labour reform. The most popular response to this question was neutral, chosen by one-third of respondents, implying that the business community are waiting to see how the reform progresses in the real economy before taking a position. That being said, twice the number of CEOs deemed their expectations of the reform to be positive (28%) rather than negative (14%). Although there are concerns that it could eventually dent Mexico’s competitive advantage and lead to increased wages, the passing of the law was also a prerequisite for the Democratic Party in the US to consider supporting the ratification of the USMCA. This was crucial given that the party now controls the US lower house, so their support is needed to pass the treaty. The positively slanted responses could also have to do with a wider issue: the possible advantage of enhanced productivity resulting from the reform, which is arguably one of the principle obstacles to Mexico achieving higher growth.

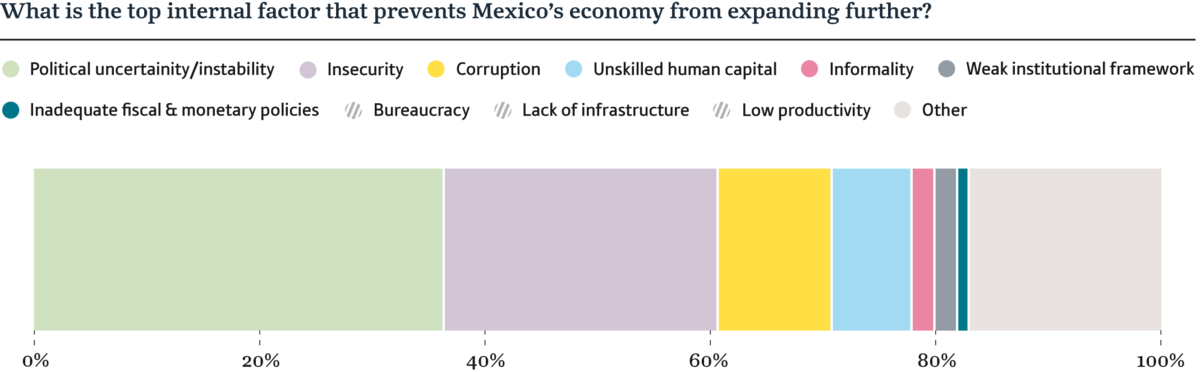

On the theme of structural challenges, respondents made clear choices about what internal factors are preventing the country from reaching its full growth potential. Out of a possible 10 responses, CEOs mainly highlighted insecurity and political uncertainty or instability as key factors, receiving 24% and 36%, respectively. While it cannot be ignored that the paradigm shift caused by AMLO’s style of governance has been disruptive for businesses, it is perhaps the uncertainty with which certain decisions have been handled that respondents are concerned with the most.

Such an example can be seen with the handling of the New Mexico City International Airport. Cancelled in a controversial referendum in October 2018, construction was halted while the project was one-third complete, while AMLO’s favoured alternative, a former military base in Santa Lucía, was subsequently blocked by judges. Construction work at Santa Lucía has resumed; however, there is uncertainty surrounding its operational viability as an airport, and is notably an unpopular decision with all Mexican airlines currently operating out of the capital. Lack of clarity on energy policy has also seemed to have slowed investment the sector, as well as a lack of progress of the landmark sector reform, as the president suspended further auction rounds until 2022.

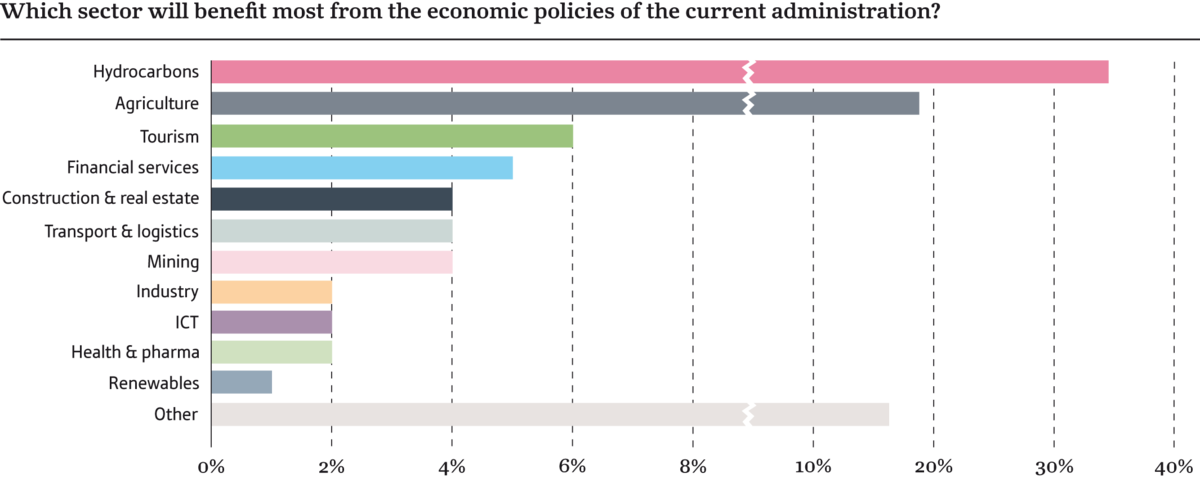

Interestingly, however, the most popular answer to the question regarding the sectors that will most benefit from the president’s policies was hydrocarbons, receiving 34% of answers. The only other option that received a notable amount of responses was agriculture, at 19%. These two standout responses are noticeable because they reflect AMLO’s more protectionist, economic-nationalist strategy of import substitution. Historically both a top oil-producing state and a substantial producer of maize on global markets, Mexico is now a net importer of both of these commodities due to its own low production yields. This is something AMLO has promised to reverse.

Although the president’s commitment to a hydrocarbons-focused energy policy has attracted criticism for its lack of relevance to the 21st century economy, Mexico still has further reserves of 7bn barrels following several recent deepwater discoveries. Even since the slump in oil prices, the commodity still contributes more than 20% of the government’s budget. While the benefits of this hydrocarbons-focused energy policy may not be immediate, according to AMLO his landmark plan to build a refinery at Dos Bocas in Tabasco will provide a much-needed boost to Mexico’s domestic downstream capacity, with the hope of one day returning the country to its position among one of the world’s top petroleum-producing nations.

Covid-19 Economic Impact Assessments

Stay updated on how some of the world’s most promising markets are being affected by the Covid-19 pandemic, and what actions governments and private businesses are taking to mitigate challenges and ensure their long-term growth story continues.

Register now and also receive a complimentary 2-month licence to the OBG Research Terminal.

Register Here×